Link is the top idea by SpareBank analyst Petter Kongslie. Link is Europe’s number one in helping companies and state institutions communicate with their customers through SMS, WhatsApp, Wiber, Instagram, and other messaging platforms. If you fly, and get a boarding SMS, it could be from Link.

The major catalyst happened in early January – Link closed the sale of its US subsidiary at 14 times EBITDA. Link trades at 8 times EBITDA. Its core business has similar profitability metrics as the disposed US business. The transaction indicates the upside.

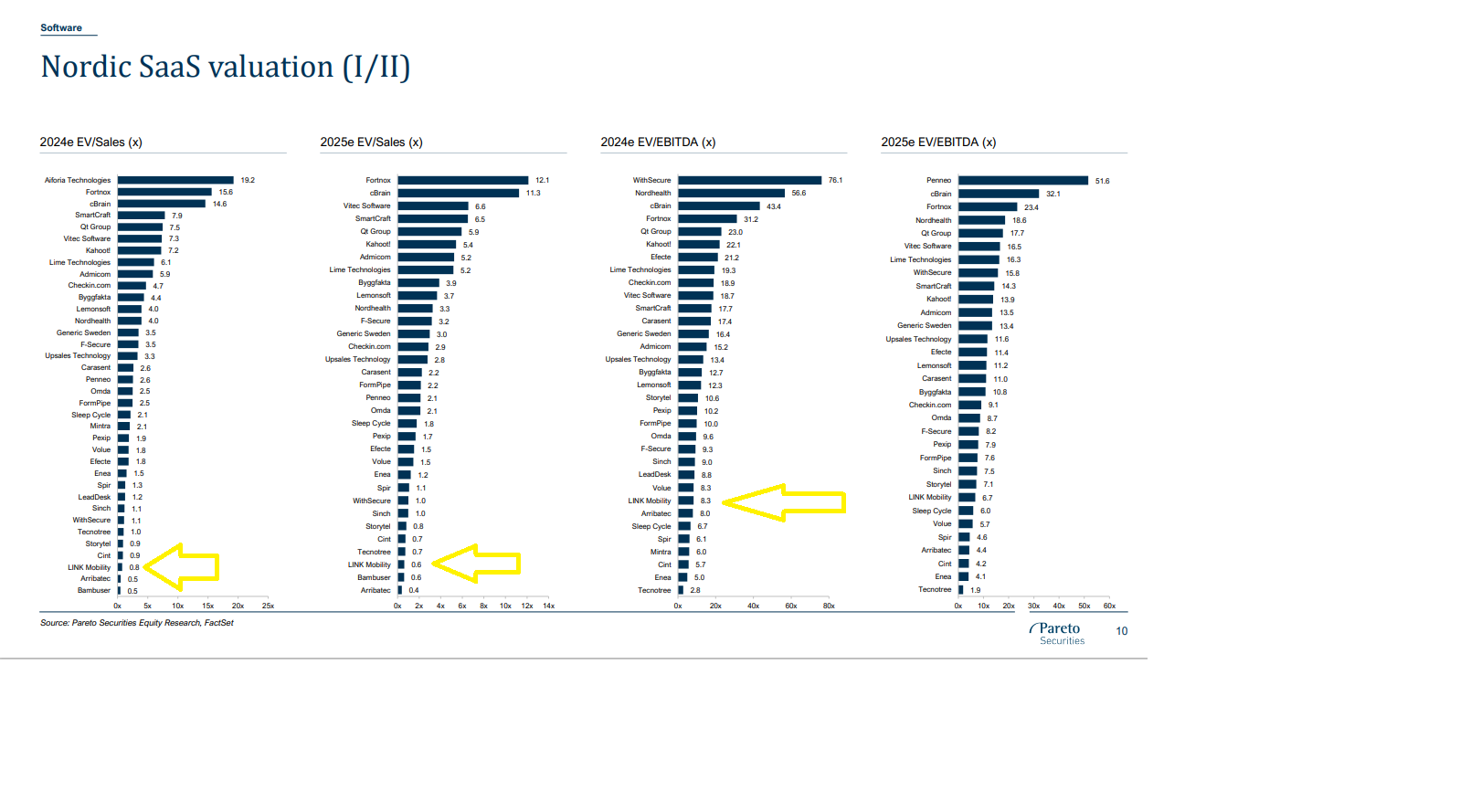

Link is one of the cheapest Scandinavian SaaS companies. The reason was its high leverage of 4.5 times EBITDA. The USD 260 million US subsidiary disposal reduced the leverage to around 1 times of EBITDA. The leverage issue is now resolved. Share price re-rating should be next.

The company has been growing organically at 14% (12% from existing and 2% from new clients). The growth is expected to continue. Further growth may be achieved through market consolidation. The company has a great track record of 30 acquisitions. After selling its US business at 14 times EBITDA, Link can now buy companies at 5-6 times EBITDA (its histrocial track record) to increase its growth further.

LINK in Short

- LINK Mobility is a Communications Platform as a Service (CPaaS) provider, providing communications products and services to enterprises, helping them to drive customer engagement and increase customer satisfaction at every part of the customer journey.

- LINK has 650 employees in 30 offices across 18 countries in Europe and the US

- Revenue close to NOK 6 billion

- Adjusted EBITDA above NOK 700 million => EBITDA margin 12%

- LINK has 50 thousand customer accounts globally and exchanges 18 billion messages a year

- In Norway, Link has a 2/3 mkt share, Sweden 50%, and in other European countries, top three positions with a 10-30% market share.

LINK was founded more than 20 years ago and relisted on the Oslo Stock Exchange in 2020 after being taken private in 2018.

Link is very cheap vs peers.

See Pareto´s relative valuation.

The leading Scandinavian brokers have all turned very bullish in January :

-

- The Arctic Securities – published on 15 January 2024 research titled: “Link Mobility – Getting the message across – one to own in 2024.” Their Price Target is 23 NOK, a 30% upside from the current share price.

-

- Pareto Securities – initiated their research coverage on 22/1/24 titled “Back to basics” with a Price Target of 25NOK, a 50% upside from the current share price.

-

- Sparebank published their latest research on 8/1/24 titled “We expect business as usual in 4Q23 and solid free cash flow” with a Price Target of 25 NOK, a 50% upside from the current share price.

- ABG Sundal Collier published their latest research on 23/1/24 titled “Link Mobility – An Undervalued Quality Company” with a Price Target of 24 NOK, a 40% upside from the current share price.

The Q4 report will be crucial. The company will provide details on the restructured and deleveraged company plus an update on aquisitions. I expect further rerating after the Q4 report. Our price target is 25 NOK for now. If the Q4 report is as bullish as we expect, we will increase our price target to 30 NOK.

What is next?

Link is deleveraged. It can:

-

- Continue acquisitions at 5-6 times EBITDA. The company has a successful track record of 30 acquisitions in Europe. This will further accelerate the growth rate above the organic 14%. In the past, the share price reacted positively to well-priced acquisitions. We expect this to continue.

-

- Buy back its shares or pay dividends. The current bond limits both; Link can buy back the debt. We believe this is less likely. Profitable growth will be the main focus.

The next catalyst is the Q4 report on 15 February. If the report is positive, expect the price target updates in the days after the report. It has most likely accumulated a portfolio of acquisition candidates, which should be taken over in the coming months. The share price is most likely to react positively to the announcements.

Summary

Link is cheap vs its peers as the Pareto slide shows. Link is cheap vs the transaction it just closed in the US. The reason for its low valuation was its high leverage, which is now resolved. Link is growing organically at 14% with a high cash conversion rate. Likely, acquisitions at lower multiples will accelerate growth further. Link successfully integrated 30 acquisitions into the profitable enterprise. It will do so in the future as well. Bright days ahead.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.