Valeura Energy Inc. (VLERF): A Unique Investment Opportunity

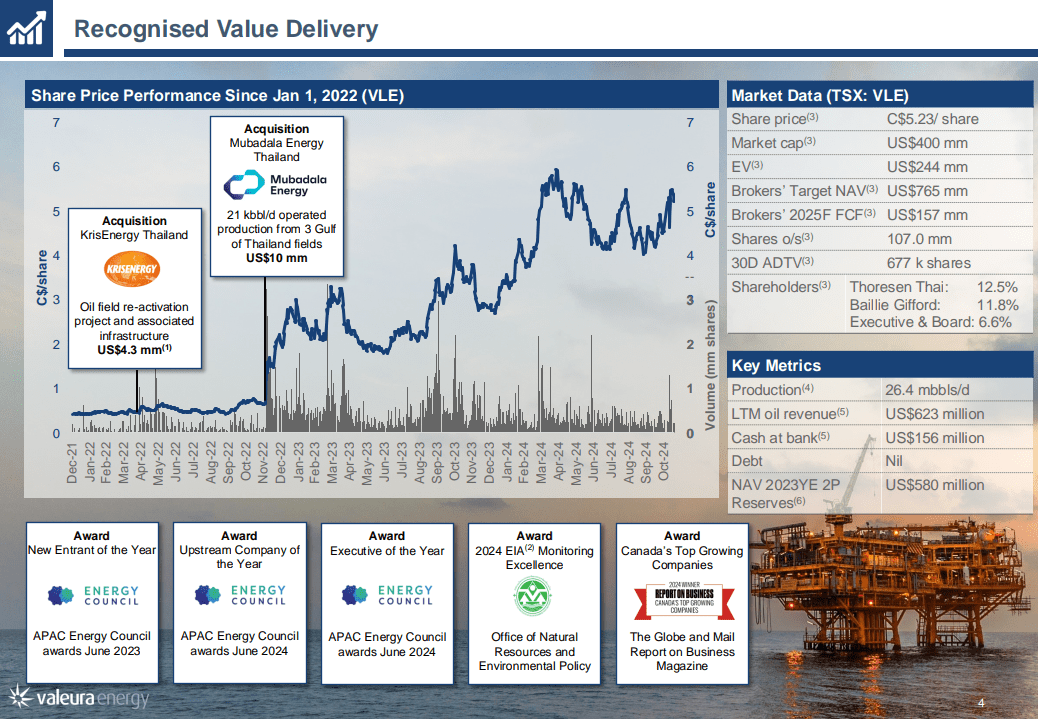

Valeura Energy, a Canadian oil producer with a significant presence in Southeast Asia, presents a compelling investment case. Despite having a market capitalization of $400 million, the company boasts $156 million in cash reserves, no debt, and generates $200 million in annual free cash flow (FCF).

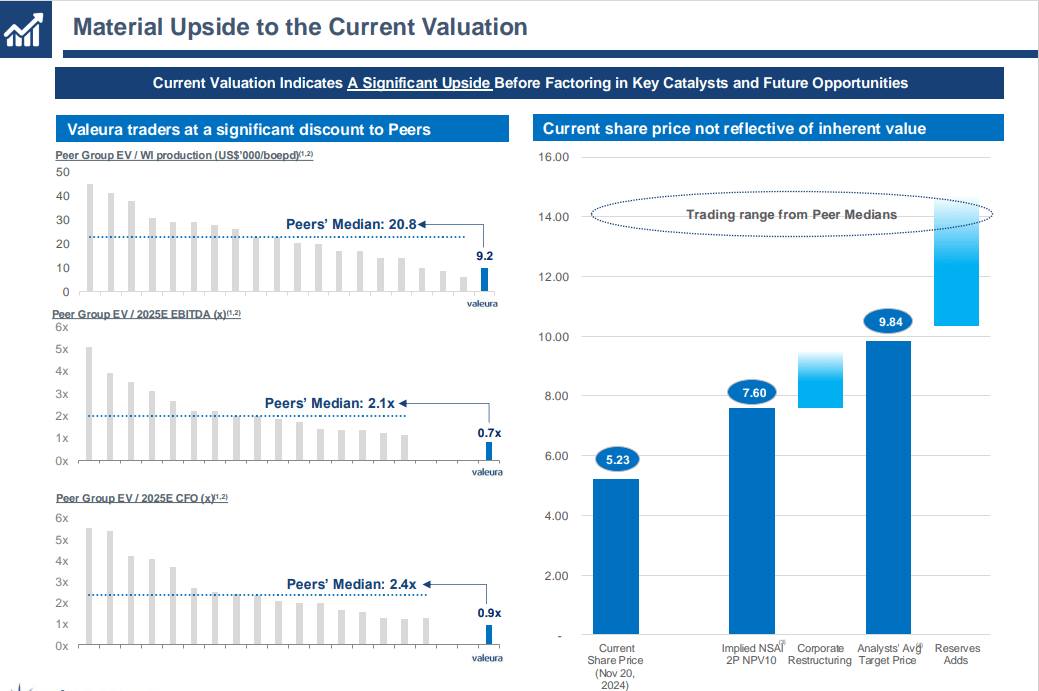

The company’s recent strategic moves and operational efficiency have led to remarkable share price growth, yet Valeura’s valuation remains attractive. Shares trade at just two times FCF and an enterprise value-to-EBITDA (EV/EBITDA) ratio of 0.8, underscoring a significant discount compared to industry peers.

Strategic Acquisitions Drive Growth

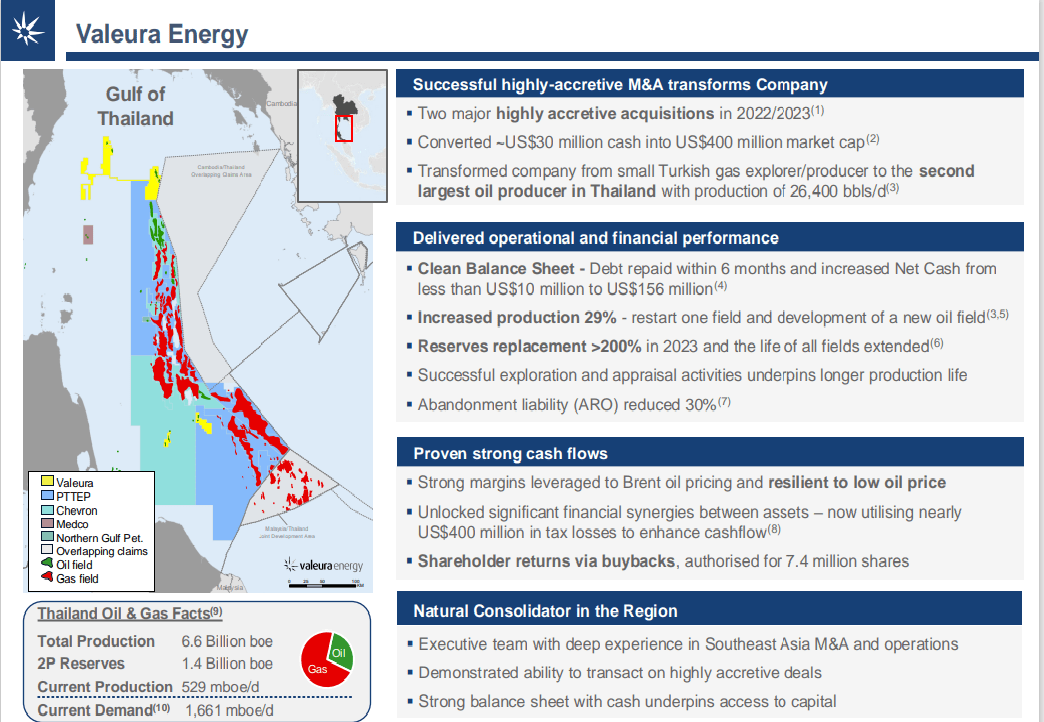

Initially focused on oil exploration in Turkey, Valeura’s transformation has been driven by two major acquisitions in 2022 and 2023. These deals have turned $30 million in cash reserves into a market capitalization of $400 million.

In addition to expanding production capacity, Valeura leveraged $400 million in acquired tax-deductible losses to enhance its financial efficiency. The restructuring ensures that three of its four production assets benefit from these tax advantages, creating an estimated net tax saving of $200 million over several years.

Operational Highlights

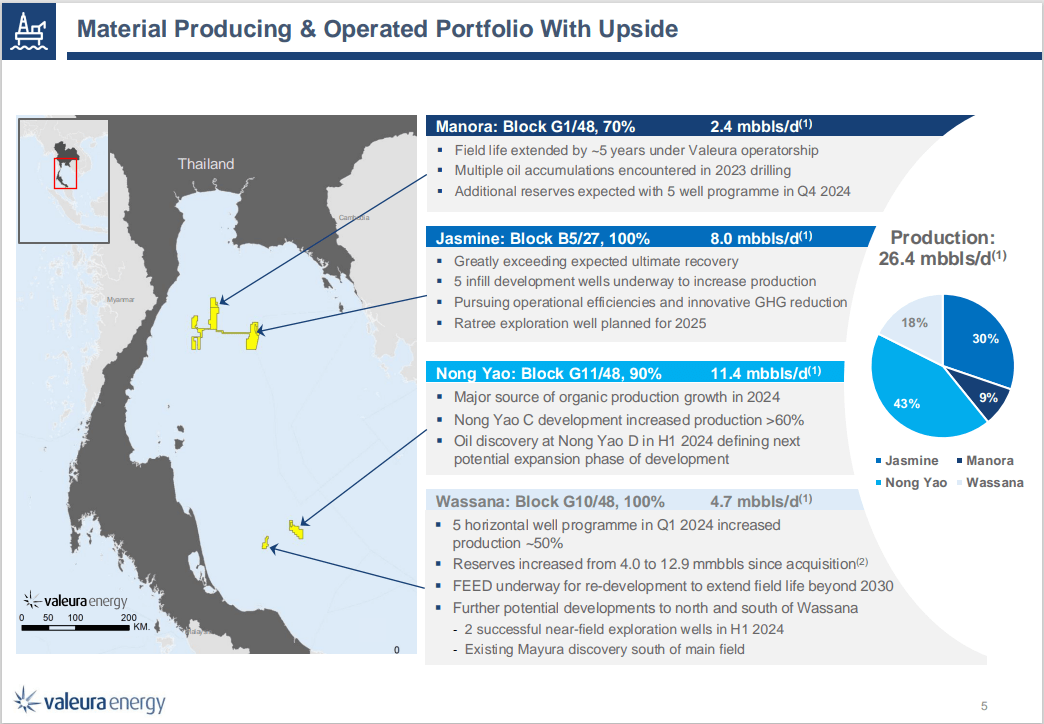

Producing Assets in the Gulf of Thailand Valeura operates four production assets in the Gulf of Thailand, a region known for its established oil infrastructure and low-cost operations. With an average production of 26,400 barrels per day (BPD), the company generated over $620 million in revenue last year.

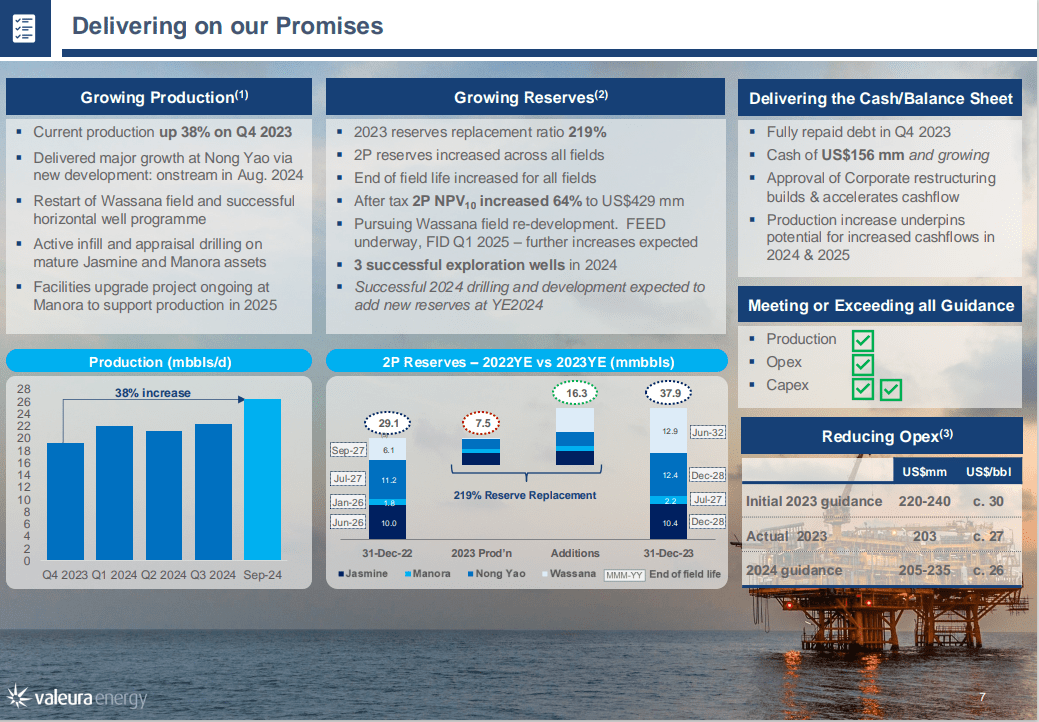

Production growth has been impressive, increasing by 38% year-over-year, while proven and probable (2P) reserves grew by 31%. This success is bolstered by a high drilling success rate of approximately 95%, ensuring consistent reserve replacement and long-term production stability.

Financial Strength and Acquisition Potential

Valeura’s strong financial position enables it to pursue additional acquisitions. With a net cash position expected to exceed its market capitalization by the end of 2025, the company is well-positioned for future growth.

Management has indicated interest in acquiring additional assets, particularly as major oil companies divest smaller assets in Southeast Asia. With limited competition in the region, Valeura is poised to secure valuable assets at favorable prices.

Valuation and Shareholder Returns

Despite a tenfold increase in its share price over the last few years, Valeura remains significantly undervalued. The stock, currently trading at C$5.20, has a price target of C$9.20, representing nearly 80% upside potential.

Management’s alignment with shareholders—holding a 6.6% stake—further supports investor confidence. Additionally, the company’s recently announced share buyback program is expected to enhance shareholder returns.

Catalysts for Growth

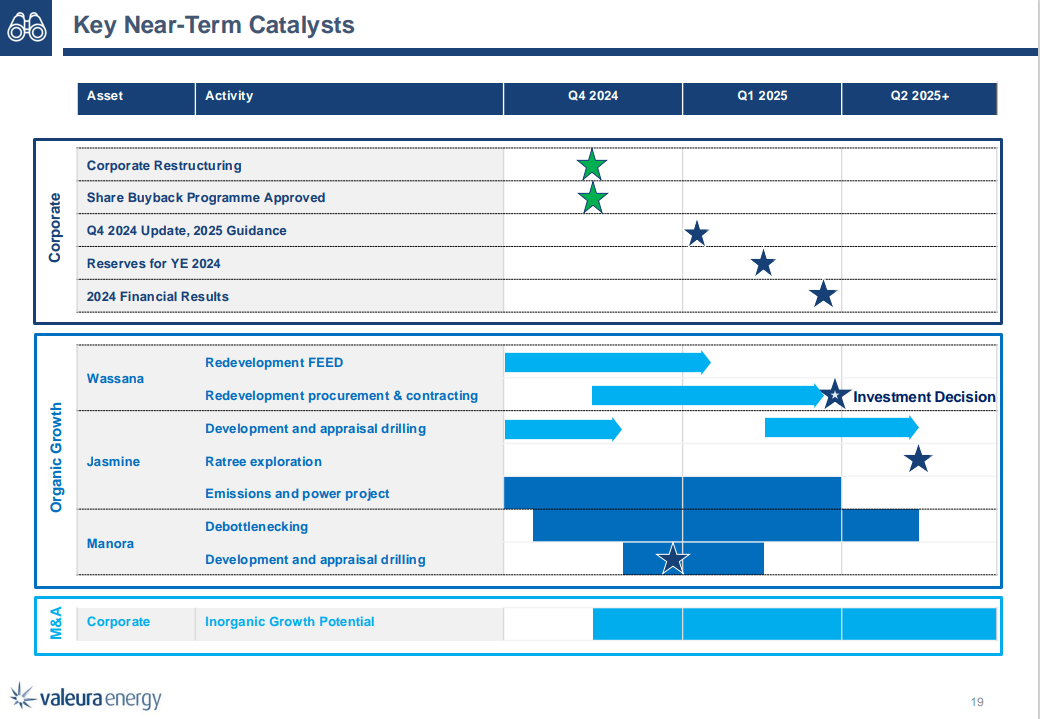

Valeura has multiple catalysts that could drive its valuation higher, including:

Updated cash balance and 2025 financial guidance (expected in early 2025).

Development progress at the Wassana field (late Q1 2025).

Ongoing operational updates and potential acquisitions.

Conclusion

Valeura Energy stands out as a well-managed company with a strong balance sheet, robust cash flow, and proven operational expertise. The strategic acquisitions that propelled its past success position it well for future growth.

As the company continues to execute on its strategy, Valeura’s stock appears poised for significant upside. Investors seeking undervalued opportunities in the energy sector may find Valeura to be a compelling choice.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

The company is reporting tomorrow its first quarterly report since it was listed.

The major event will be the shareholder list from the IPO – there are very strong names – it is already on their www, but not many people noticed

The day after it will be 40 days from the listing – that is the day of the blackout period – after 28/11, brokers will start publishing the invitation reports. there were five brokers in the syndicate. This could be a good newsflow.

Why we doubled our position today

Since the listing, SVEAD has outperformed the real estate segment, but it is still trading below the issue price of 39.5 SEK per share. We have doubled our position today. I believe the report tomorrow and mainly the initiation reports in the coming days should start the share price rerating.

Other opportunities

We are very bullish on Electro Optic Systems, the leader in shooting down drones. Do watch short video with its CEO released yesterday:

We are bullish Nebius, our largest position now. We are 150% over the last six weeks. We believe the share price could easily double over the next six months. Investmnet thesis:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Shamaran Petroleum, a Lundin-controlled company, should benefit from the reopening of the Kurdistan pipeline. Clarkson published a research report estimating that the share price could double. The company is doing well even with the pipeline closed, selling in the local market. Reopening could be very bullish for Shamaran and its shareholders.

Kurdistan Region oil exports could continue in weeks: Minister

ERBIL, Kurdistan Region – Kurdistan Region’s long-suspended oil exports could be resumed later this year if the Iraqi parliament passes an amendment proposed by the federal government, Iraq’s foreign minister said on Thursday.

Last week, the Iraqi government approved a proposal to amend articles from the federal budget to authorize compensation to companies operating in the Kurdistan Region for oil production and transportation costs, setting the rate at $16 per barrel. The proposal – yet to be finalized by parliament – aims to resume oil exports from the Region.

“We have sent this decision to the parliament because it falls under the budget law and we hope that the legislature will vote on it in these days,” Iraqi Foreign Minister Fuad Hussein told Rudaw’s Sangar Abdalrahman on the sidelines of the COP29 climate summit in Baku, Azerbaijan.

“If it [parliament] passes it [the amendment], the Kurdistan Region will be able to export oil… before the New Year,” the minister explained.

Oil exports from the Kurdistan Region through the Iraq-Turkey pipeline have been suspended since March 2023 after a ruling by a Paris-based arbitration court ruled in favor of Baghdad over Ankara, saying the latter had breached a 1973 pipeline agreement by allowing Erbil to export oil independently since 2014.

Hussein also mentioned that there are ongoing talks with Ankara over the issue.

The Association of the Petroleum Industry of Kurdistan (APIKUR), an umbrella group for international oil companies operating in the Kurdistan Region, on Thursday welcomed the proposal introduced by Baghdad.

Iraq’s three-year federal budget bill, passed in June 2023, had set the rate for one barrel of oil at $6.90 and international oil companies (IOCs) have requested three times that amount.

Before the halt, Erbil exported around 400,000 barrels per day through the pipeline, in addition to some 75,000 barrels of Kirkuk’s oil.

The KRG signed production-sharing contracts with international oil companies when it began its independent oil sector. Under this model, the oil companies cover the entire cost of production while the KRG receives the lion’s share of the profits from successful projects.

Baghdad has repeatedly said that these contracts violate the constitution and must be amended to match the service contracts that the federal government prefers before exports can resume.

There have been international calls for the resumption of Kurdish oil, with the US saying an end to the halt is “mutually beneficial” to all parties.

Clarksons Published a bullish report on Shamaran today:

Strong Free Cash Flow Following Asset Transaction We reiterate our BUY recommendation on ShaMaran and maintain our Target Price of SEK 1.3/share. We postpone the expected pipeline reopening to the start of Q2 next year, with several reports suggesting that Iraq’s Cabinet has approved a proposal to amend the budget law in a way that would theoretically allocate new funds to pay Kurdistan’s oil contractors. We model an upside of 78% to our current Target Price.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Sveafastigher, a leading Swedish residential owner, placed its IPO with Friday as the first day of trading. The book was multiple times oversubscribed, but the stock is still trading around the IPO price. We bought in the IPO and bought more in the open market. We like the story.

Sveafastigher, ticket SVEAF, is the largest residential owner listed in Sweden with 8 bln market capitalization and a free float of around 50%.

Sveafastigher owns 14 470 apartments; 690 additional ones are in construction, and 7 200 is in development.

It trades at a P/NAV of around 0.5 vs its Residential Peer Average of 0.77. That means a 54% upside to re-rate to the average.

There are strong arguments that SVEAF should trade at a premium – it has growth (through new apartment construction and through the remodelling of part of its existing portfolio), and both are in progress.

The deal was well allocated. The top 20 investors got almost 70% of the SEK 3.5 billion of capital raised. Many investors got very low allocations. Our allocation was only 10% of our subscription. Investors who got small allocations sold those in the market. That caused the share price volatility. We were buyers.

There will be several potential catalysts during the next few weeks:

Release of shareholder list – I hear strong names bought into the IPO. If correct, this should increase investor confidence and initiate price recovery.

Publication of initiation research by the syndicate brokers – the research can be published 30 days after the IPO. There may be five research initiations by the end of the year.

3rd quarter will be reported on 27 November. So, most likely, we get an intitation report before that and then updates based on the first quarter reported as a public company.

Decreasing interest rates should help the real estate sector.

Results of the rent price increase negotiation – Sweden is a rent-regulated market. Associations of homeowners with associations of tenants negotiate rent price increases. The talks are ongoing and may be concluded this or next quarter.

SVEAF should also be included in the index. Peer inclusion drove share prices by 10% in the past. It should happen towards the end of 2025.

Completing the newly constructed apartments and the remodelling projects should drive the revenue further, which should help the stock re-rate.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

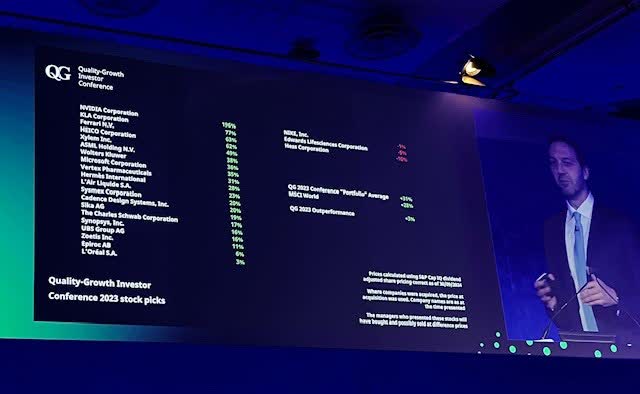

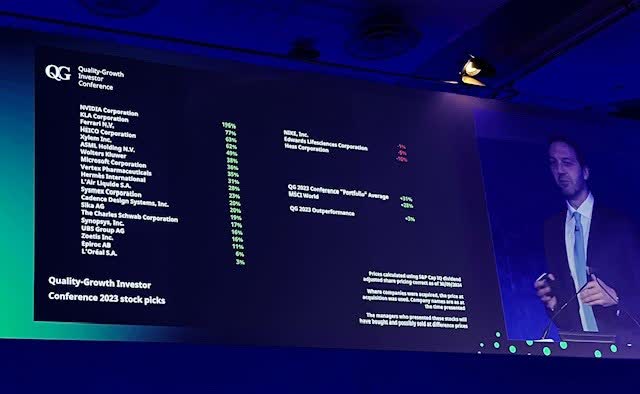

Nvidia was one of the top picks at last year’s conference, and it generated returns of 196%.

This article summarizes ideas from this year’s conference.

Key investment themes include focusing on large growth compounders, investing in disruptive consumer stocks, and prioritizing quality technology companies with sustainable competitive advantages.

Luis Alvarez/DigitalVision via Getty Images

The third year of the Quality Growth Investor Conference brought interesting investment ideas and several investment conceptual concepts.

Most Interesting Big Picture Points

The speakers argued that it is less risky to financially succeed with a large company investment than a small, promising company. Out of 800 small companies in the UK at the start of the century, only three succeeded in becoming UK large caps, while 600 have left the index. Several speakers stressed this theme. James Anderson, one of the UK’s most prominent investors, argued that 70 companies have accounted for most global value creation since 1995, and the concentration of value creation is increasing.

Presenters illustrated that investors want growth companies to reinvest profits. Growth companies that pay dividends tend to underperform significantly.

Finally, the presenters argued that trading around your positions can generate superior returns compared to general buy-and-hold strategies. Increasing positions on weakness and decreasing on strength generates substantially higher returns than traditional buy-and-hold strategies.

The conference, as well as post-conference networking, generated several exciting ideas. We share those below.

The companies recommended at last year’s conference achieved significant value creation. Nividia led with 196%, while almost all companies achieved double-digit share price growth.

Best-performing stocks presented at last year’s conference.

FIII

Individual Presentations

Each of the presenters had 20-minute short presentations. The summary of the most interesting ones is below:

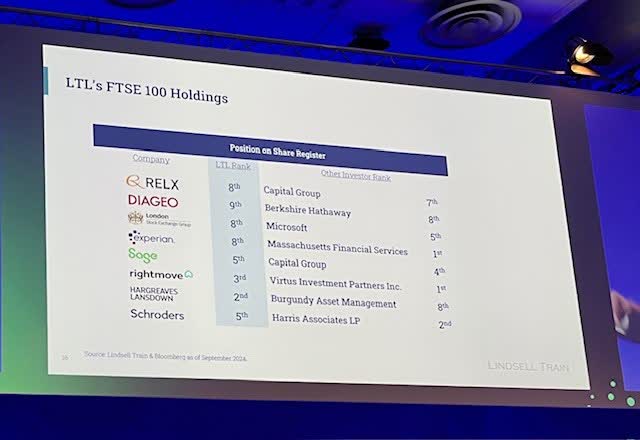

Nick Train of Lindsel Train

In the UK, Equities focuses on large growth commodities.

Train is a Lindsel Train co-founder who has managed global portfolios for over 40 years. In his presentation, he raised the main points:

UK equities have underperformed major markets since 2000

Some UK-listed global winners will drive the UK market in the future

Reasons for UK underperformance are mainly a strong 15% weighting of underperforming Telecom companies and a shrinking share of UK tech companies.

ARM and Sage are symbolic of UK underperformance

ARM is growing strongly, but listed in the US – ARM would be 5% of the UK index if listed there

Sage – for decades, has been forced by the market to pay high dividends – after they stopped and started reinvesting into growth – the share price started to over-perform

Investors want growth from tech – not dividends. Dividend-paying tech underperforms

Only a few small companies become relevant – over 25 years, only three UK companies from the index have become large companies, while 611 small companies out of 800 left the index

Large companies that can compound strong growth are the less risky winners.

AstraZeneca – the largest company on the index, now has appreciated five times over the period – its weighting in the index tripled.

London Stock Exchange – grew 24 times – its weighting doubled from 1% to 2%

Relex – moved from the 60th largest to 6th – appreciated 7 times

Rightmove – from 500th to 80th – leading digitalization of the UK property market – appreciated 17 times

We are bullish on UK companies – US investors are pushing the strong performers to grow even stronger

Investors should focus on large companies and focus on companies that have strong global investors as they push for performance – PICTURE

Our favourite is London Stock Exchange – it has a lot of optionalities to continue growing strongly

Train presented a slide with his UK favourite stocks

FII

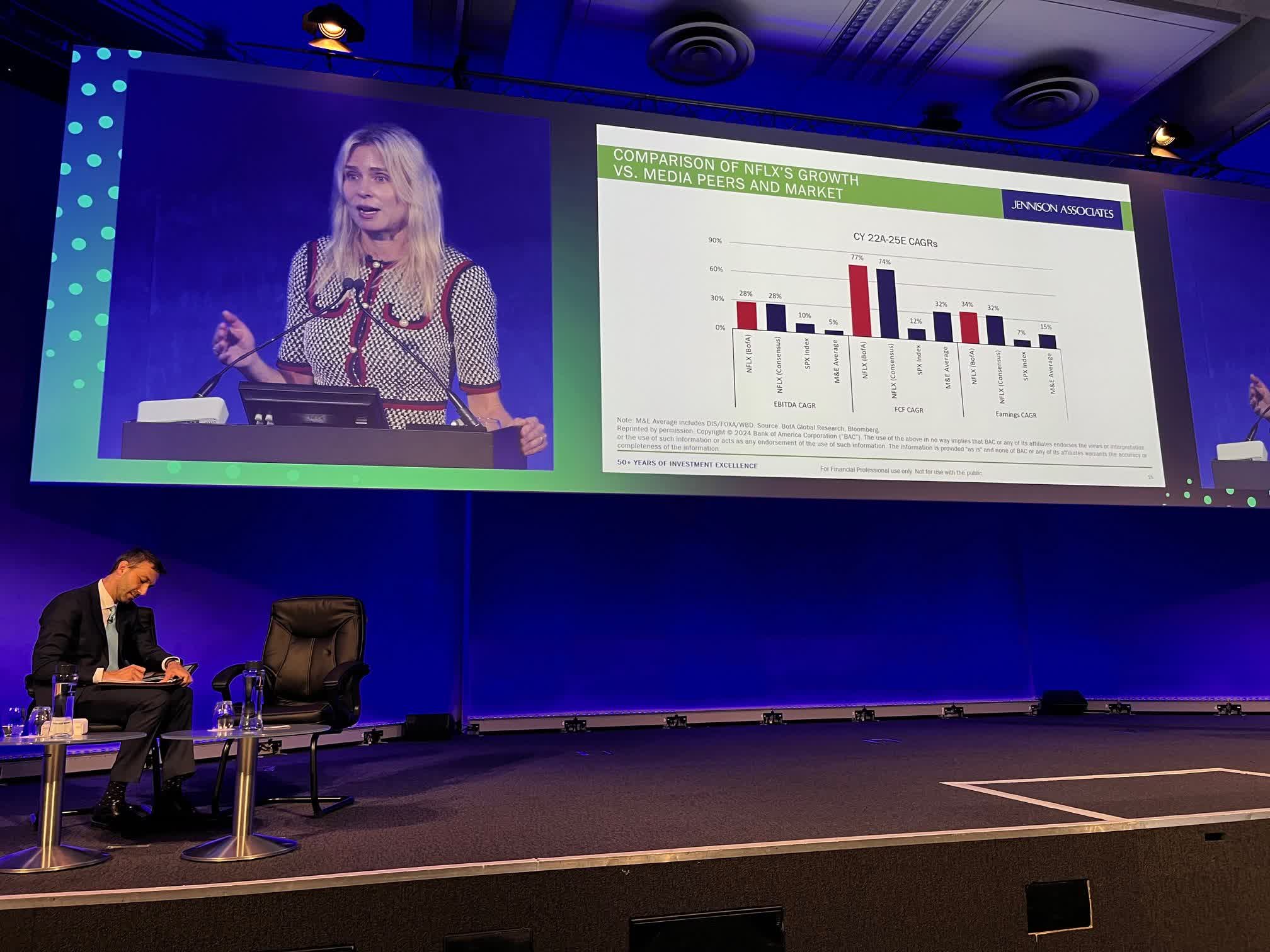

Rebecca Irwin of Jennison Associates

How to invest in disruption

Global asset manager Jennison Associates, founded in 1969, has $200 billion under management. Irwin has been a portfolio manager at Jenninson for almost two decades, focusing on consumer stocks. In her presentation, she focused on their investment principles and her two favourite positions.

We like consumer stocks; they are two-thirds of global economies

We look for companies with four characteristics

– Our companies must satisfy the below criteria

Large addressable market – only scale can grow durability of growth

Consumer acceptance

Can scaling become profitable

Can growth be durable

The combination of the above is the basis of long-term strong revenue growth

Two examples of the growth through disruption:

Netflix – disrupted media industry

Started as DVD mailing service

Moved viewing from scheduled programming to watch any time, what you want

Netflix is growing at a multiple of the industry

FII

Mercado Libre – Latin American retail disrupting the local industry

Original brick-and-mortar retailer

Now largest online store in Latin America

Large addressable market – population of 500 million and GDP of 5 trillion USD

Durability of growth secured by innovation – 76% of items delivered in 48 hours

Growth through disrupting new segments – for example, financial services in Brazil

Growth through disrupting new segments – Advertising

Growing strongly with Growing margins

FII

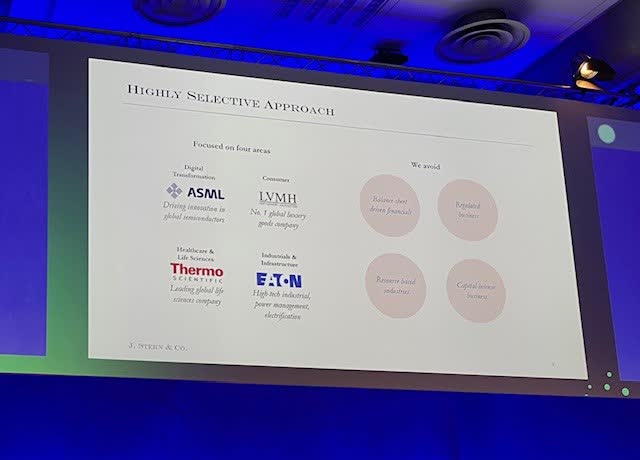

Christopher Rossbach of J.Stern and Co

Quality in Technology.

Christopher is a co-founder and CIO of a London-based private investment partnership focused on high-quality mega-cap global stocks with $2 billion under management.

We focus on companies with

Strong, Sustainable competitive position

Good growing industry

Management with a track record of value creation

Financial strength to weather adversity

J. Stern sees great value in consumer stocks

J. Stern is focused on four areas

FII

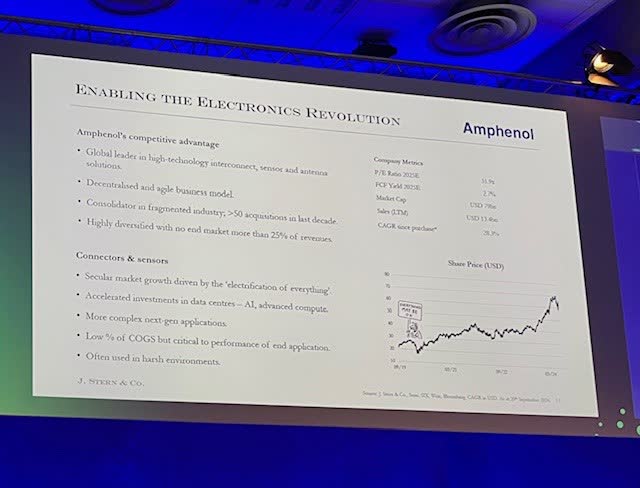

Amphenol – world leader in connectors, US listed, market capitalization of 80 billion USD

FII

ASML – Monopoly producer of machines for semiconductor production

Acquired only in the first quarter of 2023

The beneficiary in reshoring of semiconductor production – the return of the production to developed markets to limit global geopolitical risks

Significant backlog of orders

FII

Laure Negiar of Comgest.

Negiar joined the Comgest Global Equities team in 2010. The firm is Paris-based and is employee-owned. Its 50 employee shareholders are asked to borrow to fund their stake in the firm. Laure presented her positions in Eli Lilly and Analog Devices:

Eli Lilly – global pharmaceutical giant

original thesis was based on its strong position in insulin – focused on improved margins from its leading position

Later, the thesis changed – first, margins improved, and then obesity changed the game

FII

Analog devices – a global leader in analogue devices

High barrier of entry – too expensive to enter

Big customers – Auto and Industrials

Highly cyclical

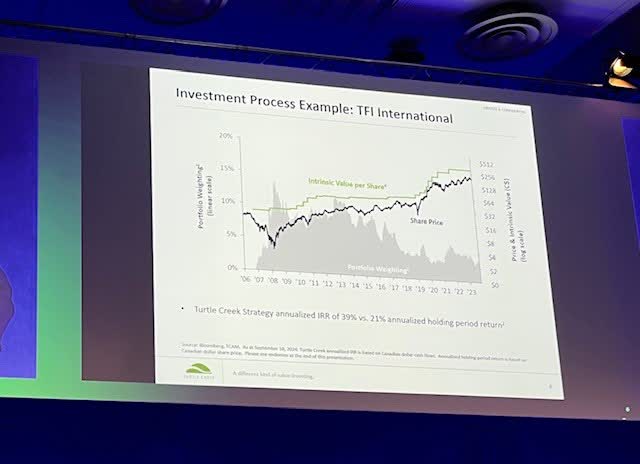

Andrew Breton of Turtle Creek Asset Management

Do not just buy and hold

Breton is the CEO of the Canadian investment manager with 5 billion USD under management, a value investor with a 22% compounded return since 1998.

We hold companies for a long period. Our shareholding fluctuates.

Buy and hold is an inferior strategy to buy and optimize

If you own a company, you need to react to fluctuating share price

We increase our positions if the value gap proposition increases and reduce if that decreases

Two examples of Turtle Creek’s strategy:

TFI International

Canada’s largest trucking company, 5th in North America, with a $12 billion market capitalization

Over 200 acquisitions deploying 6.5 billion USD

We bought in 2009, and the share price was going down. We were buying more. When the share price appreciated close to our intrinsic value, we were decreasing.

Buy and hold return would be 21% if you buy and optimize; our IRR was 39%

TFI expensive now

FII

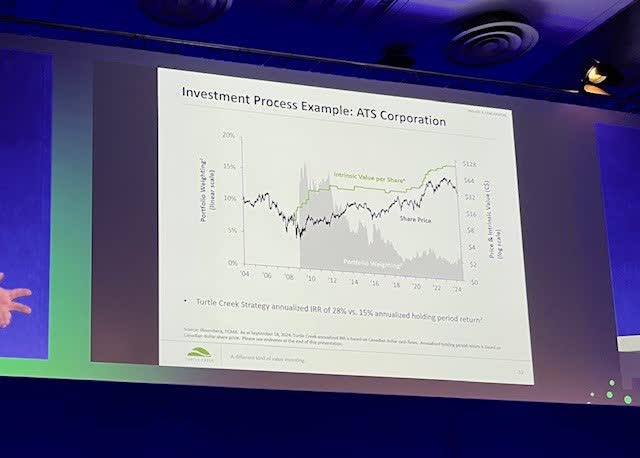

ATS Corportaion

A Canadian company active in global automation has a market capitalization of 3.6 billion USD and is listed on the Toronto Stock Exchange.

It’s cheap today. The company has massive contracts with GM, but the contracts have slowed down, resulting in share price weakness.

Buy and hold strategy would result in a 15% annual return vs our 28% in buy and optimize

FII

William Low of Nikko Asset Management

Seeing further in Changing Years.

Low joined the Nikko AM Global Equity Team ten years ago. He has been in asset management for 37 years.

We focus on real cash flow to investment CFROI

We invest in companies that can improve returns and over-perform

Average companies have 6% CFROI; we aim to invest in top 10% of companies on a CFROI basis with CFROI above 16%

High margin of safety through strong balance sheet and valuation support

Examples of our investments:

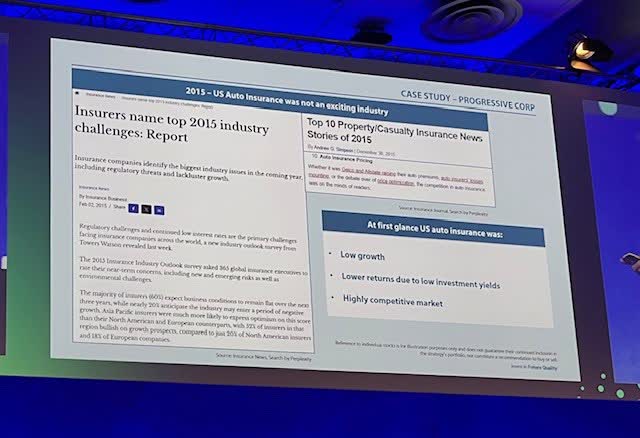

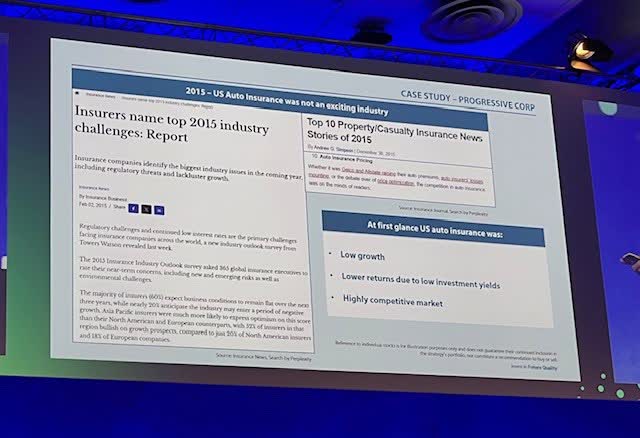

Progressive Corporation – Better use of data resulted in superior growth

FII

Polamar – US mid-cap specialized insurer

FII

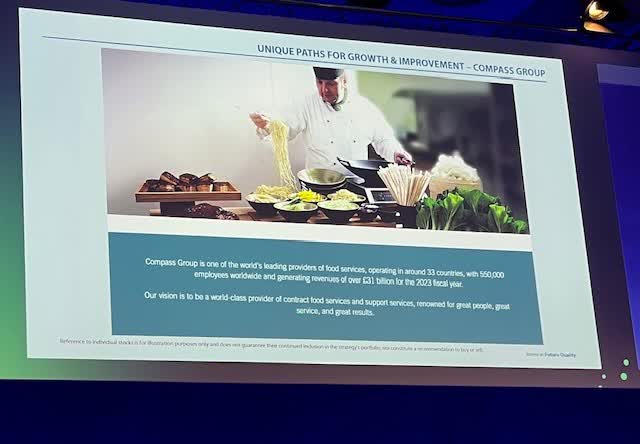

Compass Group – a leading catering global company

FII

Steven Yiu of Blue Whale Capital

Yiu is the Lead Manager in Blue Whale, a long-only global fund focused on large-cap stocks in developed markets. The firm has 1.5 billion USD under management.

– We look for Megatrends – focus on digital transformation

Technology is now 40% of the funds; we are looking for other megatrends too

During the 2020 pandemic – we bought digital transformation

In 2022, we exited the majority of the names from the slides

We invested in Nvidia

A list of current Megatrends and his investments is below

FII

META – has the most data about consumers – they know more about us than anybody; with AI, there will be more personalized advertisements. Meta should benefit strongly from AI-targeted advertising.

We believe Meta is the most promising of the Magnificent 7

We do not know which megatrend from our slide will be as dominant as AI, but we would like to be exposed to them

We have exposure to the semiconductor industry through Land Research and Applied Materials – we are believers in a megatrend in silicon sovereignty, we are trying to be exposed to derisking from Taiwan to the Western world

AI has caused 20% to be in semis – it is growing strongly, and we believe this will continue

Fireside chat with James Anderson – Lingotto Investment Management

Anderson was a partner at Baillie Gifford from 1987 to 2022. He lead their flagship fund until his departure. Anderson is considered one of Europe’s most successful investors.

The stock market has historically been dominated by a small number of winners.

Seventy companies have created almost all value creation since 1995. The concentration of value creation increases with time

One should focus on trying to find these biggest winners

There are common characteristics of these winners, and these are characteristics are predictable

More complex than finding the right companies is to stick with them when they have challenges

AI – people still underestimate how big the winning companies can be

AI is not about cheating on student essays; AI will help us to resolve the issues we face today in human biology and many other areas.

We will see ten trillion dollar company in the foreseeable future – within five years.

AI – robotics will be a critical area of new technology development. We need to wait to see who is likely to be dominant in this area and invest very heavily in it.

Climate tech is exciting. Most companies in this space are still in private hands.

Europe is lacking in innovations.

Chinese companies like BYD are no more subsidized than their European peers. However, BYD had to fight through a much tougher environment than its European peers. Their dominance comes from 30 years of innovation and investing.

The most difficult part of the investment profession is remaining loyal to the companies we invest in. We often leave investments too early.

We are now much less invested in China and I am sad about it. Your upside in the individual companies must be weighed against the risk of losing everything due to geopolitical tensions.

Most climate tech companies are still private companies. We are bullish on that theme.

We are increasingly focusing on large, successful companies – there is a higher chance they can successfully execute the plant.

I would be focused on healthcare and biotechnology — this sector is most affected by the financial industry’s short-termism. I would invest 75% of my capital in this sector.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

This is last week’s second instalment from the London Institutional Investor Growth Stock Conference.

Ideas from last year’s conference generated very substantial returns of up to 196%.

The first article focused on hedge fund presentations at the conference. This second article provides a brief summary of ideas we heard during the networking conference.

Conferences are about investment idea generation. We share the ideas in our two articles.

Luis Alvarez/DigitalVision via Getty Images

The third year of the Quality Growth Investor Conference brought interesting investment ideas and several investment conceptual concepts.

Around 200 institutional investors attended the presentation. The ideas from last year’s conference generated very substantial returns. I recommend reviewing the ideas in my first article.

Ideas from last year’s conference generated substantial returns.

FII

In our previous article, we included summaries of individual presentations by each asset manager. In this second and final installment from the conference, we briefly summarize the most interesting ideas from the networking during and after the conference. We present the reasoning given at the meetings. For a detailed analysis of the below ideas, you can search Seeking Alpha.

Talking to fellow investors generates equally interesting investment ideas as the conference itself. That is why we found the conferences valuable.

Based on historical experience with disrupting technologies, the biggest winners of AI will be different companies that are today’s winners.

Facebook is the prime candidate for growing its advertising revenues above its peers because Facebook knows more about us than its peers.

It isn’t easy to quantify potential Facebook growth. The quarterly revenues have not grown much recently, and Facebook still trades at a valuation of 1. 5 billion USD.

The valuation is around ten times its current revenues. Anybody can do a back-of-the-envelope calculation, and the value creation can be massive.

The presenters argued that we would see a 10 trillion stock within five years. Meta will be the prime contender in that race.

has a US-based market capitalization of around one billion USD. ERII is one of the few ESG companies that makes money.

ERII expects 2024 revenues to exceed 150 million USD. It has gross margins above 70%, no debt, and over 100 million USD in cash. ERII is profitable and cash-generating.

ERII is focused on desalination. Its technology saves around 60% of the energy consumed by desalination plants.

ERII dominates desalination. Its technology has a 98% global market share in large desalination plants. The company has not lost a project in seven years.

Now, ERII is starting to implement the same technology in other industries.

The first was wastewater processing. The business is growing by over 100% per year.

The next is industrial air conditioning and refrigeration. All developed countries signed up to replace existing systems that run on greenhouse gases with other, mostly CO2 systems. Those systems run at higher pressures and, therefore, need more energy. ERII technology can save 30% of energy costs in those systems. Tens of systems are now installed in supermarkets globally for customers to try.

This segment can potentially change ERII’s fortunes in the coming years and multiply its revenues over the next five years.

is an LNG tanker company listed in the US with a market capitalization of 150 million USD.

The company operates six LNG carriers.

The company’s vessels have locked into long-term contracts with an average remaining contract period of 6.4 years.

The total contractual backlog is over 1 billion USD.

DLNG has paid out debt significantly. Current debt to EBITDA is below 3x.

On the last call, the company announced that it would announce its capital allocation strategy on the next call – see the last slide of the presentation.

DLNG will most likely announce dividends. The company can pay 0.75 USD per share, compared to its current share price of 3.8 USD.

If they paid 100% of what they could pay, this would represent a 20% dividend yield.

Stocks that start paying dividends to outperform. DLNG should be an excellent example of this.

See below the latest investment presentation by DLNG from their website:

is an Australian defence company that is a global leader in drone defence. Its marketing logo is “Nobody kills drones like EOS.” In Australia, it has a market capitalization of USD 250 million.

War Ukraine has shown how drones have become the New weapon for all future wars.

EOS is the leader in shooting down drones with bullets and lasers.

Shooting drones with Bullets and Lasers is much cheaper than shooting them with rackets. The racket costs 100,000 USD, and the bullet costs about 100 USD.

It is listed in Australia, where investors are not exposed to the daily news on drone fighting and do not appreciate it.

The company is run by a respected industry veteran who was the head of Rheinmetall’s defence business and brought several Rheinmetall colleagues with him.

EOS is a former spinoff of the Australian Laser Institute. Australia spent 1 billion USD developing lasers for defence purposes.

EOS has production facilities in the US, the Middle East, and Australia and is now looking for a European production site.

EOS trades at 50% discount to European peers on Price to backlog basis.

EOS is growing strongly, generating cash, net cash positive and selling globally.

See below the latest investment presentation by EOS from their website:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

We visited Berenberg & Goldman Sachs German Corporate Conference in Munich on 23-25.9. One of the most interesting presentations was by Peter Oppenheimer, Chief Global Equity Strategist & Head of Macro Research EMEA, Goldman Sachs International.

The summary of his presentation is below:

We are expecting everywhere inflation to reach central bank targets by mid-year 2025

The rates will be going down as well, but not to the levels we have seen after the financial crises

Governments are not interested in reducing debt – government debt will grow further both in EM and DM. So, longer-term rates will be a little bit higher.

This will be a positive environment for equity markets in the US – the cycle is positive, but some structural parts are challenging.

Firstly, the current valuations are high compared to history, particularly in the US, where it has stood at the top of its valuation range over the last 20 years on PE basis.

The US market is worth 200% of the US GDP. That has not happened before.

The US is roughly 70% of overall global capital market capitalization. The rest of the world is only 30%.

Some of it is due to the technology companies in the US. The top five US companies represent 20% of global equity values.

Even without tech – the US is still expensive by historical standards

You have seen quite a lot of good news priced in terms of lower interest rates.

Secondly, the margins have peaked, and revenue growth will drive the valuations.

US markets might be rising, but slower than in the past months, as the growth will be driven by revenue growth. Revenue growth is linked to nominal GDP. So, the revenues and the valuations should grow in line with slower GDP growth.

Outside the US, markets are cheaper, but that has been the case for a long time.

We think there are selective opportunities to diversify

There is a big market divergence from 2010 after the financial crises ended – the US grew much more strongly than other countries did

It happened because the US managed to achieve much higher profit growth

The success of US tech was due to the scalability of capital-light businesses. Now, they have already been transferred to capital-heavy companies. This year, they invested 90 billion USD.

The question is whether they will be able to grow further even with capital-heavy balance sheets.

Compared to the US market, Europe is at the lowest levels since the 90s at 35% discount on a PE basis.

Part of it is due to the heavy weighting of the tech sector in the US. Even if you remove the tech sector, the discount is still historically the highest.

European markets have performed well this year.

Many of the European companies are benefiting from the global business they have.

Dax index performed well and was able to disconnect from the slow German growth. German domestic business index was the only negative index in Europe.

The lowest valuation in its history is now in the Chinese and German domestic markets.

China is at the lowest historical PE levels. The Chinese market has been weak, and the Chinese administration has heavily disadvantaged its technological sector.

Germany’s domestic-focused stocks are now at its historical lowest – there are some good opportunities in German mkt and Europe.

Recommendations:

Firstly, in the US, we would look at midcaps; they react to lower rates, and the valuations are cheap. Macro is still supportive, US macro relatively healthy, healthy labour markets and decreasing rates – in this environment, the markets have consistently grown.

Secondly, we would look at global nontech growth compounders – we have a collection of those.

Thirdly – we diversify geographically; we like China; the valuation is very cheap, and there are some opportunities there.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Last week, we spoke to the company, analysts and South Africa insiders. Below is my understanding of where Africa Energy stands.

On Monday, Africa Energy announced that its partner in Block 11B/12B, CNR, intends to withdraw from the block and that the block operator, TotalEnergies, is considering its options. The Africa Energy share price reacted by dropping 75% on large trading volume. Investors are speculating that TotalEnergies will also withdraw after a Bloomberg article quoted a PetroSA source saying that TotalEnergies had already notified the government of its intention to withdraw.

Over the last two years, the South African government has failed in the energy sector with rolling blackouts and very little progress on offshore oil and gas exploration, especially compared to Namibia next-door. The South African Energy Minister Mantashe (recently reappointed) has been promoting the gas transition publicly, but he is clearly in bed with the coal lobby and has made no progress with oil and gas, even getting tied up in court with Shell and Impact over foreign-funded environmental protests to offshore exploration. Moreover, the President has still not signed the energy bill that was approved by the parliament several weeks ago and has been promised for about a decade. Finally, TotalEnergie’s application for the Production Right for Block 11B/12B, filed more than two years ago, has still not been granted, delayed by TotalEnergie’s concerns about protests on its environmental impact assessment, now due August 30. CNR clearly lost patience, and the asset was never really core to their mainly Canadian oil business. But is it core to TotalEnergies?

There are positive signs — the new Democratic Alliance (DA) coalition government should be more friendly to business and encourage foreign investment. But mainly the Minister of Electricity role now also includes Energy taken away from Mantashe, who retains Mining and Petroleum. Taking away Energy from Mantashe, might be quite positive. So reason may prevail to help the Block 11B/12B project.

I think it can play-out in two ways:

1. TotalEnergies is bluffing and remains operator of the block with all the noise about withdrawing just a negotiating tactic to put pressure on the new South African Government to finalise the gas off-take agreement and approve the Production Right; or

2. Everybody withdraws from Block 11B/12B except Africa Energy / Main Street, which will get 100% of the block for free. AEC’s largest shareholder is now Impact, which is controlled by Johnny Copeland, a white South African billionaire who is a former member of Parliament and now CEO of HCI, a black-empowered South African business conglomerate focused on hotels and casinos. He is very well-connected in SA and is the best placed to execute the project long-term. I guess this is why the Lundin family passed the baton to him and stepped away from AEC. It may take a bit longer than expected, but sources say Copeland sees Block 11B/12B as a patriotic mission to supply South Africa with much-needed domestic gas. A 100%-stake in Block 11B/12B should motivate him to achieve this.

At the moment, I believe option 1 is more likely. TotalEnergies declared last week to the South African government that they are in fact staying in Block 11B/12B, no doubt to buy government goodwill for their efforts to explore for oil off the West Coast of South Africa. They plan to drill soon in the offshore South African blocks on trend with their large discoveries offshore Namibia in the Orange Basin where Impact (Johnny Copelyn) is their partner.

In the article published yesterday, Thulebona Nxumalo, an official at the National Energy Regulator of South Africa is quoted:

“We contacted them (TotalEnergies) to try and get clarification about what is it that is happening there. And what they indicated is that they had initially planned to exit but following engagements that they’ve had with government and other stakeholders, they’ve decided to stay. So, it sounds like they will be staying for now on that Brulpadda project,”

Of course, this is a statement that may change in the future.

In summary, we believe the AEC investment is not lost. We think the Block 11B/12B gas development will happen. There is a lot of gas there, and South Africa clearly needs the gas. If TotalEnergies stays, it will happen faster. If they do not, it will take more time, but it could happen with more upside for AEC shareholders under Johnny Copelyn’s lead.

The risk I see is Russian involvement. If Gazprombank invests in the nearby Block 9 infrastructure with PetroSA, no one will be able to use it because of US sanctions. I have no information that this is what is happening, but it is a risk. Last year, Gazprombank won a tender for financing the reconstruction of the Mossel Bay gas-to-liquids plant, which is now shut-down due to lack of gas feedstock from the depleted Block 9 offshore fields. The tender was widely criticised and based on suspicious conditions whereby all other bidders were eliminated (see our previous blog post on this). After public criticism, the tender went quiet, and it could be cancelled under the new coalition government. The final investment decision was due by April, but nothing has been announced.

Conclusion

The best case in terms of timing is that TotalEnergies stays, gets the Production Right by the end of the year, and the whole project moves forward. Africa Energy is a great investment in that scenario, especially at today’s depressed share price and with all its funding secured from shareholder loans. If it goes back to 3 SEK, where it was trading when the Production Right application was filed, you are looking at 15 times return!

The alternative is that South Africa continues to stall the gas price negotiation or Gazprombank stays involved in the block next-door, forcing a more expensive development that cannot rely on the Block 9 infrastructure. That would result in everybody withdrawing except Africa Energy/Main Street, which would control 100% of the block for free. In that situation, we still believe that the project will happen, but it will take longer.

We have been buying Africa Energy stock last week.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

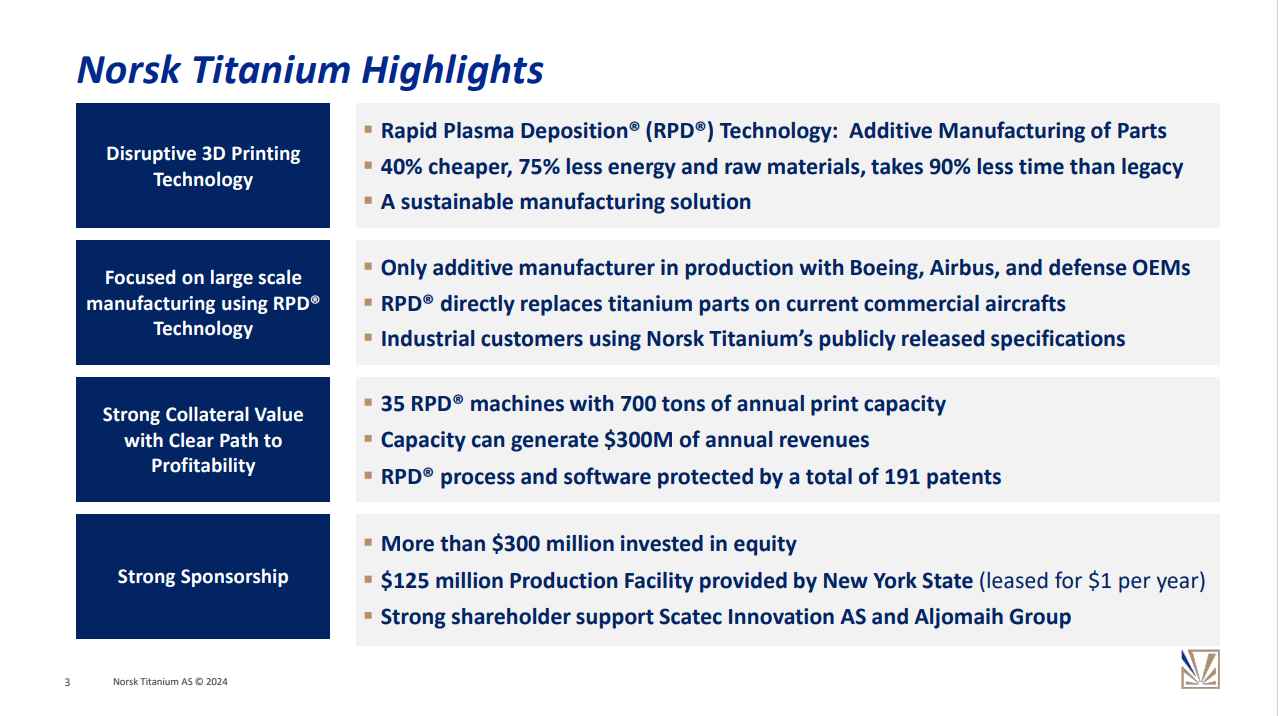

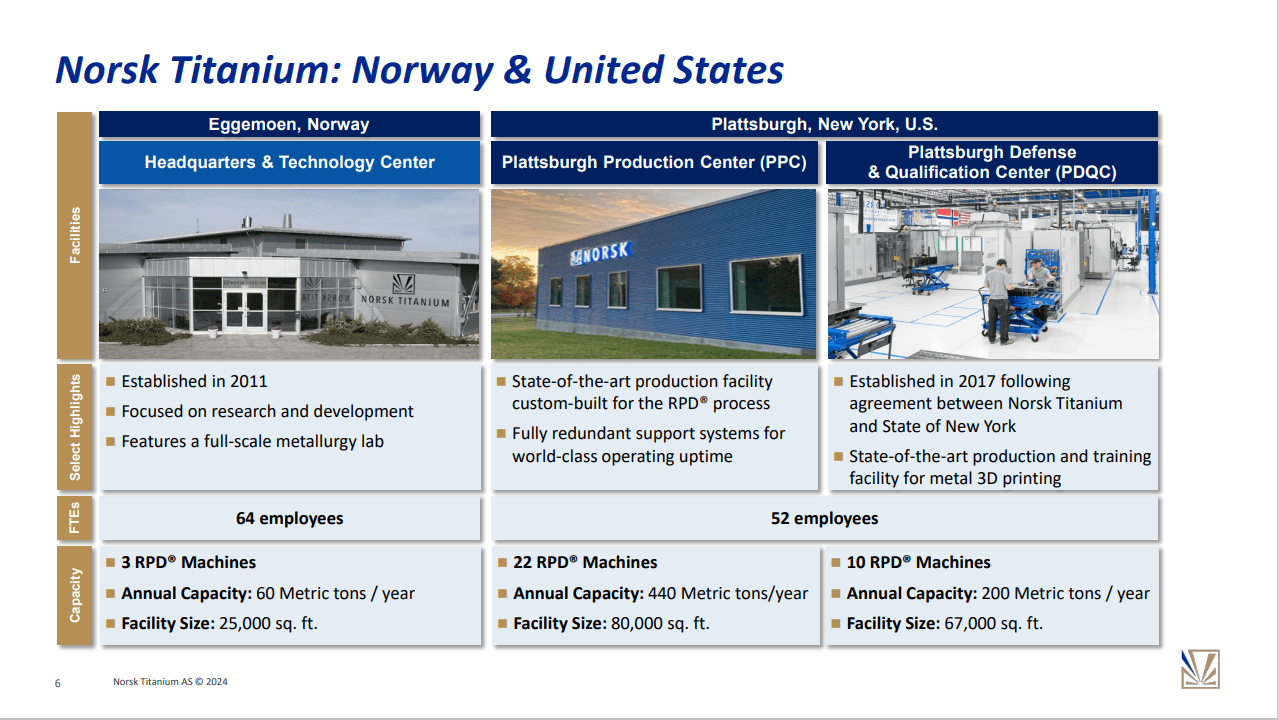

Norsk Titanium is the global leader in Rapid Plasma manufacturing of titanium parts for aerospace, defense, and chip industries.

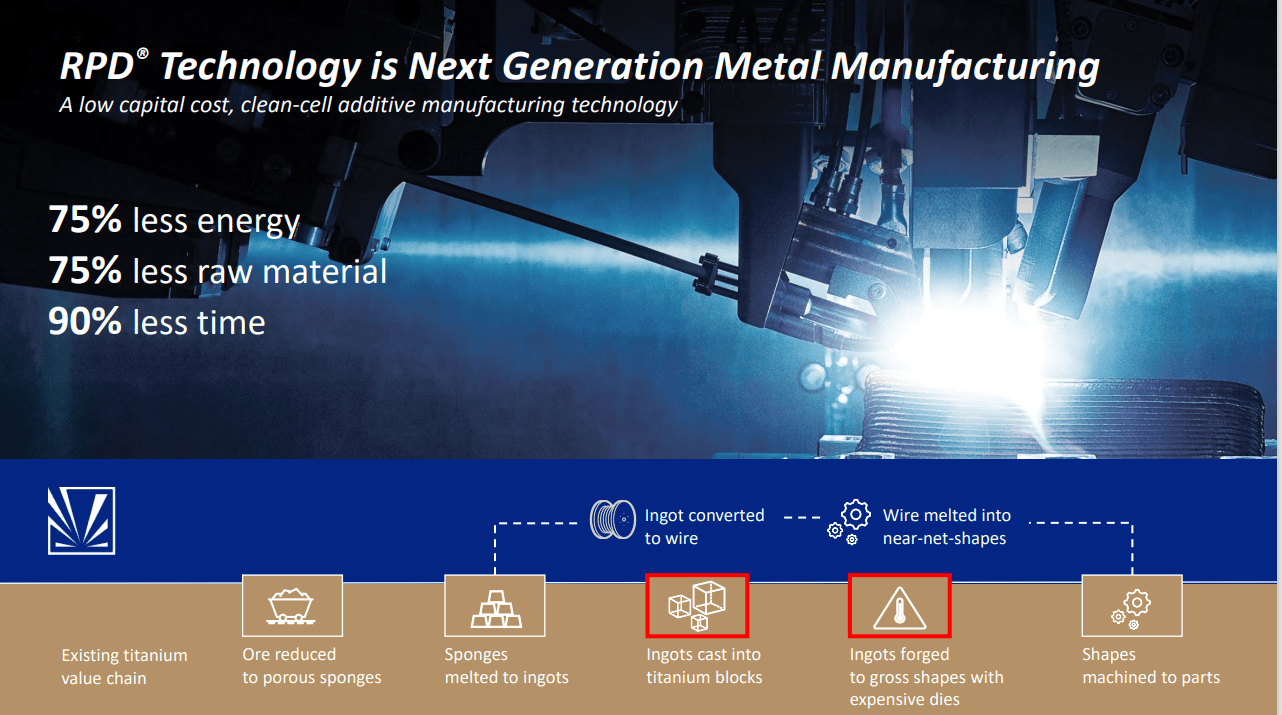

The company has invested $425 million in its proprietary Rapid Plasma Deposition technology, which reduces material and energy costs by 75% versus currently used production methods.

Norsk Titanium has partnerships and contracts with Airbus, Boeing, Northrop Grumman, and other major aerospace and defense companies.

Exponential revenue growth should multiply the stock price over the coming two years.

Norsk Titanium(OSE: NTI) and (OTCQX: NORSF) s the global leader in additive manufacturing (3D printing) of Titanium parts for the aerospace, defence, and chip industries. Their business involves producing aerospace-grade titanium components using a proprietary process called Rapid Plasma Deposition (RPD).

Norsk Titanium

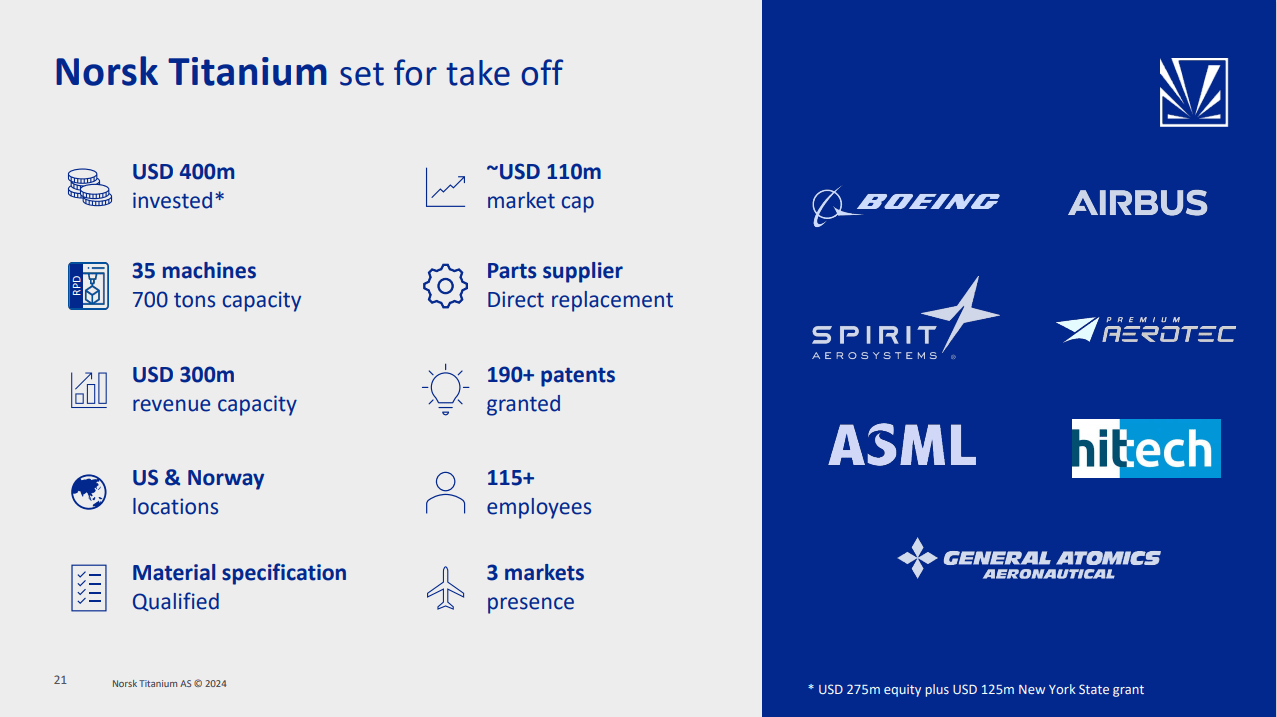

Norsk Titanium’s main production is in New York State, and its research centre is in Norway. The company is listed on the Oslo Stock Exchange with an NTI ticker and in the US with NORSF ticker. A US listing is on the cards possibly for the next year. The Company has a USD 140 million market capitalization and no debt.

Norsk Titanium invested USD 425 million into its technology – USD 300 million of shareholders’ capital and USD 125 million of grants from New York State. The company has 191 patents for its technology.

Norsk Titanium has 35 RPD machines with 700 tons of annual production capacity, which can generate USD 300 million at full capacity. The company has 115 employees in its two locations.

Norsk Titanium

Technology

Norsk Titanium’s proprietary RPD technology enables the company to produce high-quality, complex titanium parts with significant cost and time savings compared to traditional manufacturing methods. The technology consumes 75% less energy, 75% less raw materials and 90% less time vs mainstream manufacturing techniques.

RPD technology allows them to compete effectively in the aerospace industry, where titanium components are crucial but traditionally expensive.

Norsk Titanium

RPD is a disruptive technology

Norsk Titanium’s RPD technology is a disrupting technology that should disrupt current producers. RDS gives them a competitive edge over other manufacturing methods. Their process reduces material waste, production time, and costs, making them an attractive option for aerospace companies looking to streamline their supply chain and reduce production costs.

We believe RPD is the disruptive technology that will replace the current production methods. Norsk Titanium is the global leader and will most likely capitalize on this trend.

Focused on Aerospace, Defence, and Commercial

Norsk Titanium is concentrating on three revenue-generating areas. The biggest opportunity is the Aerospace industry, where regulation and licensing, which take many years, limit competition and, therefore, allow for better pricing.

Aerospace – Norsk Protected by Regulatory Barriers to Entry

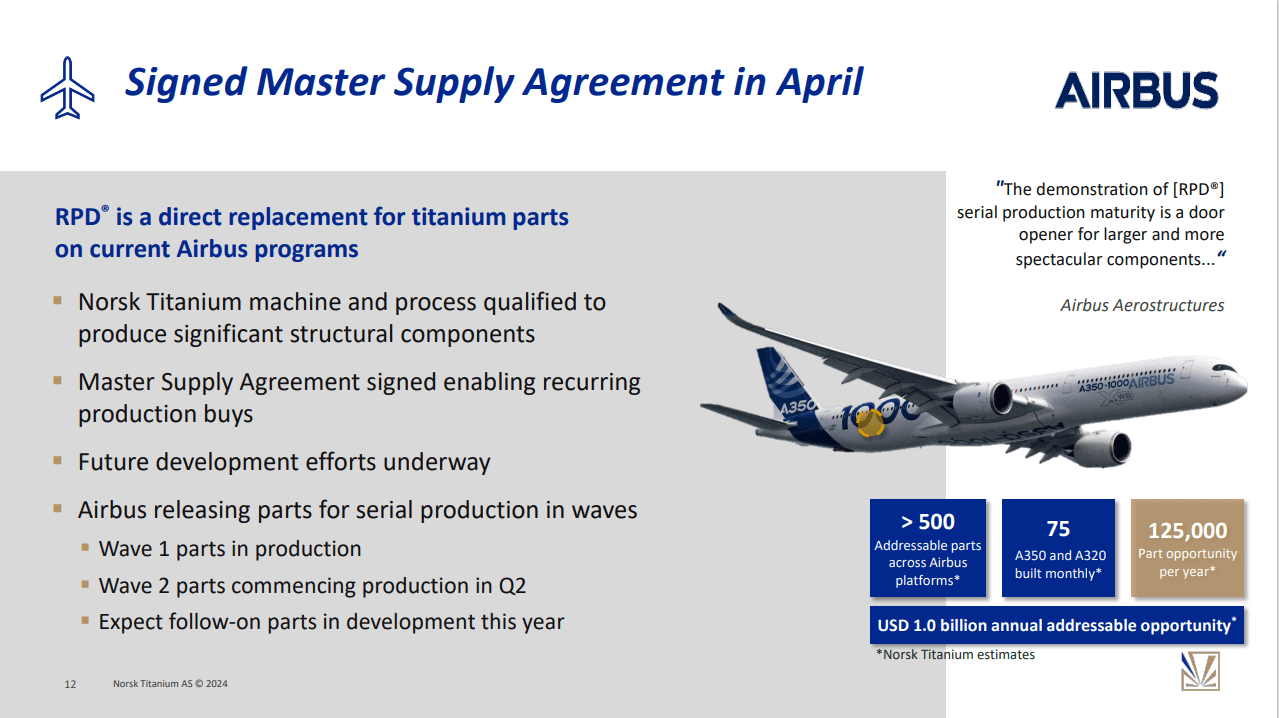

The major barrier to entry is Norsk Titanium’s partnerships and contracts with the major aerospace companies. These partnerships validate the company’s technology. Aerospace is a highly regulated industry. It took Norsk Titanium over seven years to sign the Master Supply Agreement with Airbus. That milestone was achieved in April, resulting in a series of Airbus production orders.

Norsk Titanium

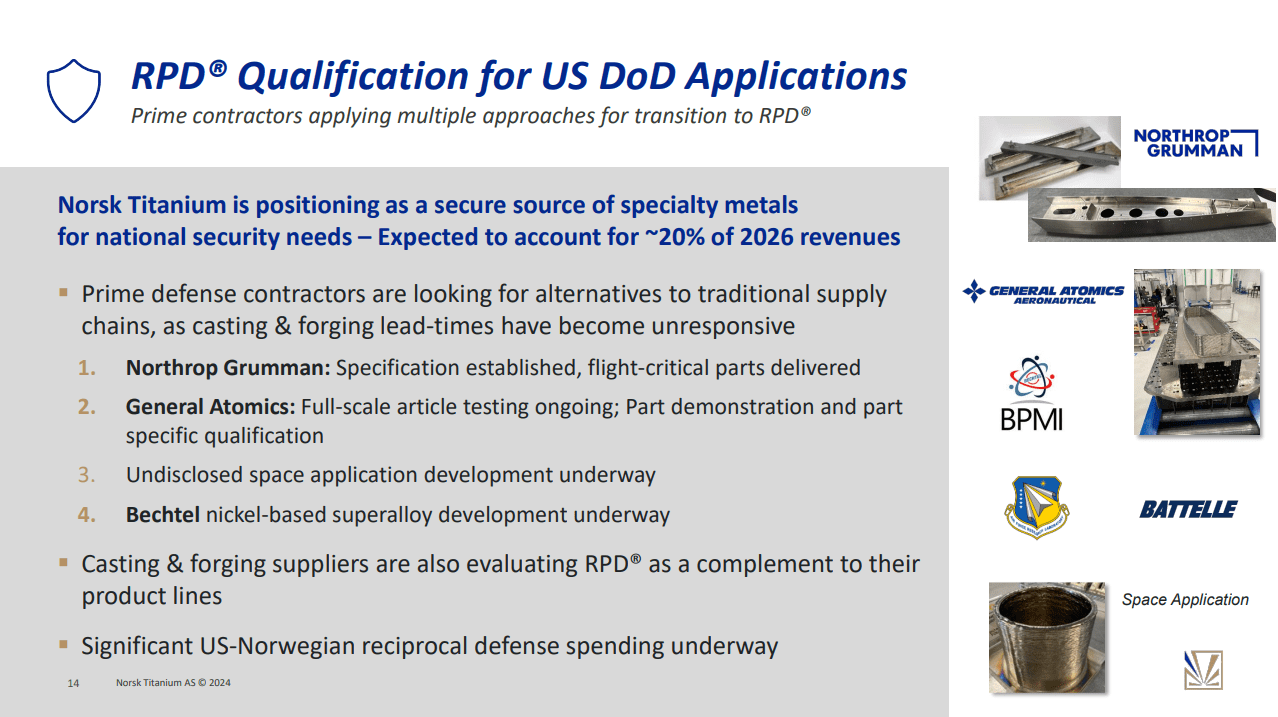

Similarly, in April, Norsk announced it had signed a Production Agreement with Boeing. The agreement started a direct supplier relationship between the companies, enabling Norsk Titanium to be a tier-1 supplier to the Boeing procurement system.

The most advanced is the cooperation with Northrop Gruman, where flight-critical parts were already delivered by Norsk Titanium. Production of parts for General Atomics, and others is underway. For Bechtel Norsk Titanium is developing a whole new nickel-based material, which is a big step forward for the company’s offering.

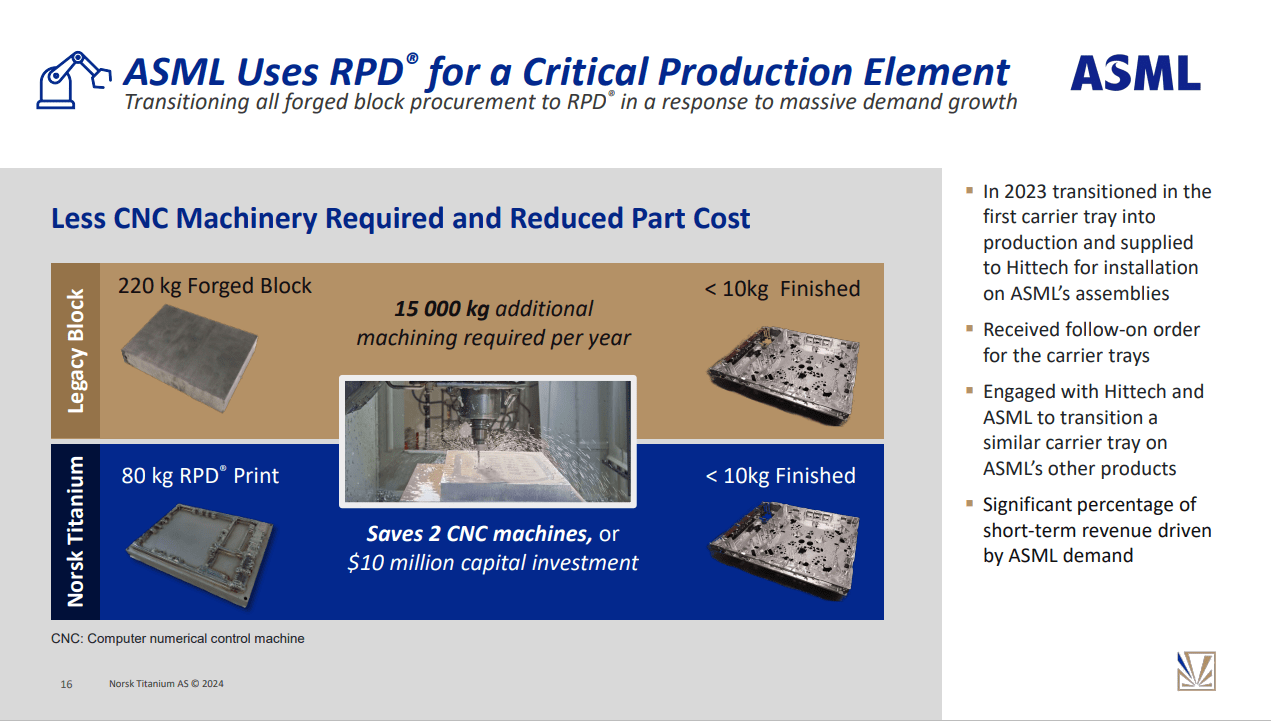

Norsk Titanium supplies Titanium components to ASML Holding, a Dutch company and one of the world’s leading suppliers of photolithography systems used in the semiconductor manufacturing industry. Norsk Titanium’s relationship with ASML is through ASML’s tier-one supply chain partner, Hittech. Norsk expects to double its sales to ASML this year.

Norsk Titanium

Strong Revenue Growth in the Coming Years

The new contracts with Airbus and Boeing, significant milestones for Norsk, have paved the way for substantial revenue growth.

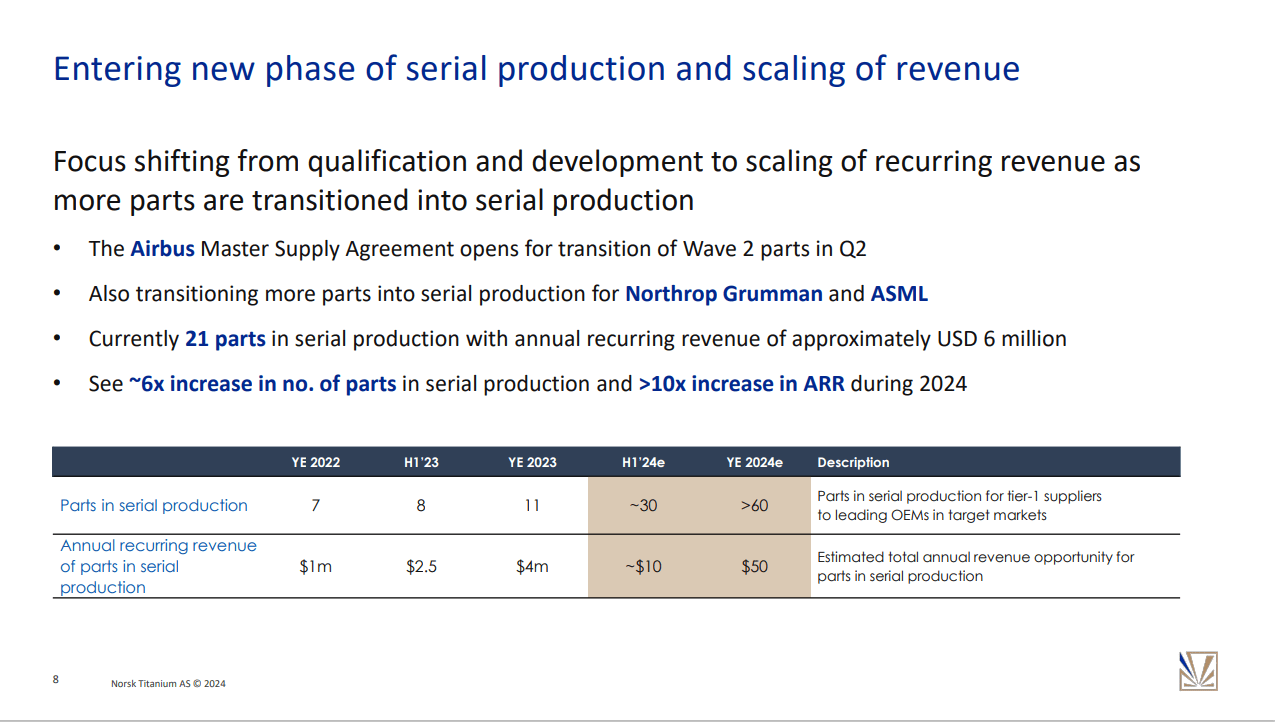

At the end of 2023, Norsk was producing 11 parts for different customers (each part may be made in hundreds or thousands of pieces)

At the end of April, the number has increased to 21 parts and

by the end of 1H24, Norsk expects to have 30 parts in production.

Based on the contractual negotiations, Norsk is guided to have more than 60 parts in production by the end of the year.

The recurring revenues would increase from USD 4 million at the end of 2023 to USD 10 million at 1H24 to USD 50 million at the end of 2024.

Norsk Titanium

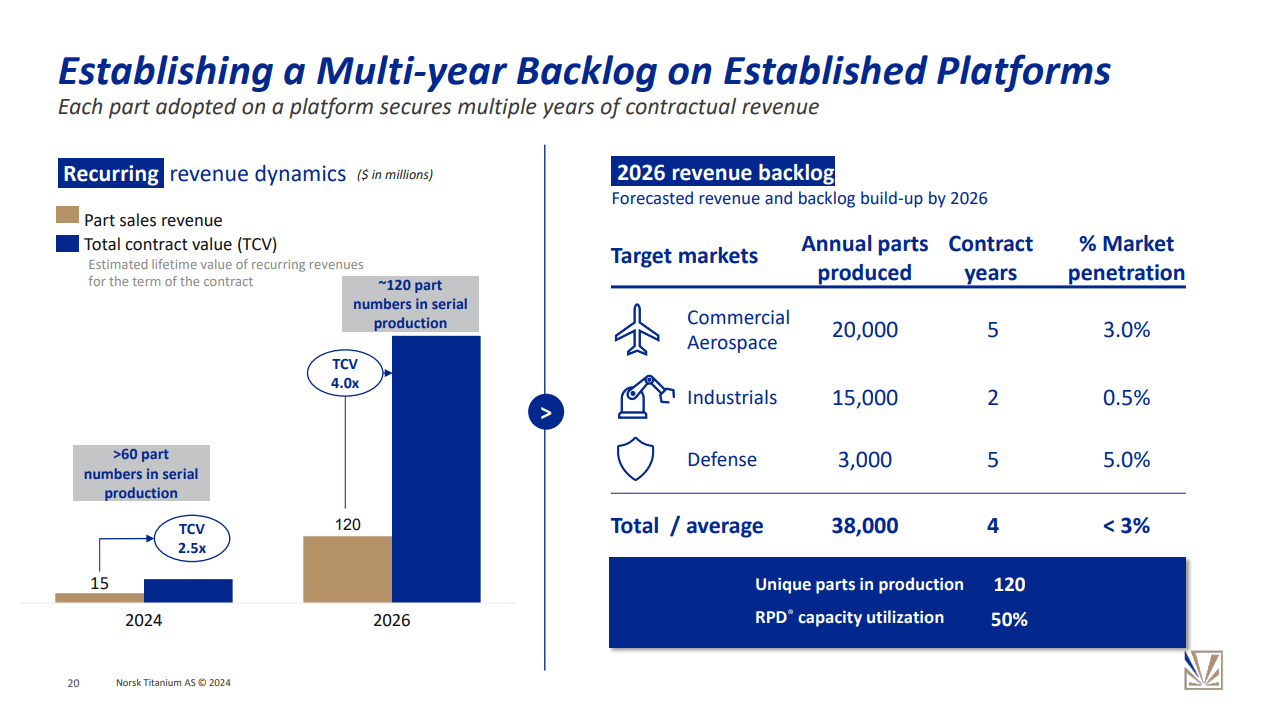

Based on its relationship with Airbus and Boing, Norsk is guiding to be producing over 120 parts in 2026 and expects recurring revenues to reach USD 150 million in that year.

Norsk Titanium

Valuation

Norsk Titanium’s market capitalization is currently around USD 140 million. That is just one-third of the USD 425 million (USD 300 million in equity and USD 125 million in grants from NY state) invested in the technology. The reason for the discrepancy is in the length of the certification process. The Airbus contract took so long that many investors lost their patience and drove the share price down. That created this opportunity.

Valuation of Norsk Titanium when producing at full capacity in 2028

Assuming revenues of USD 300 million and an EBITDA margin of 30%, you get an EBITDA of 90 million. At that stage, the company would be trading at least 10 times the EV/EBITDA multiple. As Norsk has no debt and is fully funded to break even, the company should be valued at at least USD 900 million—6.5 times its current market capitalization.

Norsk Titanium valuation based on its 2026 USD 150 million revenue guidance:

Revenue guidance for 2026: USD 150 million

EBITDA margin guidance in 2026: 30%

EBITDA in 2026: USD 45 million

Assumed debt in 2026: 0

Assumed EV/EBITDA multiple: 10

Enterprise value in 2026: USD 450 million

Current Capitalization: USD 140 million

Upside: 320%

Current share price: 2.7 NOK

Target share price: 8.7 NOK

The above does not consider the issued warrants, which can be converted into shares later this year. The warrants do not change the upside picture materially.

A material part of this upside should be realized this year.

Conclusion

Many investors lost patience with Norsk Titanium due to the long wait for Airbus and other certifications and contracts. This created the opportunity. The agreements with Airbus and Boing have been signed; the orders are piling in, andthe story has been de-risked. Investors are returning, and the share price has a good momentum. The share price has increased, but there is still a three-time potential to reach 2026 targets. We should see a substantial price rerating this year.

Norsk Titanium

Link to the April Capital Markets Day presentation:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

On December 6, 2023, we published our Golar LNG idea here. We predicted several catalysts that should drive the stock up significantly. The rumours related to one of the catalysts drove the share price up 10% yesterday. An indication of upside potential.

Summary from our original post

Golar LNG builds, owns, and operates marine infrastructure for LNG liquefaction and regasification, with a market cap of $2.3 billion.

Golar’s assets include two FLNG vessels.

The first vessel, Hilli, is currently working for Perenco. The contract ends in 3q26. The new 10-year or longer contract would be a major catalyst for the stock.

Hilli is currently working on a 1.4mtpa contract vs. her capacity of 2.4mtpa. If the new contract is for the full capacity, the EBITDA could increase by 70%.

The second vessel, FLNG Gimi, arrived in January at the BP offshore field. Its operation in late 2024 will increase Golar’s EBITDA by 50% and potentially result in a dividend hike.

Strong catalysts in the next six months.

The investment case is supported by dividends and a USD150 million buyback.

Our idea is starting to play out – Hilli is rumoured to be in contention to service YPF off Argentina, driving to GLNG 10% up yesterday.

There has been some chatter/rumours regarding FLNG Hilli, which may see her go work for YPF off Argentina after her contract for Perenco in Cameroon is finished in 3q26. The new contract will be the major catalyst for the stock, as yesterday’s share price reaction indicated.

YPF stated in their 4q23 earnings press that they want an external FLNG for 1-2mtpa from 2027, fitting well into the expiry of Hilli’s current contract. That fits well for Hilli.

Hilli is currently working on 1.4mtpa contract vs. her capacity of 2.4mtpa. Argentina rumours fit well (also fits well with GLNG mgmt. comments on the 4q23 earnings call regarding Hilli not being relevant for further Africa work at this time).

If this is correct, it helps de-risk the Hilli-case and provide visibility and long-sought for news flow. Gimi, GLNG´s second FLNG vessel, is set to commence commissioning in the coming months.

Once Gimi is operational, we believe the fixed quarterly dividend will rise and that parts of the net proceeds from the Gimi refi will be paid out as dividends.

The story is starting to play out, as predicted. Stay tuned for more.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.