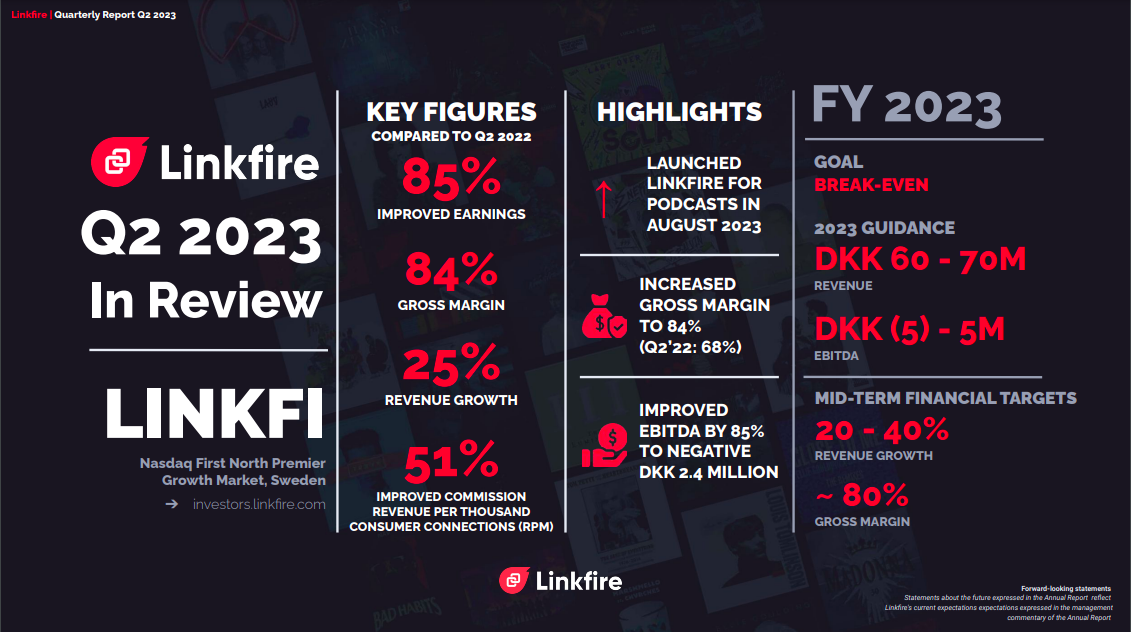

Q2 are seasonally the weakest quarters for Linkfire. Despite that the company delivered strong – its best Q2 ever, +25% above 2Q22. Other metrics show strong improvements on all levels.

Linkfire produces the best investor materials in Scandinavia. See yourself:

Linkfire’s one slide summary of 2Q23:

Linkfire two minutes video summarising the business and 2Q23:

Linkfire 2Q23 resources (webcast, presentation, detailed report)

Why we like Linkfire:

- Dominates one global business segment – smart links for sharing music on social media. All global music stars use Linkfire.

- All major music streamers work with Linkfire (Apple, Spotify, Youtube…)

- Linkfire just announced it is entering a new business segment. It enters in partnership with Apple Podcasts. The new segment is not priced in.

- Linkfire is growing strongly – 56% last year. Our base case is similar growth rate this year

- Creative management – we are one of the top five investors. We talk to Linkfire management regularly. They are very strong.

- The CEO of Band Lab became 4th largest shareholder in Linkfire. Band Lab is the largest a online Cloud Digital Audio Workstation tool for creating music with over 60 million users, including professionals like Dr. Dre or Jay-Z.

- Profitability is the main goal for 2023. With the current cost base, the revenues need to grow only by 22% above 2022 to reach profitability.

- After partnering with Amazon Music and Apple Music, new majors partnerships should be announced in 2023.

- Linkfire is cheap – Linkfire is 80% down from its IPO. It trades at 1.7xRevenues. It should trade at least 5 times.

- Plan to realise the value – the company talks about delisting from Sweden and IPO in the US to achieve a higher valuation.

We think the biggest opportunity for this year would be to look for solid companies, whose share price was beaten up severely last year. Linkfire is the best example of such investment case.

Subscribe to Blog via Email

.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Share this:

Related

Linkfire – notes from the call with the managementNovember 19, 2021Liked by 1 person

Linkfire – Record Quarter from Danish IPO of the YearMay 27, 2022

Pareto on Linkfire: Amazon Music deal gives us confidence in 2022 guidanceMay 3, 2022