This is the second installment of our best ideas for 2023. Mintra more than doubled this year, but is still 50% below its IPO price. Sparebank and Pareto analysts have Mintra as one of the top ideas. It is still one of the cheapest against peers, nicely profitable and cash generating, net cash positive, new deal accelerates growth from 1Q23 and two its largest shareholders are most likely about to take Mintra private. The Norweigan take private premiums exceeded 60% this year. Doubling candidate for 2023.

Mintra introduction

- Mintra provides e-training courses for crews on ships and energy platforms

- Mintra was hammered during Covid times as crews stopped rotating. Mintra should be booming now, as shipping and energy have the best times ever

- The share price is up 100% from February low, but the growth of the business will be reflected only with a delay for reasons described below.

- Mintra is reporting on semiannual basis. The 1H22 revenues did not reflect the growth

- Mintra is generating FCF of 80m NOK per year

- Market cap is 900 mil NOK; they have net cash of 100 mil NOK, EV is 800 mil Nok

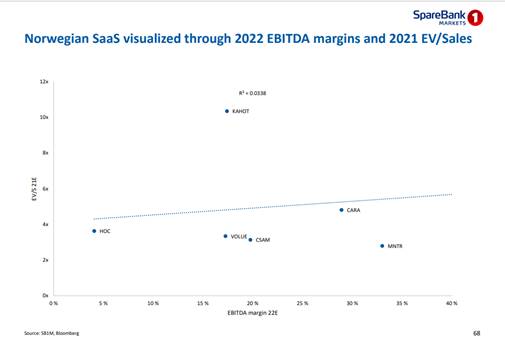

- Mintra is trading at roughly 3.5 times revenues. Mintra is one of the cheapest stocks in the Scandinavian peer universe.

- Mintra has one of the highest EBITDA margin while trading at one of the lowest EV/Sales multiples vs peers.

- Mintra was listed in late 2020 at 9.7 NOK. The share price is up 100% from February low and trades at 5.0 NOK.

- Mintra shares is accumulated by two Scandinavian investors – Tadjur and Ferd, that own 42%. They are buying stock in the market. They usually work with private companies. Both analysts that cover the stock believe they will take Mintra private.

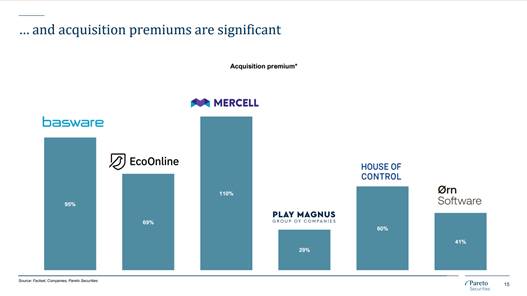

- Pareto securities showed a slide at this week’s conference that shows that the average going private premium in Scandinavia has been over 60%. This indicates a return potential for the stock

My discussion with the company

The shipping and energy boom is reflected with a delay:

- On some of the contracts, the increase in the use is reflected only with a time delay. The largest customers such as Shell or BP, sign annual contracts, which are flat-fee all you can eat contracts. Such contracts are a minor part of Mintra’s revenues. The increased use of the Mintra e-learning platform is reflected only when the contract is renewed.

- The contracts with other customers have a flat access fee + fee per use. Such contracts reflect the increased traffic faster than the above fixed annual contracts.

- Mintra is gaining new customers. They gain approximately 60 new customers in 1H23.

- The most significant new customer is BSM which operates 650 vessels. Currently, Mintra clients operate 1700 vessels. Such contracts are charged by Mintra per vessel basis. The BSM deal should therefore increase Mintra client fleet by 40% – the maritime revenue increase should be by a similar level. This will be reflected in Mintra numbers during 1Q23.

- The e-learning space has been dominated by three players. Mintra, Netvision (acquired this year by Ocean Technologies), and Adonis. Adonis is losing market share due to its technology handicap. Mintra gained several customers of Adonis recently. The industry is likely to consolidate.

- Mintra two largest shareholders are industrial holdings Todjur and Ferd. They control 42% of Mintra. They are buying in the market. They mostly work with private companies. They wanted to buy Mintra even when it was a private company. It is assumed they will take Mintra private.

- The CEO has 2 mil shares in Mintra; he is in the same boat as the other shareholders. The other shareholders are unlikely to support the buyout unless it is above the IPO issue price.

- The Norwegian buy out premiums this year have been very significant. See a slide from Pareto presentation from early November 22.

In summary:

- Mintra is cheap vs peers while having one of the highest EBITDA margin vs peers

- Mintra is profitable and is generating strong CFs

- Mintra growth is about to accelerate – just the BSM contract will increase the fleet Mintra provides trainings to by 40%. Onboarding starts on 1/1/23.

- All analysts that cover the stock believe that the two largest shareholders will take Mintra private. Average take private premiums exceed 60%.

- The stock should rerate further in the next 12 months. Either due to the growth acceleration and price re-rating or due to being taken private. Both scenarios should be very good for its shareholders.

Our trading strategy

We are fully invested in Mintra up to our individual stock limit. We believe that 2023 should be the year we exit Mintra. Our base case is the stock should double.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.