- HydrogenPro is Pareto´s top hydrogen exposure idea

- HydrogenPro booking its first revenues from the USD >50m Mitsubishi order.

- 1000% revenue growth in 2023 – Pareto estimates 2023 revenues at 64 mln USD vs last year 6 mil USD. In H2’23 FID is expected regarding the DG Fuels project and expansion announcements as further triggers.

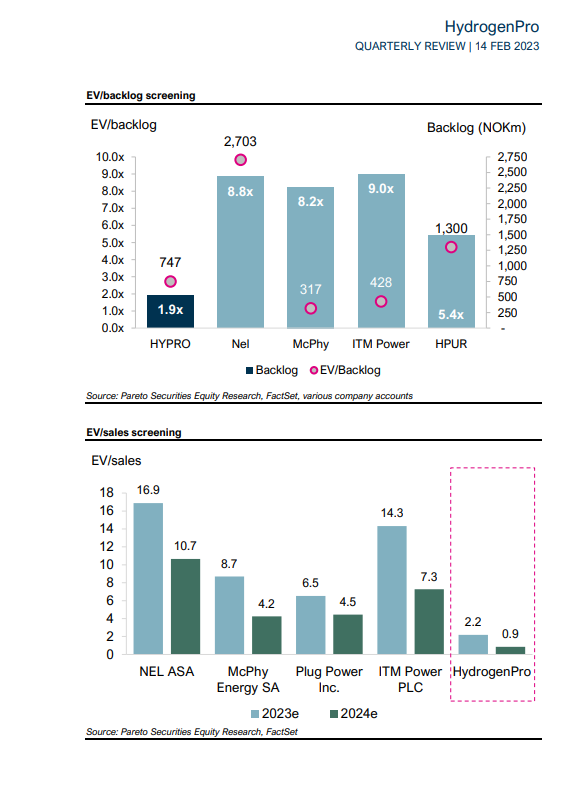

- HydrogenPro trades at 2x/1x EV/sales on our 23E/24E, vs hydrogen peers at 12x/7x, and EV/Backlog of 2x vs electrolyser peers at 8-9x.

Pareto research summary:

First revenues from USD >50m Mitsubishi order booked

HydrogenPro reported NOK 25m in Q4 revenues, of which ~14m from the ACES project (Mitsubishi) in the US. Its organization continues to grow which cause the higher cost base. The company completed tests of its electrolysers (world’s largest) which proved the readiness for large scale hydrogen production, although it is still working with Mitsubishi on some fine-tuning. The readiness for large-scale delivery was further underlined in Q4 with final upgrades on its China facility.

Small adjustments to estimates

We make limited estimate changes on the back of the quarterly report.

HydrogenPro reiterates that 90% of the USD >50m purchase order will be booked as revenue in 2023. Although it states a higher gross margin level on the contract than it has had in 2022 (22%), we keep our 20% estimate for now. The company expects FID on the DG Fuels’ Louisiana, US, project in the latter half of 2023, with the final stages of FEED being completed now. We have previously included revenues with full effect in Q4’23, but we now push these slightly and mainly include revenues from 2024 onwards which explains the drop in our 2023E revenues. The project has a value potential of USD >500m for HydrogenPro. With 100% off-take for initial production at the plant, DG Fuels is already looking at a second in Maine, US. Overall, we reiterate our main thesis, seeing solid growth prospects for HydrogenPro. We still include a NOK 250m equity raise to facilitate for the targeted manufacturing capacity expansions in 2023.

Still a top hydrogen exposure with further de-risking potential in 2023

HydrogenPro trades at 2x/1x EV/sales on our 23E/24E, vs hydrogen peers at

12x/7x, and EV/Backlog of 2x vs electrolysers peers at 8-9x. With the growth it

faces and further de-risking potential with delivering on the ACES order and a

massive DG Fuels potential, we find it to be an attractive hydrogen exposure. We keep our NOK 50 TP (DCF with 12% WACC and fully diluted share count) and reiterate Buy.

Pareto valuation graphs:

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.