A Note on Track Record

Over the past two years, I have published two investment ideas here that have generated returns exceeding 500% for readers who acted on them. I am sharing Anterix today because I believe this idea has similar potential — a structurally irreplaceable asset trading at a fraction of its demonstrable value at a moment when multiple powerful catalysts are converging.

Investment Summary

Anterix (NASDAQ: ATEX) is one of the most unusual asset stories in the US equity market: a company sitting on a nationwide, legally irreplaceable de facto monopoly on 900 MHz broadband spectrum — a dominant position built over a decade through FCC auctions and private market transactions that its own management now values at $2.5 billion to over $7 billion, yet which trades at a market capitalisation of approximately $758 million at the current share price of $40.

The thesis is straightforward. Anterix is the sole holder of nationwide broadband-capable 900 MHz spectrum in the United States. FCC rules make it legally impossible for any new entrant to replicate this position. Utilities are in the early innings of a once-in-a-generation grid modernisation cycle. On 18 February 2026, the FCC unanimously approved an expansion of the band that nearly doubled capacity.

On 26 February 2026, Qualcomm announced a deepened collaboration with Anterix, bringing industrial-grade 5G chipsets to the platform — a critical step toward availability of 900 MHz connectivity in mass-market mobile devices and a potential gateway to an Apple-like partnership.

On 14 April 2026, Amazon agreed to pay $11.57 billion to acquire Globalstar, demonstrating that the world’s largest technology companies pay extraordinary premiums for irreplaceable licensed spectrum.

Anterix has 12 signed utility customers covering 53 million people, over $400 million in contracted proceeds, and a $3 billion pipeline. A formal Morgan Stanley-led strategic review is ongoing. This article makes the case that investors today are being offered a rare opportunity to buy a scarce spectrum infrastructure asset at a fraction of its demonstrable market value.

Company History: From Pacific DataVision to Spectrum Landlord

Anterix traces its origins to 2014, when the company — then called Pacific DataVision (pdvWireless) — acquired a 6 MHz sliver of 900 MHz spectrum from Sprint for approximately $100 million. The great majority of Anterix’s 900 MHz spectrum had originally been purchased by Nextel through the FCC’s auction process. The founders, Brian McAuley and Morgan O’Brien, were the same team that built Nextel Communications — the company that pioneered push-to-talk Direct Connect and grew to a $36 billion valuation before merging with Sprint in 2005. These were not speculators; they were proven operators who understood how to commercialise licensed wireless infrastructure.

In 2020, the FCC adopted rules creating a 3×3 MHz broadband segment in the 900 MHz band. By 2021, the first licences had been granted, and Anterix had signed its first commercial deal with Ameren. The company rebranded as Anterix in August 2019. In 2024, Scott Lang became President and CEO. By April 2026, Anterix had 10 utility customers, covered 53 million people, and had $400 million in contracted spectrum proceeds.

The Spectrum: Why 900 MHz Is Uniquely Valuable

Not all spectrum is equal. 900 MHz has three exceptional qualities for utility use cases.

Physics. Low-band spectrum travels further and penetrates obstacles far more effectively than higher-frequency bands. A single 900 MHz base station can cover an area that would require four to six CBRS (3.5 GHz) base stations to serve. For utilities operating across thousands of square miles of rural territory, this translates directly into capital savings: fewer towers, less backhaul, lower total cost of ownership.

Technology ecosystem. The band has been standardised within 3GPP, meaning equipment from Ericsson, Nokia and Motorola Solutions is available off the shelf. On 26 February 2026, Anterix announced a deepened collaboration with Qualcomm — the world’s dominant mobile chipset company — to develop industrial-grade IoT chipsets optimised specifically for the 900 MHz platform. Qualcomm’s Snapdragon SDX35-3 and SDX32-3 modems will deliver 4G and 5G cellular connectivity on Anterix’s broadband platform. This partnership is significant beyond utilities: Qualcomm’s chipsets find their way into essentially all premium smartphones, including Apple iPhones. An Anterix-Qualcomm chipset ecosystem is the critical first step toward 900 MHz being available in mainstream consumer handsets, which would transform the addressable market from enterprise-only to consumer-facing. A deal with Apple, while speculative, is the logical next step in this trajectory.

The regulatory moat. The FCC’s rules require holding more than 50% of licensed 900 MHz spectrum in any county to qualify for a broadband licence. Anterix owns approximately 60% of all licensed spectrum in the 900 MHz band — a dominant position built through decades of FCC auctions and private market transactions. As of the 2020 FCC Report and Order, Anterix held licences for over 50% of the licensed channels in more than 3,100 of the 3,233 counties in the United States (excluding Pacific territories) — meaning it was eligible to apply for broadband licences in roughly 96% of US counties. The roughly 120 counties where it does not hold a 50%+ position tend to be very sparsely populated rural areas where the FCC has already licensed relatively little spectrum. A separate category of constraint involves legacy complex systems — operators with 45 or more functionally integrated sites, such as major utilities, railroads and large industrial companies. These operators are exempt from mandatory retuning entirely; before mandatory provisions can even be triggered, Anterix must first reach voluntary agreements covering at least 90% of licensed channels in the broadband segment — and even then, complex systems remain exempt and must be negotiated individually. As of the 2020 FCC Report and Order, Anterix had negotiations with 8 of the 10 largest complex systems operators. The complex systems operate low-data, narrowband systems – they need Anterix’s cooperation to get broadband.

Anterix spent years accumulating this spectrum position before the FCC froze new applications. No competitor can replicate it. The moat is structural, legal, and permanent.

The 18 February 2026 FCC Decision: Broader Than Utilities

On 18 February 2026, the FCC voted unanimously to expand the 900 MHz broadband allocation from 6 MHz to 10 MHz — nearly doubling available capacity in every county. This was the single most important regulatory event in Anterix’s history.

FCC Chairman Brendan Carr’s language at the February 18 meeting is worth reading carefully, because it reveals a vision well beyond utility grid management. Carr stated that expanding broadband capabilities in 900 MHz “promises new private wireless deployments across a range of sectors” and that the FCC is “advancing efforts to expand broadband use and create new opportunities for utilities and critical infrastructure providers” in ways that “strengthen the American economy.” Critically, the FCC’s formal order title — “Maximising the Potential of the 900 MHz Band” — signals spectrum policy aimed at broad economic productivity, not narrow utility management. In his January 27, 2026 blog post announcing the vote, Chairman Carr framed the initiative under “Good Governance” as a market-driven approach that “builds on our previous work to realign the band.”

The FCC’s framing of this as an economy-wide broadband initiative — not a niche utility tool — is significant for investors. It implies the regulator sees the 900 MHz band as infrastructure capable of serving broader sectors, including consumer applications in time. When the world’s leading mobile chipset company (Qualcomm) and the world’s leading satellite direct-to-device pioneer (Lynk, via experimental licence) are both integrating with Anterix’s spectrum, the “utility niche” characterisation begins to look too narrow.

Economically, CFO Elena Marquez stated at the April 9, 2026 investor call that the 10 MHz framework increases the company’s spectrum value to approximately $2.5 billion to over $7 billion — up from the $1.5–$4 billion range cited for 6 MHz just months earlier. NorthWestern Energy became the first utility to sign a 10 MHz contract within weeks of the ruling, immediately validating the expanded band in the market.

The Qualcomm Partnership: Opening the Door to Consumer Devices

On 26 February 2026, Anterix announced a deepened collaboration with Qualcomm Technologies, Inc. — a landmark development that has received insufficient investor attention. The partnership involves Qualcomm developing industrial-grade IoT chipsets (Snapdragon SDX35-3 and SDX32-3) specifically optimised for Anterix’s 900 MHz broadband platform, enabling 4G and 5G connectivity on utility private networks.

The strategic implications extend far beyond IoT. Qualcomm is the chipset architecture that powers the vast majority of premium Android smartphones and supplies modem technology that Apple uses in its iPhones. When Qualcomm builds 900 MHz support into its Snapdragon modem family, that capability percolates through the entire consumer device ecosystem. Anterix Chief Technology and Engineering Officer Carlos L’Abbate stated that the partnership gives utilities “a clear, scalable roadmap to 5G — one that delivers immediate operational value while supporting long-term network evolution.”

The implications are profound. If 900 MHz chipsets are embedded in standard consumer phones — the logical trajectory of this Qualcomm partnership — Anterix’s spectrum can support not just utility machines and sensors, but the billions of handsets already in people’s pockets. This transforms the potential customer base from a few hundred regulated utilities to hundreds of millions of individual device users. A commercial agreement with Apple — analogous to the Apple/Globalstar Emergency SOS arrangement that underpinned the Amazon/Globalstar deal — is the speculative but logical next step.

The Amazon/Globalstar Deal: Strategic Buyers Pay Up for Spectrum

On 14 April 2026 — just days before this article was written — Amazon announced it would acquire Globalstar (GSAT) for $11.57 billion in cash and stock at $90 per share, representing a 117% premium over Globalstar’s price from late October 2025. The deal is primarily driven by Globalstar’s globally harmonised spectrum portfolio — L/S-band, Band 53/n53, and C-band optionality — which Amazon will combine with its Amazon Leo satellite broadband system to enable direct-to-device services.

The strategic lesson for Anterix investors is direct: the world’s largest technology companies pay very substantial premiums for irreplaceable licensed spectrum, and they do so when they see the spectrum as a platform for future consumer-facing services. Amazon paid $11.57 billion for spectrum that directly competes with SpaceX’s Starlink, which is itself already building out its spectrum position through the EchoStar acquisitions. Spectrum scarcity at the consumer connectivity layer is now driving some of the largest technology deals in history.

Globalstar’s Q1 2026 revenue was $71.96 million annualised — far lower than Anterix’s $400M+ in contracted proceeds already in hand. Yet Globalstar commanded $11.57 billion. The valuation differential is driven by spectrum type, strategic optionality, and the identity of the buyer. Anterix’s 900 MHz position — nationwide, terrestrial, an irreplaceable spectrum franchise now expandable to 10 MHz — represents a comparable class of strategic scarcity.

Notably, SpaceX had previously explored acquiring Globalstar before Amazon outbid it. That competitive dynamic confirms that multiple of the world’s most powerful companies are actively competing for licensed spectrum platforms. Anterix’s ongoing strategic review with Morgan Stanley is taking place in exactly this environment.

The Lynk Partnership: Opening the Satellite-to-Consumer Frontier

At the April 9, 2026 investor call, Anterix announced a partnership with Lynk Global — a direct-to-device satellite company — to file for an FCC experimental licence to test integration of Lynk’s satellite direct-to-device capabilities with Anterix’s 900 MHz private wireless. The testing covers handsets, computers, edge devices and routers across multiple geographic locations and begins in seven US markets from May 2026.

This is potentially the most transformational development in Anterix’s history, and it is the one most likely to be mispriced by the market. Lynk is a pioneer in satellite direct-to-device connectivity — already the second D2D provider licensed for commercial service in the US after SpaceX, with FCC approval to operate in Guam and the Northern Mariana Islands. Lynk’s technology allows standard unmodified smartphones to communicate directly with satellites using existing cellular spectrum. In other words, Lynk can turn Anterix’s 900 MHz licences into a platform for delivering satellite connectivity to every mobile phone user in America.

Chief Regulatory Officer Chris Guttman-McCabe said the expanded 900 MHz band creates “broader strategic optionality” for “industrial IoT networks, transportation and logistics hubs, water and wastewater systems, and satellite providers.” Asked whether the satellite work could become a standalone product, he said simply: “stay tuned.” CEO Scott Lang said the company is “leaning in early” to position customers “to take advantage of what’s next.”

The parallel to the Grain Management situation is instructive. Grain Management acquired 800 MHz spectrum from T-Mobile for approximately $2.9 billion, initially targeting utilities — but is now pivoting to satellite D2D operators as well, recognising that low-band spectrum is the strategic infrastructure layer for the next generation of connectivity. Anterix’s 900 MHz is one step higher in frequency than Grain’s 800 MHz, with superior propagation characteristics for both terrestrial and satellite-assisted applications. If Anterix secures FCC approval to enable satellite D2D on its 900 MHz licences, the addressable market shifts from 60 utilities to 300 million American mobile users.

The Customers: America’s Largest Regulated Utilities

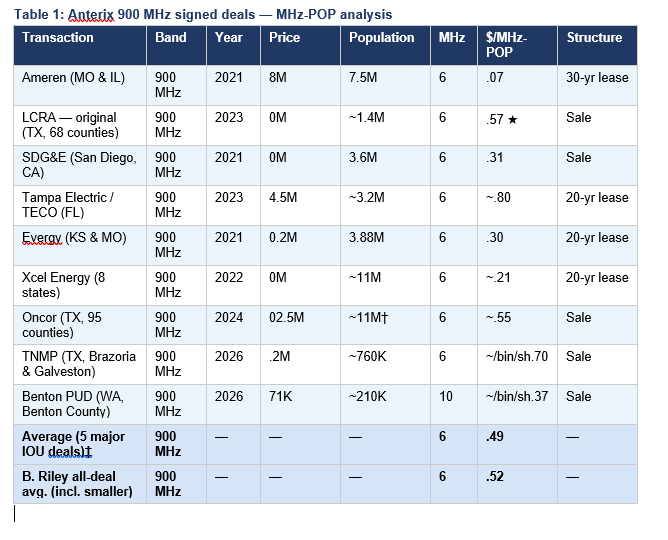

Anterix’s 12 signed customers as of April 2026 are all investment-grade, regulated US utilities whose spectrum purchases are effectively cost-recoverable through state utility commission rate bases:

- Ameren (MO & IL) — December 2020; $48M; 7.5M people; 30-yr lease

- San Diego Gas & Electric (CA) — February 2021; $50M; 3.6M people; $2.31/MHz-POP

- Evergy (KS & MO) — September 2021; $30.2M; 3.88M people; “fair market value”

- Xcel Energy (8 states) — October 2022; $80M; ~11M people; 20-yr lease

- Oncor Electric Delivery (TX, 95 counties) — June 2024; $102.5M; 13M people

- LCRA (TX) — original 2023, expanded January 2025; $13.5M add-on

- CPS Energy (San Antonio, TX) — January 2026; $13M; nation’s largest community-owned utility

- Texas-New Mexico Power (TNMP) — March 2026; subsidiary of TXNM Energy

- NorthWestern Energy (MT, SD, WY) — March 2026; $7.7M; first 10 MHz deployment

- One additional undisclosed customer

Together these customers collectively serve tens of millions of people across multiple states — and the addition of Benton PUD, a publicly owned utility (PUD), marks the first time Anterix has signed a non-investor-owned utility, opening an entirely new category of potential customers.

Current Monetisation and Financial Position

Anterix generates revenue through two models: long-term spectrum leases, where Anterix retains the licence, and the utility pays for the right to use it, and outright spectrum sales, where the licence transfers permanently to the utility. Both structures generate large upfront cash payments. Understanding why utilities increasingly prefer outright purchases over leases is essential to grasping the commercial dynamics of this business, and reveals a structural incentive that is highly favourable to Anterix.

Utilities in the United States are regulated entities whose financial returns are governed by state public utility commissions. The fundamental principle of utility regulation is straightforward: a utility earns a regulated rate of return on the capital it invests in infrastructure — its rate base. When a utility buys an asset outright, that asset enters the rate base and generates a perpetual, commission-approved return on investment. When a utility leases an asset instead, the lease payments are treated as an operating expense and do not contribute to the rate base at all. This distinction is financially material. A utility that purchases 900 MHz spectrum licences is making a capital investment that earns regulated returns for decades. The spectrum becomes a productive infrastructure asset on the utility’s balance sheet — earning the same regulated return as a substation or a transmission line — with ratepayers bearing the cost and the commission approving the expenditure as prudent infrastructure investment. This is precisely why utilities such as SDG&E, Oncor, LCRA and CPS Energy have chosen outright purchase over leasing: not simply because they prefer ownership, but because ownership is economically superior under the regulatory model they operate within. For Anterix, this dynamic is highly favourable. As utilities increasingly internalise the rate-base benefit of owning spectrum, outright sales — which represent the most complete and immediate monetisation of Anterix’s licences — are likely to become the preferred structure. It also means that the 60+ potential customers in the pipeline have a structural financial incentive built into their regulatory frameworks to buy rather than rent, creating durable and growing demand.

Key financial metrics as of April 2026:

- Over $400M in contracted proceeds from 12 signed deals

- ~$123M in contracted proceeds outstanding as of Q3 FY2026

- $80M+ expected in Q4 FY2026

- Zero debt on the balance sheet

- Cash and restricted cash ~$38M (December 2025)

- 18.96M shares outstanding; market cap ~$758M at $40/share

- Spectrum assets carried on balance sheet at $325M — far below monetisation potential

Adjacent revenue streams include TowerX (with Crown Castle, 40,000+ tower sites) and CatalyX (SIM/eSIM management), with a combined addressable market that management estimates at approximately $1 billion annually. The AnterixAccelerator programme has $250M in active negotiations and is described as “oversubscribed.”

How Shareholders Can Realise Value

Path 1 — Organic pipeline conversion. The $3 billion pipeline across 60+ potential customers is the standalone story. Converting even 30–40% at historical deal prices would generate $900M–$1.2B in additional contracted proceeds — meaningfully in excess of the current market cap. Management confirmed at the April 2026 investor call that it will discontinue the “Demonstrated Intent” disclosure in Q4 FY2026, signalling that the pipeline is maturing beyond the need for such granular tracking.

Path 2 — Strategic transaction. The Morgan Stanley-led strategic review remains active. The Amazon/Globalstar precedent (117% premium, $11.57B) powerfully illustrates what strategic acquirers pay for irreplaceable licensed spectrum. B. Riley analysts estimate a plausible acquisition price of approximately $75/share — an 88% premium to the current price. Potential acquirers include infrastructure funds (Brookfield, DigitalBridge, Stonepeak), Crown Castle, Ericsson, Nokia, Qualcomm, and utility consortia — each with compelling strategic motivation.

Path 3 — Consumer and satellite market expansion. The Qualcomm chipset partnership and the Lynk satellite D2D experimental licence open a third path: transformation from a utility-only spectrum licensor into a platform for mass-market consumer and satellite connectivity. If even a fraction of this optionality is realised, the addressable market resets from $3 billion to many multiples of that figure.

Who Could Acquire Anterix?

The Morgan Stanley strategic review has been running since February 2025 with confirmed ongoing inbound interest. The Amazon/Globalstar deal — $11.57 billion at a 117% premium, announced just days ago — is the most powerful recent proof point that strategic buyers pay extraordinary prices for irreplaceable licensed spectrum. Several categories of acquirer have both the motivation and the financial capacity to acquire Anterix at a meaningful premium to current market prices.

Infrastructure and digital infrastructure funds. Firms such as Brookfield Infrastructure, DigitalBridge, Stonepeak and KKR Infrastructure are the most natural fit. Anterix matches their template precisely: a dominant licensed asset with a structural moat, generating long-dated contracted cash flows from investment-grade regulated utility customers, zero debt, and an expanding addressable market. A take-private at $0.80–$1.20/MHz-POP would be highly value-accretive for a fund with patient capital and the operational resources to accelerate pipeline conversion.

Crown Castle. The tower company already operates the TowerX partnership with Anterix, giving it direct commercial insight into the business and its utility customer relationships. Acquiring Anterix would transform Crown Castle from a passive tower lessor into a vertically integrated private wireless infrastructure provider — owning both the tower layer and the spectrum layer in every utility deployment. This vertical integration would enable Crown Castle to capture a significantly larger share of the value chain per deal.

Telecom equipment vendors. Ericsson and Nokia are both deeply embedded in the Anterix ecosystem and supply radio equipment for 900 MHz deployments. Either could acquire Anterix to vertically integrate the spectrum layer, gaining a decisive competitive advantage in winning utility network build-out contracts. A utility procuring a 900 MHz private LTE network from Ericsson-plus-Anterix would deal with a single vendor controlling spectrum, equipment and deployment. Qualcomm, which deepened its chipset partnership in February 2026, is a more speculative but not implausible candidate given its strategic interest in expanding 900 MHz into consumer devices.

Large utility consortia. A consortium of major US utilities — perhaps led by NextEra Energy, Duke Energy or Dominion — could acquire Anterix to permanently lock in spectrum access and prevent competitors from securing it. As grid modernisation accelerates and 900 MHz becomes the de facto standard for utility private wireless, the long-term cost of not owning the underlying spectrum layer could become material. A consortium acquisition would also allow participating utilities to reduce per-unit spectrum costs and share clearing and licensing infrastructure.

Hyperscalers and large technology companies. The Amazon/Globalstar deal confirms that the world’s largest technology companies are willing to pay over $11 billion for irreplaceable licensed spectrum assets. Microsoft, Google and Amazon all have industrial IoT and grid infrastructure ambitions. Owning the licensed spectrum layer for US utility infrastructure — now expandable to 10 MHz and increasingly relevant to consumer devices through the Qualcomm partnership — would represent an extraordinary strategic asset for any hyperscaler seeking to build an industrial connectivity platform.

B. Riley analysts have estimated that a strategic buyer would likely pay above the market-implied level but below the average of Anterix’s own signed deals, suggesting a plausible acquisition range of approximately $0.77–$0.87/MHz-POP — implying a share price of approximately $75, or roughly 88% above today’s $40. Any acquirer with the ability to accelerate pipeline conversion would rationally pay more than the public market implies, given that the underlying asset value is validated by ten arm’s-length utility transactions at materially higher per-MHz-POP prices.

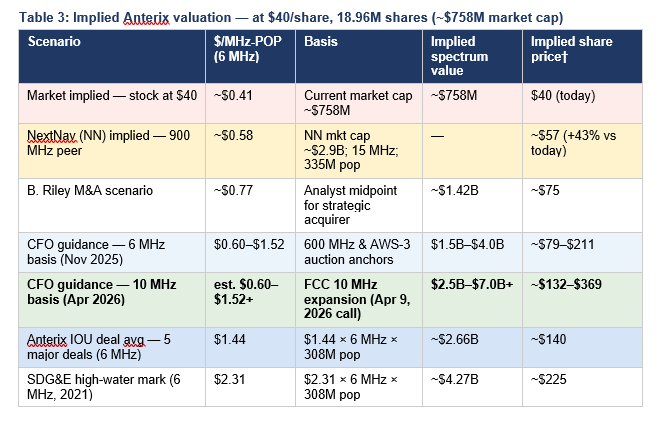

Valuation: Three Tables Tell the Story

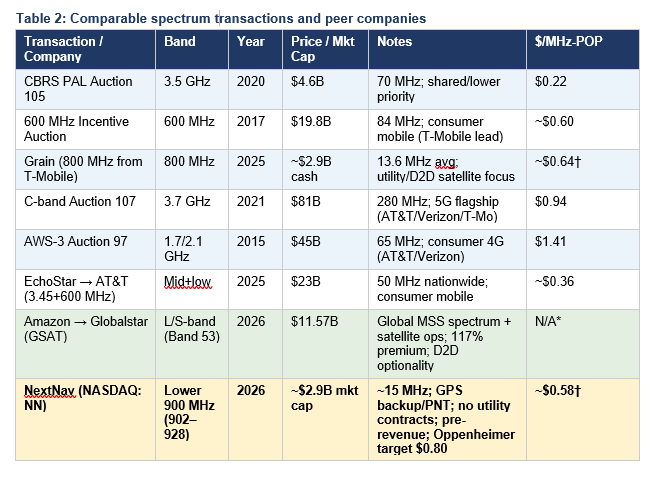

We present three analytical tables. Table 1 shows Anterix’s own signed deals — the most directly comparable transactions. Table 2 provides broader market context, including FCC auctions, the Amazon/Globalstar deal, Grain Management’s 800 MHz acquisition, and the crucial NextNav (NN) peer comparison. Table 3 shows implied company valuation and per-share price across scenarios, all calculated at the current price of $40 and 18.96 million shares outstanding.

Source: Anterix SEC Form 8-K filings; Light Reading; Evercore analyst note; B. Riley Securities research (March 2025); company confirmation (April 2026). MHz-POP calculations: author’s own. ★ = LCRA original (April 2023) is the highest $/MHz-POP deal on record at ~.57. † Oncor: company territory population is 13M but 95-county coverage population estimated at ~11M; author uses ~11M for MHz-POP. ‡ Average calculated on Ameren, SDG&E, Evergy, Xcel, and Oncor (the five largest investor-owned utility deals at 6 MHz). Benton PUD (10 MHz, rural county) and TNMP/LCRA (smaller or partial coverage) excluded from average as not directly comparable for pricing benchmarks.

Source: FCC public auction records (Auctions 97, 105, 107); EchoStar SEC Form 8-K (August 2025); Amazon press release (April 14, 2026); Bloomberg; Grain Management press release (March 20, 2025); Broadband Breakfast (April 1, 2026); TradingView/Oppenheimer (April 2026); IEEE ComSoc Technology Blog. † Author’s own MHz-POP calculations. * Amazon/Globalstar not directly comparable due to global MSS licence structure; shown for strategic context only. NextNav (NN): market cap ~$2.9B as of April 2026; estimated 15 MHz contiguous lower 900 MHz spectrum (902–928 MHz); different band and use case from Anterix (PNT/GPS backup vs. broadband); no utility contracts; pre-revenue; shown as 900 MHz band valuation reference only.

The NextNav (NASDAQ: NN) comparison deserves particular attention. NextNav holds approximately 15 MHz of lower 900 MHz band spectrum (902–928 MHz) and trades at a market capitalisation of approximately $2.9 billion — implying roughly $0.58/MHz-POP. This is 40% above Anterix’s current implied $/MHz-POP of $0.41. Yet NextNav has no utility contracts, generates essentially no revenue from its spectrum, and its business case depends on a speculative FCC rulemaking for GPS backup services that has yet to be approved. Anterix, by contrast, has $400M+ in contracted proceeds, 10 signed utility customers, and a proven commercial market. If Anterix were to trade at NextNav’s implied $/MHz-POP, the share price would be approximately $57 — already 43% above today’s level. Oppenheimer’s $0.80/MHz-POP target for NextNav, applied to Anterix’s 6 MHz position, implies an Anterix share price of approximately $120.

Source: † Per-share figures are author’s own calculations: ($/MHz-POP × 6 MHz × 308M US population covered) / 18.96M shares. CFO valuation ranges from Q2 FY2026 earnings call (November 13, 2025) and April 9, 2026 investor call. B. Riley $75/share from March 2025 research note. NextNav comparison: author’s own calculation applying NN’s implied $/MHz-POP to ATEX’s 6 MHz position. Deal average updated to $1.49 following company corrections (April 2026). Figures exclude cash (~$38M), TowerX/CatalyX revenue, and pipeline option value — spectrum value only; a floor estimate, not a ceiling. Not financial advice.

The most striking observation from Table 3: at $40/share, the market implies Anterix’s spectrum is worth $0.41/MHz-POP — well below NextNav’s implied multiple despite NextNav having no contracts, less than one-third of what every major Anterix utility customer has paid in arm’s-length transactions, and less than one-ninth of the LCRA deal, which stands as the highest $/MHz-POP transaction on record at $3.57. Management’s own $7 billion upper bound (10 MHz basis) implies a share price of $369. Even B. Riley’s conservative M&A scenario ($75/share) represents 88% upside from today.

Key Risks

- Execution and pace: The $3B pipeline is not contracted. Utilities have been slow historical decision-makers, and conversion timelines are difficult to predict.

- FCC licence delivery: Licences are granted county by county as incumbents are cleared. Anterix estimated in its 2020 shareholder letter that total clearing and licensing costs would range from $130–$160 million nationally. Complex-system counties — where operators with 45 or more integrated sites are exempt from mandatory retuning — require voluntary negotiation, which can be protracted and is not guaranteed to succeed on commercially acceptable terms.

- Strategic review uncertainty: The Morgan Stanley process has run 14+ months with no announced deal. There is no guarantee it results in a transaction.

- Cash runway: With ~$38M in cash and no debt, Anterix is dependent on contracted proceeds arriving on schedule. Operational discipline remains critical.

- Liquidity and volatility: With ~18.96M shares outstanding and 90%+ institutional ownership, ATEX is thinly traded and susceptible to outsized price moves on news events.

- Grain competition: Grain Management’s 800 MHz portfolio (acquired from T-Mobile for ~$2.9B) targets a similar utility customer base. While the bands differ in propagation characteristics and ecosystem maturity, Grain represents a credible competitive alternative for utilities evaluating private wireless options.

- Satellite and consumer optionality remains speculative: The Lynk partnership and the Qualcomm consumer device roadmap are not contracted revenue. FCC approval for satellite D2D operations on 900 MHz is not guaranteed.

Summary: A De Facto Monopoly at a Rare Discount, With Multiple Expanding Catalysts

Anterix is not a conventional investment. Its value resides in its spectrum asset — a finite, legally protected nationwide spectrum franchise representing a de facto monopoly position that took a decade to build and cannot be replicated. The opportunity exists because most investors do not follow small-cap spectrum companies. A company whose own management describes its spectrum as worth $2.5 billion to over $7 billion trades at a market capitalisation of approximately $758 million.

When we last published ideas generating 500%+ returns, the common thread was a structurally mispriced asset with multiple catalysts converging. Anterix today presents more converging catalysts than any other opportunity we have seen:

- The February 2026 FCC ruling doubled capacity and permanently expanded the addressable market.

- The Qualcomm partnership (February 2026) brings 900 MHz into the consumer device chipset roadmap and signals a credible path to an Apple-like deal.

- The Lynk Global experimental licence opens the satellite-to-consumer frontier on Anterix’s spectrum.

- Amazon paid $11.57B for Globalstar (April 2026) at a 117% premium — confirming that the world’s largest technology companies pay extraordinary prices for irreplaceable licensed spectrum.

- NextNav (NN) trades at ~$0.58/MHz-POP ($2.9B market cap) with no utility contracts, versus Anterix’s $0.41/MHz-POP with $400M+ contracted. The closest 900 MHz band peer is valued 40% higher despite having nothing comparable to show for it.

- Grain Management paid ~$2.9B for 800 MHz utility-focused spectrum — a comparable low-band transaction at $0.64/MHz-POP versus Anterix’s implied $0.41.

- The Morgan Stanley strategic review remains active, with management confirming ongoing inbound interest.

- Management’s own spectrum valuation ($2.5B–$7B+) is 3–9x the current market cap of $758M.

For an investor with a 2–4 year horizon and tolerance for execution risk, ATEX offers an irreplaceable spectrum franchise with a structural moat, a live M&A process, a validated and growing customer base, three expanding market opportunities (utility, industrial/satellite, consumer), and a valuation that implies the market believes the spectrum is worth less than any comparable public auction or private transaction has ever suggested.

In a market where most “value” investments are commodities dressed as moats, Anterix has a real one: written into FCC regulations, validated by ten of America’s largest regulated utilities, deepened by Qualcomm’s chipset partnership, and now positioned at the frontier of the satellite direct-to-device revolution.

Important Disclaimer

This article is produced for informational and educational purposes only and does not constitute financial or investment advice. Spectrum valuations are inherently uncertain. Management estimates are forward-looking statements subject to material risks and uncertainties. Past deal prices are not guarantees of future transaction values. All numerical calculations are the author’s own unless otherwise noted. Readers should conduct their own due diligence and consult a qualified financial adviser before making investment decisions.