Biovica announced a few weeks ago, that FDA requested one additional information needed for Biovica FDA approval. Analysts believe it is the final bit in the puzzle and that FDA approval is comming within a few weeks. Biovica could easily double by the FDA approval.

Pareto’s take on today’s announcement

DiviTum’s 510(k) resubmitted to the FDA

Expected for later May, Biovica surprised yesterday evening with the 510(k) application for DiviTumhaving been resubmitted to the FDA. In a call with the CEO the same evening, he clarified that the FDA wanted to look at the data before it is being resubmitted and thereafter was fine with the submission. Subject to no further delays by the FDA, we expect approval before end of June. Thereafter, DiviTum will be made available to physicians and patients being treated in metastatic breast cancer setting, finding out earlier (after 2 weeks) if the given drug (CDK 4/6 inhibitor) is working or not (instead of >3 months). A crisp new readout at the disposal of physicians that we believe will change treatment monitoring practices over time. The company will update on its commercialization strategy at its capital markets day on May 17. We reiterate our Buy rating on BIOVIC with a target price of SEK 103/share.

EU will reduce Russian gas consumption. Done deal. Only question how quickly this will happen. Russian stop of gas for Poland and Bulgaria may indicate that this may be quick. How to trade this? I am sure there are many trades. The first that comes to mind are LNG shipping and coal. I wrote here several times about LNB shipping idea – see the older posts. I focus today on Polish coal.

Polish Coal

Coal stocks are very cheap. Especially Polish coal stocks.

Coal prices have doubled last year and doubled again in 2022. The EU ban on Russian coal that comes into effect in Q3 is pushing coal prices further. Russia exports USD5 billion of coal to EU. And finally the threat of Russian gas supplies also helps and will help coal prices. We see very interesting coal prices prospects.

We are long Polish coal mine JSW. The JSW Group is the largest producer of high quality hard coking coal in the European Union and one of the leading producers of coke used for smelting steel. SEE:

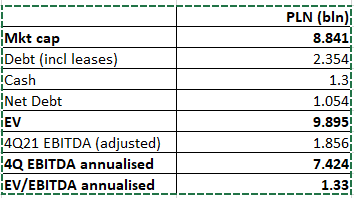

JSW will generate EBITDA equal to its market capitalization in 2022

I spoke to IR last week. Below is a summary of what they said and my valuation assessment of this:

In 2021 JSW sold 13.8 mil tons of coal. They expect 14.5 mil tons for 22

They had a very strong 2021Q4 – if you annualize Q4 numbers into a fully year – JSW is trading at just 1.2 EV/EBITDA. Very cheap for the largest EU coking coal producer. I enclose the valuation table below.

Last week the company has announced its Q1 trading report (see the website). 1Q22 was the best quarter for many years:

coal volumes sold up 6% qoq

average selling price in USD up 24% qoq

PLN down by 2% qoq

implied revenue growth in PLN 34% qoq

The increase in realized coal prices should flow through the Profit and Loss and increase EBITDA, and profits.

The coal price effect should increase EBITDA in PLN by 27%.

I assume a quarterly reduction of EBITDA due to energy costs inflation by 7%. The number is arbitrary. You can plug your own number into the below model to see the impacts.

Under the above assumptions 1Q22 EBITDA should increase by around 20% vs 4Q21.

I annualized the estimate 1Q22 EBITDA to get an 22 annual EBITDA. At the current share price JSW trades at EV/EBITDA22 of 1.0. Very cheap.

Q2 and Q3 should be even better.

The reason is how pricing is done. They fix prices on a quarterly basis. For example, if you want to model the average price for 22Q2, you take an average of 5 months before the Q2 (Nov21-March22) and discount it by 10%.

So today’s high prices will affect their Q3 and Q4 figures. You have a good pricing visibility.

Back of the envelope valuation table

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

After the Amazon Partnership announcement Linkfire management organised calls with major investors. We spoke to the company, the Pareto Securities analyst, and other shareholders. Below is my take on the conversations:

Linkfire Investment Opportunity Summary:

Linkfire connects consumers on social platforms who wanted to download a song to music streaming companies that provide the content. Linkfire collects revenues from both.

Linkfire has 70% market share in its segment. The penetration is still very low.

Linkfire revenues have grown at 40%-60% CAGR with a stable 76% gross margin. The growth is accelerating further in 2022 to 50-70%.

Linkfire managed to dominate music industry. They will now enter with the same product podcasts, movies and games. These new areas will multiply the revenue opportunity.

Very strong catalysts in the next six months.

Amazon Partnership is a transformative deal for Linkfire.It is important for two reasons:

It is further increasing the revenue acceleration

It is increasing Linkfire’s leverage towards its partners – the other streaming companies and the record labels and artists

The company had a standard affiliate deal with Amazon before and it was not a global agreement. It is also fair to assume that the pricing was significantly lower than the current deal.

Linkfire makes the highest returns in developed markets where the rates are highest. Amazon is strongest in the developed markets. Therefore, the deal should help Linkfire to increase fees in the most profitable segment.

The top three streaming companies have around 60% subscriber market share (Spotify 31%, Apple Music 15%, Amazon Music 13%). Linkfire now has two of them as a client (Amazon and Apple).

Amazon´s importance is increasing; it increased its market share from 13% to 15% just in 1Q22.

Amazon and Apple partnerships must be a powerful selling point with the streaming clients. After the deal, the largest streaming companies must have been in contact with Linkfire. They all must be worried that Linkfire is now incentivized to work closely with Amazon and Apple, which would increase the market share of the two at the expense of others. The Amazon deal should therefore enable Linkfire to accelerate the completion of similar deals with other major streaming companies.

The Amazon transaction is also a big selling point for Linkfire subscription clients – the artists and the record labels. It is a rubber stamp on Linkfire capabilities by the best in the industry. Linkfire should be able to accelerate its content client numbers as well as the pricing power is increasing by such deals.

Pareto analyst estimates that Amazon transactions alone should be able to double commission-based revenues already in 2022 (see my yesterday post with details). If other deals come along, the revenue acceleration would increase further.

Linkfire is working to replicate its business model to other areas. The next ones in line are podcasts and audiobooks. These industry segments are fragmented; there are many content providers. The Amazon deal may indicate that Linkfire would most likely enter the area in partnership with a major player in Audiobooks and Podcasts. With a strong partner on board, the capture of the smaller partners would be much faster. Amazon deal should help in getting a strong partner in Audiobooks and Podcasts on board.

We are very bullish on Linkfire. The Q1 report is due on 25 May 2022.

Link to the 2022 annual report presentation– very good document:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Linkfire, announced partnership with Amazon Music, that in Pareto view has the potential to double commission-based revenue in 2022. It is a major news. Linkfire is the global market leader in smart links for music streaming companies with a 70% market share.

Five bullet point summary on Linkfire opportunity:

Linkfire connects consumers on social platforms who wanted to download a song to music streaming companies that provide the content. Linkfire collects revenues from both.

Linkfire has 70% market share in its segment. The penetration is still very low.

Linkfire revenues have grown at 40%-60% CAGR with a stable 76% gross margin. The growth is accelerating further in 2022 to 50-70%.

Linkfire managed to dominate music industry. They will now enter with the same product podcasts, movies and games. These new areas will multiply the revenue opportunity.

Very strong catalysts in the next six months.

Pareto summary of the Amazon Partnership:

Amazon Music becomes an affiliate partner to Linkfire

Linkfire enters a multi-year marketing and affiliate agreement with Amazon Music. This agreement will further fortify Linkfire´s position as the leader in its market niche, and will help Linkfire greatly strengthen the monetization of its traffic. We believe the agreement will have a significant positive impact on commission-based revenues, and will help Linkfire reach its mid-term financial target of 50-70% annual organic revenue growth over the FY2021-FY2023 period.

Linkfire announced on Friday evening (22/4/2022) that the company has just signed a multi-year marketing and affiliate agreement with Amazon Music. The agreement will entail a custom strategy for user acquisition tailored for Amazon Music and will leverage the vast traffic flows of Linkfire. The agreement will monetize Linkfire’s traffic when a consumer clicks through a Linkfire smart link and then signs up at Amazon Music or makes a transaction within Amazon’s ecosystem.

We had suspected that Linkfire were coming close to signing a new affiliate partner, and expect this new deal to give a significant revenue boost to the company. Amazon Music has an estimated market share of around 13% of the global music streaming market, and given that Linkfire, according to our estimates, currently monetizes ~15% of its total traffic, this new affiliate deal can potentially almost double the company’s monetization rate on its traffic. All things equal, assuming the same amount of consumer connections as well as RPM as in 2021, this deal could result in the commission-based revenue close to doubling in 2022. Given this, our confidence that Linkfire can reach its mid-term target of growing revenue organically at an annual rate of between 50-70% over the 2021-2023 period has increased.

See the previous blog posts on Linkfire for more details

Link to the 2022 annual report presentation– very good document

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

This is the third installment of “How to trade the Russian war”

We have been bullish on Product tankers since the war started. The idea is that EU will seek to limit its supplies from Russia. Russia is the main supplier of diesel for the EU. As the dependance on Russia is decreasing, EU will have to ship Diesel from longer distances and Russia will ship its Diesel also much further. Product tankers should benefit. And they already are. The current daily rates imply sub 4x P/E and +20% ROE for Hafnia.

Pareto just revised its price targets and see 35-40% upside from current levels. If the EU embargo on Russian diesel is enacted, product tankers should see much higher upsides.

We are long Scorpio and plan to buy Hafnia on weakness.

Pareto Research Summary

Product Tankers: True inflation for the first time in 15 years

Driven by both higher input costs and booming order intake for container vessels and gas carriers – newbuild prices are (almost) back at 2008-peaks. This is pushing return requirements upwards – at a point in time where we should be starting to replace the ageing vessels that do not fit well in an EEXI/CII world from 2023. The stage is set for 2023 – and with the tragic invasion of Ukraine we see an additional demand increase of 5 – 10% for product tankers. We raise our estimates and see 35 – 40% upside for Hafnia and Scorpio Tankers. BUY ahead of Q1 reports next month.

Ship value inflation for the first time since 2007 For the first time in 15 years, we have seen a consistent increase in newbuild prices. Shipyard orderbooks are filled up with container and gas carriers, while rising input costs and reduced yard capacity also push prices higher. As a consequence, MRs are now quoted above USD 40m for the first time since 2009 – and some 15% above the last 10Y average. This is pushing return requirements upwards, with the 10%-return rate now closing in on USD 19,000/day – a level which would imply sub 4x P/E and +20% ROE for incumbent Hafnia.

…and spot rates are surging – ahead of schedule Meanwhile, product tanker spot rates have had an encouraging start to 2022. LRs saw early Q1 tightness, with several regions experiencing strong demand and vessel shortness. MRs have since stolen the show, and again it is encouraging to see strong demand and vessel tightness in both the Atlantic and Pacific at the same time. Seaborne transportation demand should be back to pre-COVID levels imminently, and with a ~5% orderbook and rapidly ageing fleet scrapping activity will remain high – and net fleet growth low.

Altered Russian product exports could mean 200x new MRs The tragic invasion of Ukraine is putting ~1.2mbd of Russian product exports to NW Europe under pressure. A likely new destination is South America, and in turn this will push more US volumes to Europe. This would mean a big boost to tonne-miles, with 1.2mbd ~4% of total volumes – and the new distance about five times as great. While still early it could require as many as 200x incremental MR tankers – or roughly 10% of the total MR/Handy fleet (6% of total product tankers). This is most likely one reason for the MR strength we now see, and we have raised our 2022 estimates 5 – 15%, seeing double digit demand growth this year.

HAFNI: Just getting started – TP up to NOK 36 (29) With the rare combination of decent leverage and low cash break-evens Hafnia is now in a very comfortable situation. We could see dividends return after Q1, with Q2 guidance set to be solid. Current NAV of NOK 29 will become 36 by YE’22, and we see no reason for any discount here. TP up to NOK 36 (29), and we reiterate our BUY / top tanker pick rating.

STNG: Now leverage is working with them – TP up to USD 30 (22) We raise our TP to USD 30 (22) ahead of the Q1 release early next month. Scorpio’s heavy debt burden should now be working in their favor, and we expect firm Q2 guidance from the eco-fleet with (mostly) scrubbers to give an initial taste of the potential. Reiterate BUY.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Very interesting article from FT today. Extracts below.

Hedge fund trader who won big on GameStop backs energy stocks

Hedge fund trader who won big on GameStop backs energy stocks Senvest Management snaps up shares in unloved oil and gas companies.

Senvest made on GameStop 2,400% profiting $700mn.

Oil and gas stocks are on track for further strong gains, as a sector shunned by ethically minded investors regains favour.

New York-based Senvest Management, 86 per cent gains in 2021 ranked him among the best-performing hedge funds in the world, said he now has a quarter of his portfolio in fossil fuel stocks.

“The result of the ESG movement is that there’s been massive multiple compression [in oil and gas stocks] and we still haven’t come back from that,” said Mashaal, adding that many oil and gas companies had felt that investment capital “wouldn’t be there for them”.

“Now there are other countervailing interests, such as the security of energy supply, that have come to the fore and which are not going to go [away] anytime soon,” he said.

He believes a surge of funding will be needed in the traditional energy sector to correct years of under-investment.

“You’ve got a couple of years before a meaningful production response can be mounted to satisfy demand. There’s a very solid outlook [for oil and gas stocks] for another year or two,” he said.

“There’s a lot of room for multiple expansion [in these stocks],” said Mashaal, adding that a high oil price had not been fully factored into these companies’ share prices.

“People realise this is not going away in the short or medium term. It’s not like ESG goes away, but we [now] need to balance it with energy security and where you want to buy your oil from,” he said.

We spoke to one of our brokers in Norway. We were told Senvest is active in Norwegian energy stocks. Many of the stocks trade at 30-40% CF yield. Plenty of upside in our view.

We are long Aker BP, Var Energi, Africa Oil, Africa Energy and Noble in the energy sector.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Pryme, Quantafuel plastic recycling peer got very positive report by Nordea analyst Elliott Jones. The share price is beaten down since the IPO. Lately market was concerned about the capital raise in the current markets. The capital raise happened, which is a major short term catalyst. The share price saw +30% based on Elliott Jones report. As the major risk is resolved we are bullish. This could be a Pryme ride this year.

If you look at Quantafuel graph, the share price performed very well up to starting the production. Nordea indicates this could happen with Pryme too.

Quatnafuel – we speak to large investors that spoke to the company recently. All the feedback are very positive. Hope for a company update soon.

We are scheduled to talk to Arctic analyst on Quantafuel this week. Stay tuned for a report.

Extracts from Nordea Research:

First facility is fully capitalised

What has happened? Capital raise finally complete

In the company’s Q4 report in February, Pryme announced that it aimed to raise EUR ~15m to ensure completion of its first facility in Rotterdam

On 8 April (last Friday) the raise was finally complete, with Pryme raising NOK 154m via a private placement

In line with previous comments, the proceeds will fund remaining capex for its first facility, opex until mid-2023, the acquisition of an industrial plot in the Port of Amsterdam and working capital movements

Changes to estimates

We include the capital raise terms and expected upcoming repair issue in our model, which results in Pryme’s first facility being fully capitalised (production expected Q4 of this year)

The proceeds from the raise result in a slightly smaller future capital requirement than previously expected, with the company’s second facility due in H1 2023 (we build in the raise just prior to construction beginning)

We hold all other estimates unchanged

Valuation

Our valuation methodology unchanged, which involves deriving cashflows for each future facility and discounting back to today (WACC, propability weightings etc all constant)

However, by updating our estimates for the above and updating for FX, we arrive at a new target price of NOK 85 (100), primarily due to the dilutive aspect of the capital raise

What do we think?

Despite the above, we see clear advantages from the completion of the placement:

The share price is down by over 35% since the February announcement, pointing to the possibility of a recovery once the dust settles

Given a new CEO will start in May and the first oil is expected in six months (key triggers), we foresee no negative changes to business fundamentals

Even post the raise, Pryme remains clearly the cheapest option on the market for chemical recyclers today (including 8x lower than QFUEL)

Thus we reiterate Buy, with Pryme representing by far the cheapest option by market cap in the chemical recycling space

Key triggers?

With the raise being our previous immediate trigger, focus for investors should move to development of facility one ahead of production in Q4

Key information on this could also be included in the company’s Q1 report on 25 May

We are long Pyme – our family office invested in the capital raise last week.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Brussels has said a block on Russian coal exports will be part of an upcoming fifth sanctions package that is currently being discussed by EU member states.

Further the coal price in Q4 did not reflected the Russia coal ban.

The stock is very cheap today. If the Russian coal happen this stock could easily triple. It would still trade below 4 EV/EBITDA on Q4 numbers.

Disclosure: The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

I wrote here several times about COOL Co. First time when share price was around 75 NOK about five weeks ago. It is 105 today. Today ABG came out with PT of 154NOK. I remain very bullish on COOL for reasons I wrote before.

A pure LNG shipping company We believe rates could see all-time highs next winter Initiating coverage with BUY, TP of NOK 154

A pure LNG shipping company Cool Company Ltd. (CoolCo) is a pure-play LNG shipping company that owns and operates eight TFDE LNG carriers. The company aims to become a leading player in LNG shipping through consolidation opportunities and offering investors pure exposure to the shipping of liquified natural gas. It aims to keep the fleet exposed to the spot market, and to commit to longer-term time charters when prevailing market rates are deemed favourable. Eastern Pacific Shipping and Golar LNG are the two main shareholders, with stakes of 38% and 31%, respectively.

Gas forward curve yield new ATH for LNG rates in ‘23e Global liquefaction capacity is expected to increase substantially in the coming years and recent events such as the Russian invasion of Ukraine and the EUs acceptance of gas as “sustainable” will likely add even more investments. We expect fleet utilisation above 90% already this year, and as the gas forward curve yields more than USD 1m/day in TCE, we believe rates could hit all-time high next winter. We model for a rate for a 160k TFDE to increase to USD 90k/day in ‘22e, up from an average of USD 87k/day in ’21. Further, we expect the tightening of the LNG shipping market to yield rates of 146k/day in ‘23e and 138k/day in ‘24e, again assuming that European and Asian gas prices remain well above the US price. As such, we model for avg. EBITDA in ’22-‘24e of ~USD 200m, which results in a 36-40% dividend yield in ’23-‘24e.

Initiate with BUY, TP of NOK 154 We initiate our coverage with a target price of NOK 154, derived from a 10% discount to our estimated one-year forward NAV. The forward NAV valuation methodology is based on estimating future asset (vessel) values from forecasted freight rates, which in turn is based on our proprietary supply and demand model. With a limited number of peers in the LNG shipping space, we argue that asset-based valuation is the most applicable pricing method for CoolCo despite modest liquidity in the second-hand market for LNG carriers.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

COOL is one of my top picks to play EU diversification of gas supplies away from Russia. I first wrote here about COOL a month ago when it was trading at 75NOK. It is 95 NOK now. Fearnley says: COOL remains one of the few and best plays on these improving market conditions. They increased their price target from 105NOK to 130 NOK, just three weeks after their initial report. There will be further re-rating. The share price move should remain rapid.

Fearnley Research Summary:

Materializing on Improving LNGC Market

Our take: Likelihood of capitalizing on strengthening fundamentals, revising TP on period market outlook. Reiterate Buy, TP lifted to NOK 130 (NOK 105).

The LNGC market is playing into the hands of COOL with increasing expectations both for prompt and time-charters as political focus on energy diversification and securing supply intensifies. COOL remains one of the few and best plays on these improving market conditions (see our initiation report March 9th).

We see increased likelihood for COOL to lock in strong earnings for its open positions over the coming months and reiterate our Buy rating while revise our (base case) TP to NOK 130 (Buy, NOK 105 March 29, 2022) reflecting USD 100k/d rates for two open positions in 4q22 (in addition to the USD 120k/d TC previously reported in the market). This underscores the operational leverage and further potential in the platform, while appetite for modern tonnage and rising steel values reduces downside risk.

Freight rates and operational leverage Period rates for modern vessels continue to improve with TFDEs now quoted at USD 102.5k/d for 1-year durations followed by 3-year duration at USD 85.5k/d. COOL being one of few with open capacity to the improving market could by locking in the two vessels (opening in 4q22) at USD 100k/d generate additional USD 0.4/s EPS for 2023. Given the rumored (TW) 1 year fixture at USD 120k/d and current market assessment, we argue the 100k level to be on likely and on the conservative side.

Earnings focus over NAV into potential high-cycle We argue NAV lags price development as we head into a potential high-cycle and see earnings as a more appropriate metric to capture current earnings prospects. This is further backed by multi-year charters also seeing strong developments. Rising steel values and limited yard capacity through 2026 (at least at current NB prices) also reduce downside risk together with clear charter preference for modern tonnage. We estimate NAV at NOK 85/sh. and have increased our 2022 EBITDA estimates by 12% and 2023 EBITDA by 18%. Including the two additional TCs we see avg. EPS at USD 2.2/sh over ‘22/’23 which at 7x earnings reflect the NOK 130 TP.

FEARNLEY SECURITIES ACTED AS JOINT LEAD MANAGER & BOOKRUNNER IN CONNECTION WITH THE EQUITY RAISE AND LISTING OF COOL COMPANY

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.