Big day for QFUEL today. Plenty of additional catalysts in the pipeline. Expect wave of broker price target re-ratings. Shorts should be covering. Next two lines modifications should be completed very soon. All four lines should be in operation in Q2. We have been bullish and we are very bullish now.

Terje Eiken, COO of Quantafuel just announced, that he bought 10 000 shares at 21.85 NOK today. Symbolic gesture.

I think there is plenty newsflow in the short term:

- Short covering

- Price target changes – Pareto, and Fearnley placed QFUEL price target under review. It means that they may publish PT uplift. Others should follow

- Completion of modifications on all four lines (within two weeks)

- Start of the production on all four lines (during Q2)

- Q1 results – the previous Q4 was the best presentation I saw from QFUEL. We have a high expectations from Q1 call

- Further announcements on production milestones

- Strategic partnerships progress

Pareto

QFUEL NO – Quantafuel – Proof of Concept at Skive

Quantafuel announces Proof of Concept (PoC) for its Skive plant, being a key milestone to I) further derisk the technology and to II) move forward with larger-scale Plastic-to-Liquid plants (Quantafuel has a pipeline of more than 5 plants). The company defines PoC as >7 days of continuous production with an uptime above 90% at 16,000 tonnes of annual capacity, with an overall oil yield of 68%. Going forward, the company will continue to remove bottlenecks and optimize operational parameters reaching for higher throughput and earnings, which is a normal exercise in the process industry, according to the company. Quantafuel sates that it will revert with a guiding on Skive in due course, and we also believe new FID announcements are not far away. Today’s news is a strong positive and we expect the share to trade higher after declining ~50% YTD. TP under review.

Fearnley

Quantafuel (Under review)

- Reached PoC at Skive

QFUEL announce this morning that the company has reached Proof of Concept (PoC) at the chemical recycling plant in Skive, Denmark, after seven days of continuous production on the two operating lines with an uptime above 90%. This corresponds to an annual intake capacity of 16,000 tonnes of plastic waste at plant level (all four lines). Further guiding for the Skive plant will be announced shortly. Going forward, QFUEL will focus on further optimizing operations and removing bottlenecks, moving towards full operation at Skive and next-generation larger-scale facilities. We see this achievement of reaching PoC, after several delays and required upgrades, as an important step towards successful operations at Skive and supportive of the long-term growth plan. Further, we believe this to have a positive effect on investor confidence.

Sparebank

(+) QUANTAFUEL: Announces proof of concept for Skive. The past seven days it has converted 145tonnes which corresponds to an annual production of 16,000t. The achieved proof of concept equals more than 7 days of continuous production with an uptime above 90% and an oil yield of 68%. This implies just short of 11,000 tonnes of output, which QFUEL has previously announced that it will sell for USD1000/t. Hence, Skive will be expected to have an annual turnover of close to NOK100m after this PoC.

ABG Sundal

Quantafuel declares proof-of-concept for Skive

QFUEL (B) announced this morning that it has reached the very important proof-of-concept (PoC) milestone at its Skive chemical recycling plant. This includes continuous operations at >90% utilization for more than seven days at a level corresponding to an annual capacity of 16.000 tonnes of plastic waste feedstock. The oil yield achieved is 68% vs the long-term guidance for its plants which is 80% (which remains). QFUEL states it will continue to optimize parameters and remove bottlenecks to improve throughput and earnings. The milestone means the roll-out plan can continue with even greater confidence. The company will revert with guidance on Skive, but currently our assumptions for gradual ramp-up towards all four lines in operation by Q4 appears reasonable.

Other trading ideas

- I wrote about Cibus on Friday. We bought at 220 after the SPO and sold at 232. Good one day trade. It is still a great value, it was 260 last week.

- I sold out from very recently Norske Skog at 50% over less than a year. I love the company. It is cheap and plent of catalysts. The major fund is out of lock up now. They always sell shortly after lock up expiry. I will buy back on the SPO. It could be this week.

- We are still bullish on Coolco. We wrote about the company when the share price was around 76 NOK about month ago. It is 96 NOK today. No brainier trade. EU is telling us they will source more gas from other sources than Russia. It means LNG shipping. It is already reflected in the rates. My price target is 130NOK. I believe we could be there within a month

- I am bullish on Biovica. The story takes longer than I thought, the value is there in my view. Company provided bullish updates last week. Could be one of the best performing positions this year.

- We are also long other pharma names: Sedana, Bioinvent, Ascelia, Vicore, Hofseth Biocare and Eigr.

- We remain strongly bullish on Linkfire. They provided very strong guidance at Q4, which the market ignored. Again, this could be one of the best performing stocks this year from my portfolio. There is my article on Linkifre on SeekingAlpha and plenty on this blog.

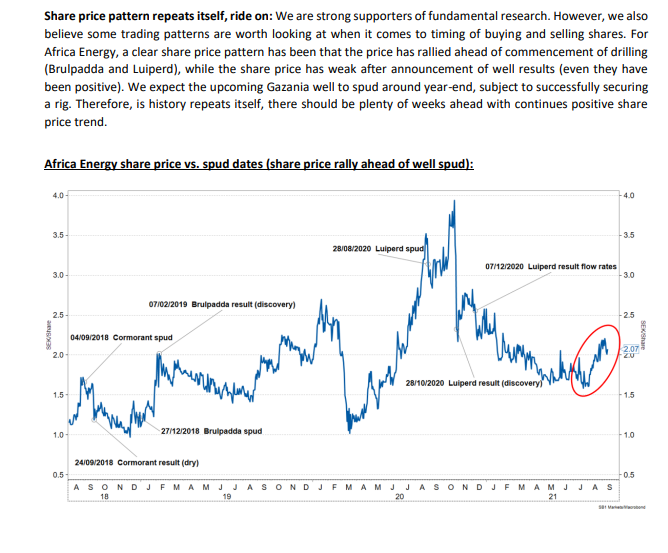

- I am long oil through Africa oil, Africa Energy, AkerBP, and Var Energi. Var is out of blackout today. 8 brokers that were in the IPO syndicate should publish their research. Very bullish short term for Var.

- I am bullish on Aker Horizons. Last week transaction showed, that these guys can deliver. AKH trades at 15% discount to NAV according to Pareto. AKH was caught by the renewable sell off last year. I believe that we are seing a reversal now.

- I am long Fusion Fuel Green. Similar story like AKH. I expect this to be at least doubling candidate this year.

- I am also very bullish on Huddly. The management was buying in recent weeks. So we were. Again, this stock should double in next two quarters.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.