On Friday, the S&P500 stock index closed above 5000 points for the first time in history, and in this context, I would like to share some fresh and interesting numbers.

We reached 5000 from lows close to 4000 at the end of October last year, since then we have witnessed growth in 14 of the 15 trading weeks (by more than 22% overall).

The last time we recorded similar statistics was at the turn of 1971 and 1972. It took the index 757 days to get from 4,800 to 4,900, but only 15 calendar days to move another 100 points to 5,000.

Europe has also seen a stock rally, and the EURO STOXX50 index has finally surpassed its 2007 pre-financial crisis levels. The broad pan-European STOXX600 index has also come within striking distance of its all-time highs.

The rise in the S&P500 index is once again driven by stocks from the “Magnificent 7” basket, representing a third of the index’s market capitalization, which have risen by more than 38% since 27.10.23. Since the beginning of the year, it is 18% against 5% of the entire index.

And once again, stock prices are tracking earnings growth, as of 27.10.2023 the expected profit for the next twelve months for the “Magnificent 7” has increased by more than 16% against almost zero growth for the rest of the index. We have already discussed this phenomenon at our Investment Breakfast in October 2023. If we put the above in the context of the fact that over the same period, the yield on the ten-year US bond has fallen from values close to 5% to values attacking 4% from above, the explanation for the growth of stock indices is obvious. In addition, after the so-called “pivot” from the December meeting of the Fed, there was a significant easing of financial conditions, which led, and will continue to lead, to good macroeconomic indicators in the US in the first quarter of this year. At the same time, however, this may lead to an increase in inflation expectations and a revision of monetary policy in the rest of the year, with an impact on interest rates and the valuation of risky assets. Regarding the expected development in the coming weeks, it is also good to remember the rule “tops are a process, lows are a moment”, which says that the search for the top may take some time. Stock rallies of a similar magnitude to the one we are experiencing do not respect valuations, but only interest rates, more precisely real interest rates, so this parameter will be the most important factor in the near future. In terms of valuation, the “Magnificent 7” shares will continue to have the greatest impact on the value of the index, and a detailed analysis of their valuation has been published on this platform by Aswath Damodaran. According to the professor, the prices of these shares already reflect the uniqueness of the business models of these companies that bring growth and profit. His conclusion is that those who have not owned shares so far will not be able to make up for their losses with the current purchase and points out that even the best companies sometimes bring disappointment, to which the markets overreact, and at such a moment it is good to buy.

Written by Leos Jirman of Emun Partners, emphasis added

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Vicore, Bioinvent and Hofseth all reported positive news today.

Vicore Pharma

Vicore Pharma is the global leader in Idiopathic pulmonary fibrosis (IPF). IPF is a condition in which the lungs become scarred, and breathing becomes increasingly difficult. Vicore has the best-ever results in their study. This year, the company is planning its 2B study, which may be used for the FDA approval.

Vicore Pharma announced this morning that they have signed an out-licensing deal for C21 in Japan. This is a strong deal that validates the potential for C21 in the IPF indication. The company received USD10m upfront and can receive an additional USD275m in milestones and royalties or 20%+ on sales in the end.

Nippon Shinyaku looks to be a strong partner in Japan. The Japanese market for IPF is relatively large, and Nippon Shinyaku already has a strong footprint within the rare respiratory disease market.

Nippon Shinyaku will be operationally and financially responsible for the future development of C21 in Japan.

Vicore trades at a fraction of market value vs the US peers, which have much worse results while being at the same stage of development. Vicore retained a new US-based CEO who is introducing the company to the US investors. The top US industry specialists have already invested.

Bringing US investors on board is low-hanging fruit. Last week, the company announced they’re attending the conferences below. this was not happening under the previous CEO. Big progress:

Guggenheim 6th Annual Biotechnology Conference Location: New York, NY. Fireside Chat Date and Time: February 7 at 2:30 PM ET/ 8:30 PM CET. Webcast Registration: Link

Oppenheimer 34th Annual Healthcare Life Sciences Conference Presentation Date and Time: February 13 at 10:40 AM ET / 4:40 PM CET. Webcast Registration: Link

BioInvent

BioInvent is a clinical-stage company that discovers and develops antibodies for cancer therapy.

Bioinvent has: – 5 Projects in clinical development – 10+ Licensing, supply and collaboration agreements – 108 Employees (full-time equivalent) – 1,358 SEKm in liquid funds etc

BioInvent today announced a clinical supply agreement with AstraZeneca to evaluate BioInvent’s antibody BI-1206.

BI-1206 is one of BioInvent’s most advanced drug candidates and is developed to re-establish the clinical effect of existing cancer treatments such as pembrolizumab and rituximab, drugs with combined global sales of approximately USD 23 billion annually.

The drug candidate is evaluated in two separate clinical programs, one for the treatment of non-Hodgkin’s lymphoma (NHL, a type of blood cancer) and one for the treatment of solid tumours. Two delivery formulations (intravenous (IV) and (subcutaneous (SC) of BI-1206 are being evaluated in parallel.

Bioinvent announced today: – Clinical supply agreement with AstraZeneca to support Phase 1/2a BI-1206 combination study – BI-1206 to be evaluated in combination with Calquence® and rituximab in Phase 1/2a trial in non-Hodgkin’s lymphoma – The ongoing rituximab combination trial will be expanded to include the triplet arm Pareto analysts wrote today:

“This increases the chance that BI-1206 will eventually reach the market, while also increasing the potential market itself. With BINV slowly but steadily growing while being well funded, we reiterate our Buy rating on BINV with a target price of SEK 134. ”

Hofseth BioCare (HBC) is a high-tech tech, fully integrated business that takes off-cuts from salmon and produces high-value health nutritional products for people and pets. The company gradually transforms its portfolio into human health high margin products.

Hofseth Biocare today announced it delivered 80% revenue growth in 2023 vs 22. The company CEO issued positive guidance, saying they expect “further 50% revenue growth in 2024, higher capacity utilisation and positive EBITDA in 2024”

Norsk Titanium (Euronext: NTI), a global leader in additive manufacturing for aerospace-grade structural titanium components using its patented Rapid Plasma Deposition® (RPD®) technology, announces development of Inconel 625 for US Navy applications.

NTI recently announced material progress in their cooperation with Airbus. Today NTI announced that under a contract with Bechtel Plant Machinery, Inc. (BPMI) Norsk Titanium has adapted their industrialized RPD® process for Inconel 625. As part of the ongoing effort, Norsk Titanium and BPMI are developing the deposition parameters and heat treatment process needed to produce additively manufactured Inconel 625 with material properties equivalent to legacy castings and forgings.

Inconel 625 is used in US Navy applications that require high strength and resistance to corrosion. Bechtel Plant Machinery, Inc. is developing new manufacturing processes for Inconel 625 to deliver cost and schedule savings to their customers as well as developing alternating sources of supply for crucial materials.

“This initial effort is an important first step in opening the nickel superalloy market to our additive process,” said Nicholas Mayer Norsk Titanium Vice President of Commercial. “We look forward to taking the learning from this effort, and applying it to specific Naval applications,” added Mr. Mayer.

Norsk Titanium has recently announced qualification and production milestones in their core commercial aerospace titanium market. The addition of nickel superalloys and maritime applications is a key part of Norsk Titanium’s long term growth strategy.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

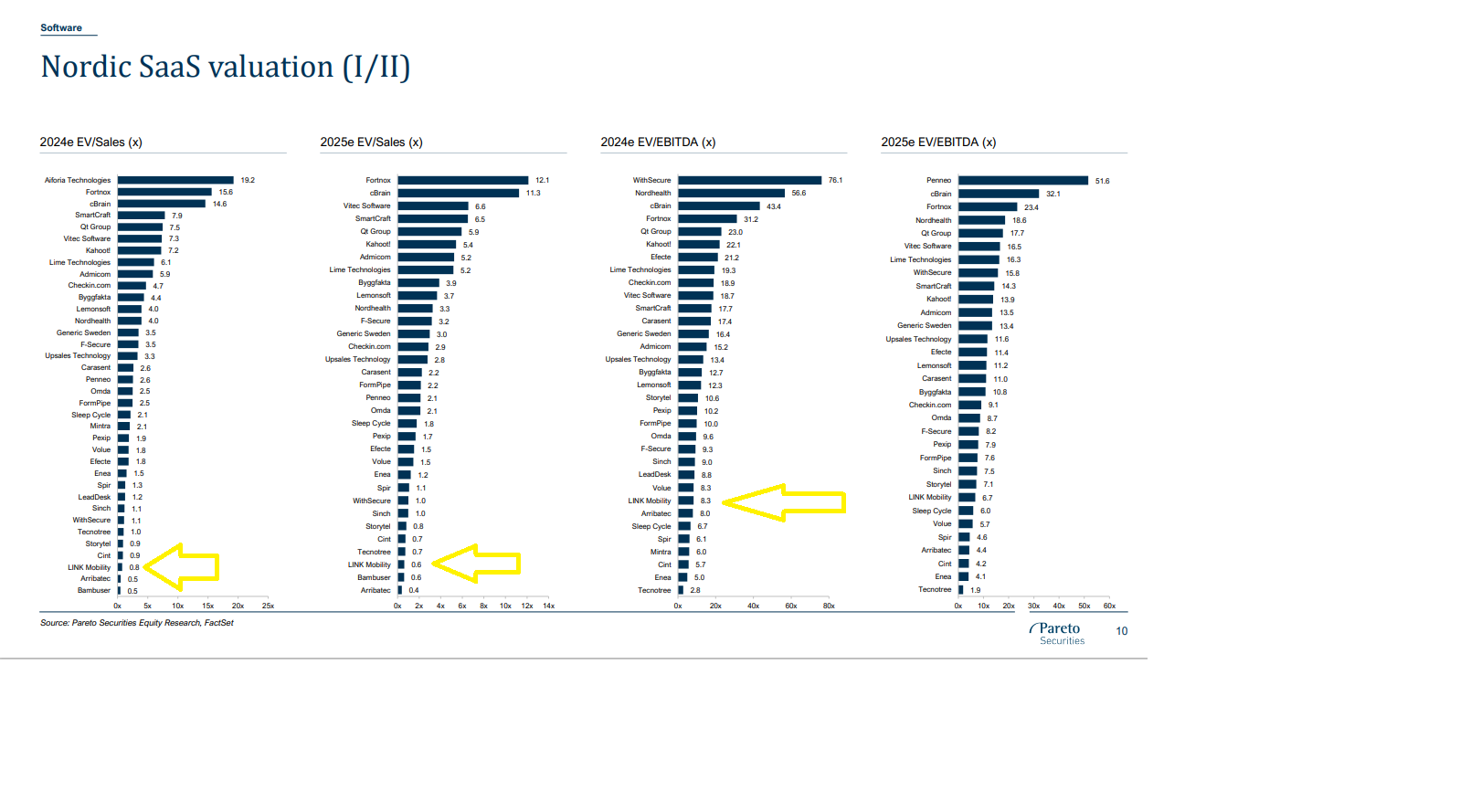

Link is the top idea by SpareBank analyst Petter Kongslie. Link is Europe’s number one in helping companies and state institutions communicate with their customers through SMS, WhatsApp, Wiber, Instagram, and other messaging platforms. If you fly, and get a boarding SMS, it could be from Link.

The major catalyst happened in early January – Link closed the sale of its US subsidiary at 14 times EBITDA. Link trades at 8 times EBITDA. Its core business has similar profitability metrics as the disposed US business. The transaction indicates the upside.

Link is one of the cheapest Scandinavian SaaS companies. The reason was its high leverage of 4.5 times EBITDA. The USD 260 million US subsidiary disposal reduced the leverage to around 1 times of EBITDA. The leverage issue is now resolved. Share price re-rating should be next.

The company has been growing organically at 14% (12% from existing and 2% from new clients). The growth is expected to continue. Further growth may be achieved through market consolidation. The company has a great track record of 30 acquisitions. After selling its US business at 14 times EBITDA, Link can now buy companies at 5-6 times EBITDA (its histrocial track record) to increase its growth further.

LINK in Short

LINK Mobility is a Communications Platform as a Service (CPaaS) provider, providing communications products and services to enterprises, helping them to drive customer engagement and increase customer satisfaction at every part of the customer journey.

LINK has 650 employees in 30 offices across 18 countries in Europe and the US

Revenue close to NOK 6 billion

Adjusted EBITDA above NOK 700 million => EBITDA margin 12%

LINK has 50 thousand customer accounts globally and exchanges 18 billion messages a year

In Norway, Link has a 2/3 mkt share, Sweden 50%, and in other European countries, top three positions with a 10-30% market share.

LINK was founded more than 20 years ago and relisted on the Oslo Stock Exchange in 2020 after being taken private in 2018.

Link is very cheap vs peers.

See Pareto´s relative valuation.

The leading Scandinavian brokers have all turned very bullish in January :

The Arctic Securities – published on 15 January 2024 research titled: “Link Mobility – Getting the message across – one to own in 2024.” Their Price Target is 23 NOK, a 30% upside from the current share price.

Pareto Securities – initiated their research coverage on 22/1/24 titled “Back to basics” with a Price Target of 25NOK, a 50% upside from the current share price.

Sparebank published their latest research on 8/1/24 titled “We expect business as usual in 4Q23 and solid free cash flow” with a Price Target of 25 NOK, a 50% upside from the current share price.

ABG Sundal Collier published their latest research on 23/1/24 titled “Link Mobility – An Undervalued Quality Company” with a Price Target of 24 NOK, a 40% upside from the current share price.

The Q4 report will be crucial. The company will provide details on the restructured and deleveraged company plus an update on aquisitions. I expect further rerating after the Q4 report. Our price target is 25 NOK for now. If the Q4 report is as bullish as we expect, we will increase our price target to 30 NOK.

What is next?

Link is deleveraged. It can:

Continue acquisitions at 5-6 times EBITDA. The company has a successful track record of 30 acquisitions in Europe. This will further accelerate the growth rate above the organic 14%. In the past, the share price reacted positively to well-priced acquisitions. We expect this to continue.

Buy back its shares or pay dividends. The current bond limits both; Link can buy back the debt. We believe this is less likely. Profitable growth will be the main focus.

The next catalyst is the Q4 report on 15 February. If the report is positive, expect the price target updates in the days after the report. It has most likely accumulated a portfolio of acquisition candidates, which should be taken over in the coming months. The share price is most likely to react positively to the announcements.

Summary

Link is cheap vs its peers as the Pareto slide shows. Link is cheap vs the transaction it just closed in the US. The reason for its low valuation was its high leverage, which is now resolved. Link is growing organically at 14% with a high cash conversion rate. Likely, acquisitions at lower multiples will accelerate growth further. Link successfully integrated 30 acquisitions into the profitable enterprise. It will do so in the future as well. Bright days ahead.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Our top ideas for the coming year. Our family office has a position in all the below.

Golar LNG

Golar LNG Limited

Golar LNG builds, owns, and operates marine infrastructure for LNG liquefaction and regasification, with a market cap of $2.3 billion.

Golar’s assets include FLNG vessels currently working for Perenco, with the potential for new contracts that could double EBITDA.

The arrival of FLNG Gimi to the BP offshore field and its operation in late 2024 will increase Golar’s EBITDA by 50% and potentially result in a dividend hike.

The Investment case is supported by dividends and a USD150 million buyback.

Strong catalysts in the next six months.

The new contract for GLNG’s largest liquefaction vessel, Hili, will be a major catalyst for the stock – it has the potential to double the current EBITDA. The announcement is expected in the next six months.

The arrival of GLNG´s second liquefaction vessel, Gimi, to the BP offshore field – is expected in January 2024.

The commissioning of Gimi is expected to be in the first half of 2024. During the commissioning, GLNG will start earning revenues from BP

Operation of Gimi – expected late 2024

Refinancing of Gimi debt – expected after Gimi operation.

Increase of dividends/buybacks – the operation of Gimi should result in a dividend hike. Currently, Golar pays USD 1 per share. Consensus assumes a 100% dividend hike to USD 2.

Conversion of FLNG Fuji – the ship will be delivered to Golar in early 2024. Further details on its FLNG conversion timing and potential contracts would be very value-creative.

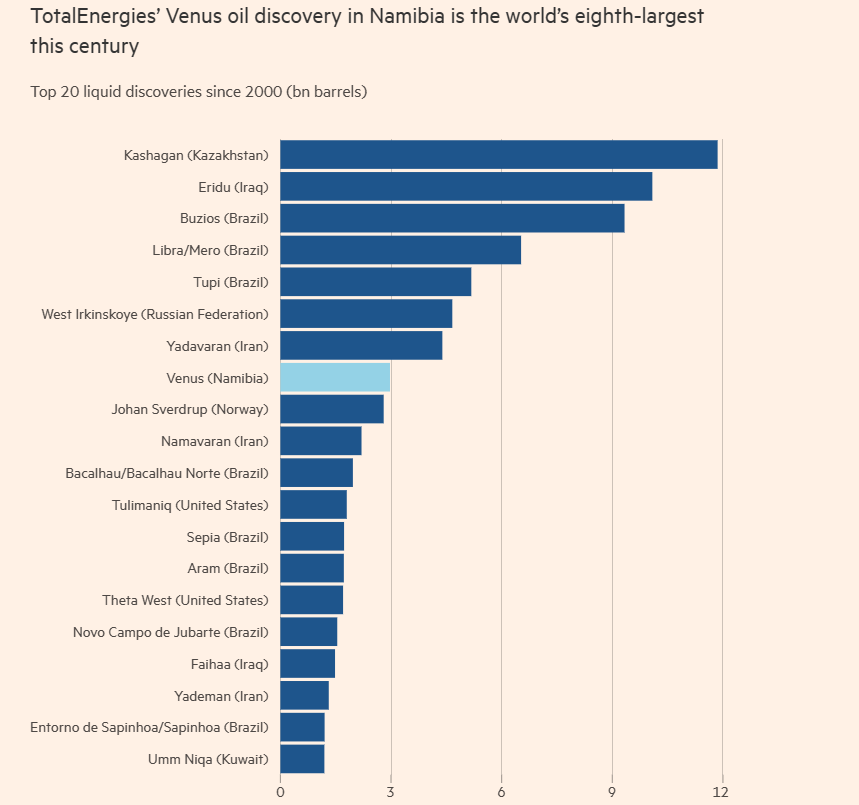

Africa Oil owns a 6% stake in the Venus discovery, the 8th largest discovery made in the 21st century.

TotalEnergies is the largest investor and operator of Venus. Total calls Venus “Golden Block”. Total is spending 50% of its global exploration budget on Venus.

Retail investors speculated on Venus’s size disclosure during Total’s Capital Market Day through Africa Oil shares, causing a 30% drop in its share price. That made the opportunity more attractive.

The second Venus well results are expected to be published by the end of November. That should further certify Venus’s size and push the Africa Oil stock up.

Africa oil At 19 SEK/sh, the Venus discovery/ Namibia exposure either is not reflected in the share price at all, or ii) Venus is reflected, but AOI’s production in Nigeria is valued at EV/GAV ~0.3x.

Either way, we find the 19 SEK/sh entry point in AOI to be highly attractive. Total has drilled two wells on Venus. Results for both will most likely be communicated in connection with TotalEnergies Q4 results February 7th).

Vicore Pharma

If Vicore were a US-listed company, its valuation would be multiple times higher. The best proof is Pliant, a company in a similar state of development with much worse drug results. Vicore hired a new Boston-based CEO whose claim is to connect Vicore to a US investor base. Just before the year’s end, Vicore also hired a new Chief Medical Officer with experience in respiratory medicine from AstraZeneca and Galecto. Just connecting the story to US investors should strengthen the share price materially. Top US professional pharma investors have already entered the last capital raise. This should continue in 2024.

In cancer treatment – the speed of cancer monitoring drives survival. Biovica breast cancer tests can quickly detect whether the selected medication is working.

Biovica biomarker breast cancer test can detect cancer progression at least 60 days earlier than imaging. And 3-10 times cheaper.

Bloomberg just reported, “Biomarkers are Dramatically Changing Cancer treatment”. Biovica was the first-ever FDA-approved Biomarker test for cancer. It has the potential to be one of the market leaders.

Very strong clinical data – 28 studies including from the most prominent US hospitals (Mayo Clinic, John Hopkins, the Dana-Farber Cancer Institute).

Market potential > $2 billion for monitoring of metastatic cancer.

Linkfire presents a unique Private Equity deal opportunity.

Linkfire was listed in 2021 at 7 times higher capitalisation than it is today. The company is due to be delisted on 14 January 2023. After delisting, the company will start the process of selling itself to a strategic partner. The founder and CEO resigned from their positions to focus on the sale of the company. If this succeeds, it is a multiple-times opportunity.

Titanium printing consumes up to 80% less titanium in the production of parts for aviation and defence. Being first in the field is an opportunity and risk:

Aviation is a highly regulated industry – to break through the licensing takes a long time.

Once this is achieved, the opportunity is very material – Norsk Titanium can disrupt traditional titanium producers.

ERII is one of very few highly profitable renewable companies.

ERII has a $1 billion market cap, zero debt, $100 million in cash, 72% margins, and 20% revenue CAGR.

Energy Recovery dominates the global industrial desalination industry, having a 90% global market share.

ERII is now trying to copy its technology into a new global segment – industrial air-conditioning and refrigeration.

Due to Kigali protocol, all greenhouse gas industrial air-conditioning and refrigeration systems need to be replaced with CO2 systems.

Energy Recovery devices can save up to 40% of energy in the new CO2 devices. ERII has a 25-year track record and no major competition.

Next year will be the year of transformation for its industrial air-conditioning and refrigeration products. ERII guides it to install the product in 50 locations this year. This should cause major revenue updates for the coming years.

Renewables trade like growth stocks. Both are very sensitive to interest rates. SpareBank published a very nice illustration.

The graph illustrates how renewable stocks have been hammered by raising rates. The graph also shows that the yields have been reversing from the November FED pivot, as has the renewable index. So, if you believe the rates have peaked, you should look at renewables.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

A lot has been said about the recent announcement of the Gazprombank cooperation. We saw a lot of speculation in Africa Energy forums. Below is my read of the situation.

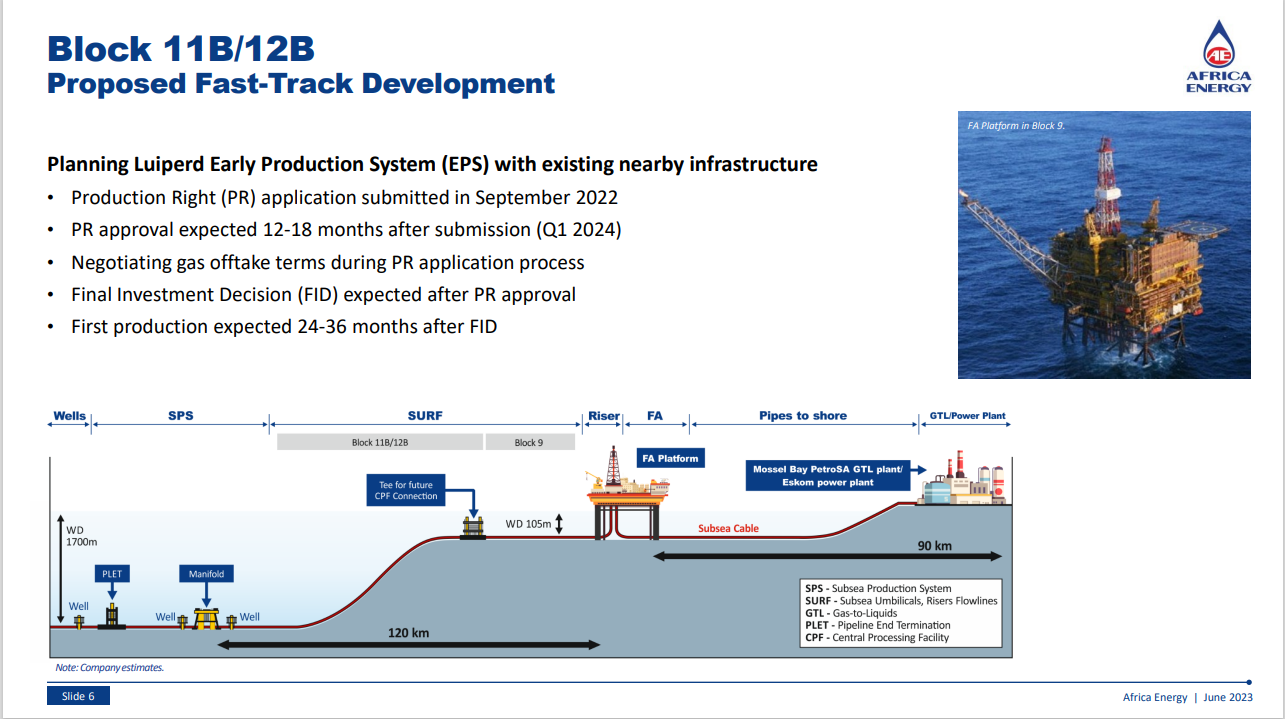

Africa Energy owns 10% interest in Block 11B/12B, one of the most significant recent gas condensate discoveries offshore South Africa. The major shareholder in the Block 11B/12B and the operator of the field is Total Energies.

The Total has applied for production rights to the SA government, and the approval is expected in the middle of next year. Total has been engaged with relevant authorities to attempt to negotiate an offtake for the gas. Our base case is we should see the offtake agreement concluded next year as well. After that, Total will proceed to commercialisation. At that stage, Africa Energy would either sell its 10% stake in the Block or participate in its development.

There are potential off-takers for Total/Africa Energy gas from field 11B/12B Petro SA, Eskom, or independent off-takers in the form of Gas to Power Plants. Both Petro and Eskom are state-owned by the SA.

Eskom produces electricity by burning diesel. In June, Eskom announced a tender for converting its facilities from diesel to gas. This is positive for Total. Tender results are yet to be announced. When done, Eskom can be supplied gas by the Total consortium from block 11B/12B.

Petro SA has been a major SA supplier of diesel from their gas to diesel conversion facility. Mossgas Plant was the major supplier of diesel during the apartheid times.

Petro also supplies Eskom, which uses diesel to produce electricity.

Petro had been using gas from a nearby offshore field. Petro owns the offshore infrastructure used to transport the gas from the offshore field to its facilities. Total consortium assumes that they COULD be using Petro´s infrastructure to transport the gas from 11B/12B to Mossel Bay. Since late 2019, the nearby gas field has been exhausted, and the Petro SA facility is operating at a minimum level.

Petro SA ran a tender for an upgrade of its facilities. There were 20 participants in the tender. 19 participants were eliminated from the tender due to Petro´s requirement that the selected bidder must be at least partly government-owned. Only GazpromBank has satisfied the state-owned condition and won the bidding. The condition was widely criticised by SA opposition and local and international media.

The contract terms are confidential. What was reported in the press:

The contract is only for USD200 million refurbishment of the Petro´s Mossel Bay plant

GazpromBank will finance the refurbishment and will obtain a profit share from the plant operation

No press report mentioned that GazpromBAnk would be supplying LNG to Petro

No press report mentioned that the gas infrastructure used to transport gas from the offshore field to Mossel Bay would be part of the deal GazpromBank contract.

The contract has one condition precedent – both parties can step out until FID is reached. That is expected in April. Due to the criticism of the tender process, any outcome may be possible.

In summary, nothing has changed in the business case for Total and Africa Energy shareholders. The contract only secures, that Petro would be well-positioned to be an offtake customer for the Total/Africa Energy consortium.

Our family office is Long Africa Energy. We believe when the Production Rights are granted, and the Offtake Agreement secured, the Africa Energy share price should be several times higher than the current levels.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Golar LNG builds, owns, and operates marine infrastructure for LNG liquefaction and regasification, with a market cap of $2.3 billion.

Golar’s assets include FLNG vessels currently working for Perenco, with the potential for new contracts that could double EBITDA.

The arrival of FLNG Gimi to the BP offshore field and its operation in late 2024 will increase Golar’s EBITDA by 50% and potentially result in a dividend hike.

Strong catalysts in the next six months.

The investment case is supported by dividends and a USD150 million buyback.

alvarez

Introduction to Golar LNG

Golar LNG Limited (NASDAQ:GLNG) builds, owns, and operates marine infrastructure for theliquefaction and regasification of LNG. It currently owns two out of nine existing FLNG ships in the world, which positions it perfectly for the projected LNG deficit in Europe.

Golar has a market capitalization of USD 2.3 billion, a net debt of USD 1.0 billion, and an enterprise value of USD 3.3 billion. In 2022, Golar generated an EBITDA of 360 million in 2022.

The company has been historically trading at EV/EBITDA multiple of 6-8 times.

Golar Assets

Golar is focused on Floating liquefied natural gasvessels (FLNG) designed to facilitate the production, liquefaction, and storage of natural gas at sea. If you have a producing well at sea, you can add an FLNG vessel and liquefy the gas for transportation on the sea. Golar has the following vessels:

FLNG Gimi – was delivered to Golar in November (construction costs USD 1.7 billion). Gimi is now on its way to Nigeria to start its 20-year contract for BP.

FLNG Fuji – was acquired for USD 77 million, delivery is scheduled for 1Q24 – USD 177 million deposit for conversion already made by Golar.

Golar Arctic – LNGC carrier contracted with an Asian Shipping company. Golar already divested 15 LNGC carriers – Golar will most likely divest Golar Arctic as well.

Hilli – New Contract Could Double Golar EBITDA

The current Hili contract with Perence expires in mid-2026. A new contract has not been announced yet.

The Perenco contract covers only 50% of Hilli’s design capacity. It means only 50% fees vs its potential fees.

Golar is now looking for a new contract that would have a higher utilization.

Any improvement will have a positive impact on the EBITDA contribution from the unit.

For instance, assuming a 90% and similar pricing as the current contract would almost double the current EBITDA of USD 371 million to USD 668 million.

Golar LNG stated that it is in detailed discussions with three specific parties regarding new employment opportunities for FLNG Hilli.

The company anticipates that contract lengths could be between 10 and 20 years.

If you assume the new contract at 90% utilisation – the EBITDA would increase by USD 300 million.

If you apply the EV/EBITDA range of 6-8 times, the new contract would increase Golar´s Enterprise value by USD 1.8 – 2.4 billion. That is a material upside vs the current market cap of USD 3.3 billion.

The market expects the new contract to be announced in the next 6 months. This will be a major catalyst for the stock.

Gimi – The BP Contract Will Increase Golar EBITDA by 50%

The new FLNG Gimi, delivered to Golar in November, is now on its way to the BP offshore field located offshore between Senegal and Mauritania.

Arrival is expected in January 2024.

Once Gimi arrives, Golar will start earning revenues – BP will start paying Golar standby fees.

Once the commissioning starts, Golar revenues will further increase.

Once in operation, Gimi should generate an EBITDA of USD 215 million.

Golar will collect 70% of that – USD 150 million.

The Gimi operation is expected to commence in late 2024.

Gimi’s operation should increase Golar´s current EBITDA by 50%.

The increased cash generation should result in a dividend hike.

Once Gimi is in operation, Golar is expected to refinance the USD 700 million of its debt with a lower interest margin. The refinancing would increase Golar’s profitability and its cash flows to equity holders.

Dividends and Buybacks support the investment story

Golar has been paying a dividend of $0.25 per share per quarter, which represents a 5% dividend yield. After the Gimi operation commences next year, the dividends should increase. Market consensus expects dividend doubling.

During the last quarter, Golar repurchased 0.2 million shares at an average price of $21.36. The company still has $117 million remaining from its approved buyback scheme of $150 million.

Strong catalysts ahead

The new contract with Hili will be a major catalyst for the stock – it has the potential to double the current EBITDA. The announcement is expected in the next six months.

The arrival of Gimi to the BP offshore field – is expected in January 2024.

Commissioning of Gimi – expected in the first half of 2024

Operation of Gimi – expected late 2024

Refinancing of Gimi debt – expected after Gimi operation.

Increase of dividends/buybacks – the operation of Gimi should result in a dividend hike. Currently, Golar pays USD 1 per share. Consensus assumes a 100% dividend hike to USD 2.

Conversion of FLNG Fuji – the ship will be delivered to Golar in early 2024. Further details on its FLNG conversion timing and potential contracts would be very value creative.

Sale of Golar LNG.

Conclusion

There are strong catalysts ahead supported by USD150 million buyback. After a few quiet years, strong news flow and material EBITDA jumps should rerate the stock in the next year.

Golar fell 5% following its earnings release last week despite no major surprises. A good entry point for both short-term and long-term.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

“I have invested 10 Mil NOK in the capital raise” “Our US team invested most of their bonuses into the capital raise. This was a great sign of confidence for me”

Important CEO quotes from the report:

We made progress during the quarter in all three of our priority areas, which are the USA, Europe and collaboration with pharmaceutical companies.

We have thus far announced the signing of three agreements with major hospital chains. They are with leading healthcare providers in the states of Arizona, Florida and Missouri. In total, these agreements cover approximately 50 hospitals.

A summary from both studies will be presented as posters in December at the San Antonio Breast Cancer Symposium (SABCS), which is the world’s largest breast cancer symposium.

We are also delighted by the enthusiasm we are seeing from oncologists who keep ordering the assay via our CLIA lab in San Diego. They have been placing regular orders, and many are even increasing the frequency of their orders.

… we anticipate that there will be ten agreements signed with major hospital chains by the end of the financial year,

In Europe, our goal for quite some time has been to sign partnership agreements with the five largest, most populous countries in the EU (Italy, Spain, Germany, the UK and France) plus the Nordics. We have already achieved that in Italy, and our progress with negotiations indicates that we will have another agreement signed by the end of the fiscal year.

Subsequent to the end of the period, we signed a commercial partnership agreement for the Nordics with Axlab, which is one of the leading companies for cancer screening and diagnostics in the Nordics.

Three new projects started up during the period, which means that we now have 19 ongoing projects for collaboration and sales to pharmaceutical companies that are developing new cancer drugs.

With great optimism for the future, I will myself be subscribing for SEK 10 million in shares.

Biovica Q2 (August to October): Confirmation about commercial progress

The recent CMS Medicare price of USD 322 is the last progress during a quarter of improved presence, including Direct Bill, Hospital contracts, pharma partner projects and European distribution. Actual sales is in line with our expectations at SEK 2.5m, and Biovica reiterates the outlook, including higher DiviTum test volumes during calendar H1 2024. We are in the process of reviewing our Base Case (SEK 27, Bull SEK 60 and Bear SEK 5) reflecting an increased number of shares related to the ongoing rights issue.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

In current markets, securing funding for breaking-even companies is not easy. Companies are pressed to issue equity at draconian terms. Linkfire just announced it secured EURO 5 million in debt funding from Mr Kuok Meng Ru, founder of BandLab, who is also LInkfire’s 4th largest shareholder. A very great achievement in current markets is a rubber stamp on the project from a major industry player.

Linkfire A/S secures debt financing of DKK 37.3 million (approx. EUR 5 million) on an improved interest basis to strengthen cash preparedness

Linkfire A/S (“Linkfire” or the “Company”) announces that it has secured debt financing of DKK 37.3 million from Kuok Meng Ru, a shareholder of Linkfire and Group CEO & Founder of Caldecott Music Group (“CMG”), as an expression of his commitment to and belief in the Company’s potential.

The terms of the financing agreement are similar to the terms previously announced (see the corporate announcement from 9 May 2023), whereas the financing is structured as a drawdown facility and carries a reduced annual interest rate of 17 per cent compared to 18 per cent previously, accruing on each draw of the facility and paid quarterly. The board assesses the interest level to reflect current market terms.

The facility has a duration of 2.5 years. It is repayable in whole or in part in the interim in case of future equity or debt raises during the term of the loan.

The loan will be deployed to repay part of Linkfire’s existing loans under the previously announced credit facility, contribute to financing the Company’s operations until cash flow break-even expected in 2024, and allow Linkfire to continue various avenues in its pursuit of maximizing shareholder value. The expected net proceeds from the loan is approximately DKK 20 million and will be utilized for the Company’s operations.

The debt financing is a testament to Kuok Meng Ru’s continued belief in the Company’s potential and unique market position.

Linkfire is reporting tomorrow before the open

Linkfire hosts a Q3/2023 interim report webcast on November 23, 2023

Linkfire (NASDAQ: LINKFI.ST) will publish its interim report for the third quarter on Thursday, November 23, 2023, at approximately 7.30 AM CEST. A webcast for investors and media will take place at 10.00 AM CEST on the same day.

The report is presented by Lars Ettrup, Co-founder and CEO, and Tobias Demuth, CFO. The presentation for the webcast can be downloaded on https://investors.linkfire.com/ 30 minutes before the webcast starts. A recording of the event will be available on the same website later the same day.

In addition to the Q&A at the end of the webcast, participants also have the possibility to preregister questions via email to investors@linkfire.com. The Q&A session is moderated through a chat function, which will be available via the webcast link below.

Please register for the webcast using this link: https://lnk.to/Q3-23 After registration, you will receive a link to access the webcast via e-mail.

What to expect from the Q3 report

Last year, Linkfire announced that 2023 is the first year the company will be EBITDA positive. Tomorrow’s Q3 report might be the first EBITDA positive quarter. If that is achieved, it would be a major milestone in Linkfire’s history.

We are long LInkfire.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

If Vicore were a US-listed company, its valuation would be multiple times higher. The best proof is Pliant, a company in a similar state of development with much worse drug results. Vicore hired a new Boston-based CEO whose claim is to connect Vicore to a US investor base.

The new Vicore CEO is now starting to talk to US investors. He has a strong investment proposition – no other drug has ever had such strong results in IPF.

Vicore presentation at the Stifel conference – last week, Vicore CEO attended the Stifel 2023 Healthcare Conference in New York. The link to his PDF presentation is below:

During the conference, the CEO will make a presentation to the whole conference, plus he will have an opportunity to have one-on-one meetings with certain investors.

What is positive – Vicore is getting invitations to such conferences. Stifel would not invite Vicore unless they believed they would be able to do trading with their stock or get a mandate for a future capital round.

We heard Vicore is attending a conference in February hosted by Guggenheim and are talking to other US-based brokers on investor roadshows.

This is all new for Vicore. Very new. Getting US investors on board is the first step to re-rate the Vicore share price.

Our family office believes Vicore is one of the holdings with the highest upside potential in our portfolio.

Do watch the webcast.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Africa Oil owns a 6% stake in the Venus discovery, the 8th largest discovery made in the 21st century.

TotalEnergies is the largest investor and operator of Venus. Total calls Venus “Golden Block”. Total is spending 50% of its global exploration budget on Venus.

Retail investors speculated on Venus’s size disclosure during Total’s Capital Market Day through Africa Oil shares, causing a 30% drop in its share price. That made the opportunity more attractive.

The second Venus well results are expected to be published by the end of November. That should further certify Venus’s size and push the Africa Oil stock up.

Jeremy Poland

Introduction to Africa Oil

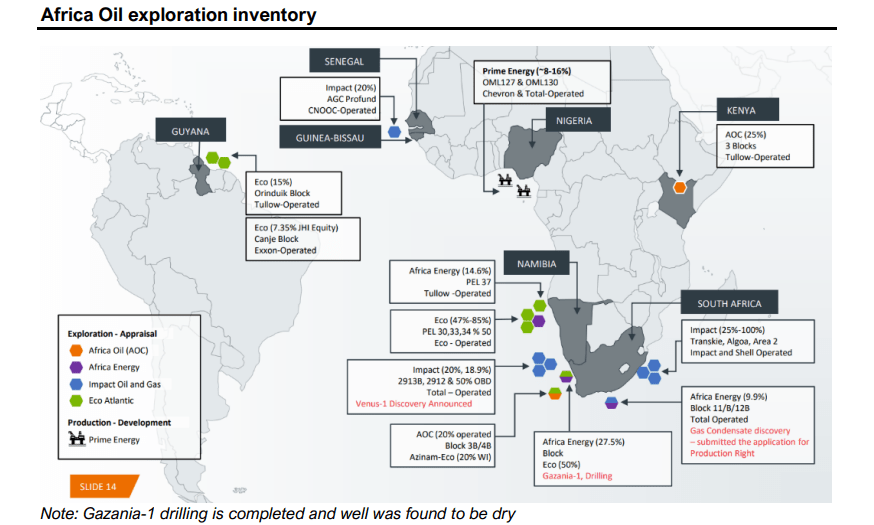

Africa Oil Corp (TSX:AOI:CA) (OTCPK:AOIFF) is an upstream oil corporation that was founded in 1988 and headquartered in Vancouver, Canada. Its core lies in exploration assets located in the nascent and under-explored terrains of West and East Africa.

Africa Oil is listed in Toronto (TOR: AOI) and Stockholm (STO: AOI). The market capitalization is CAD 1.2 billion (USD 850 million). The 2023 Revenues, EBITDA, and Net Profit are estimated at USD 300 million, USD 270 million, and USD 210 million, respectively. The company has a year-end 2023 projected Net Cash position of around USD 200 million.

Africa Oil’s strategic capital allocation and disciplined financial management have helped maintain a strong balance sheet, enabling it to weather the volatile phases of the oil industry.

Africa Oil owns two operating assets, two major oil discoveries, and several prospective resources:

Operating Assets

Africa Oil owns 3 of the top 5 oil-producing fields in West Africa through its 50% stake in Prime:

Agbami field (OML 127) is operated by Chevron (CVX), and Africa Oil owns an indirect 4% stake.

Egina, Akpo (OML 130) is operated by TotalEnergies (TTE), and Africa Oil owns an indirect 8% stake.

Both production assets are in Nigeria. The company has a long-lived production base of 20,000 bbl/day net to AOI with very low operating costs of around USD8/bbl.

The three producing assets generated Net Revenues to AOI of USD 138 million and USD 300 million in 2022 and projected 2023. respectively.

Prime Track Record

The three West African oil-producing wells illustrate greatly AOI capabilities:

AOI bought a 50% stake in Prime in January 2020 for USD 520 million.

In three years, AOI collected USD 713 million in dividends from Prime.

If oil would remain at USD 70 per bbl, AOI should receive at least USD 150 million in dividends from Prime over the next three years. With oil at current prices, the annual dividend would be significantly higher.

I believe it could be a great investment with strong cash flows coming for the years to come.

Discoveries – Venus of the Century

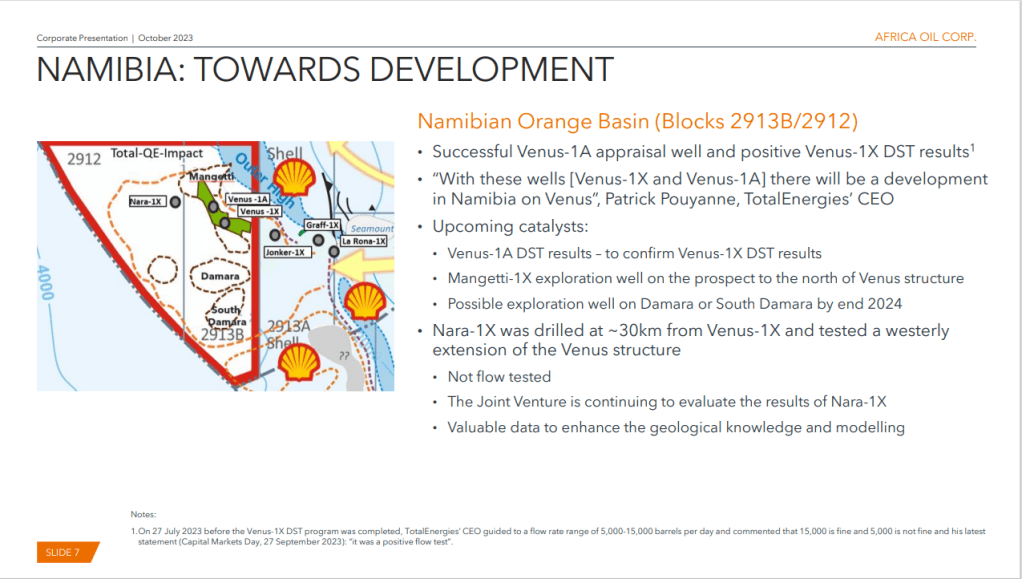

Africa Oil holds a 6.2% indirect stake in the Venus discovery offshore Namibia through its 31% stake in Impact Oil and Gas. The operator of the discovery is Total, which owns a 40% stake (other owners are Qatar (30%), Impact (20%), and Namcor (10%)). Total has mooted Venus as a “Golden Block” and will spend this year more than 50% of its global exploration budget to apprise Venus. Venus is very material for Total and even more material for AOI. The Financial Times reported Venus as the eighth-largest discovery in this century, bigger than Johan Sverdrup, Europe’s largest producing field.

FT article (ft.com)

The other important discovery in the AOI Portfolio is Preowei, which is part of OML130 that AOI owns indirectly through Prime. Preowei deposit may increase production of the OML130 by 50%, which is material for AOI. Just for comparison, AOI’s stake in Venus may contain at least 25 times more oil than AOI’s stake in Preowei.

Significant Development and Exploration Upside

Africa Oil has an additional portfolio of development and exploration assets, split between direct interests and indirect interests through its portfolio companies. The slide below summarizes the opportunities.

ft.com (ft.com)

Another material asset that could drive the share price is Block 11B/12B. AOI owns an indirect 3% stake (through its 30% stake in Africa Energy) in the block, which is also operated by TotalEnergies. Total has applied for a production license that should be issued early next year. Total is also negotiating an off-take agreement with the nearby power plant owned by Eskom. Achieving those targets should drive the AOI stake in Africa Energy materially higher.

Production assets and Venus represent most of the value of Africa Energy. In the next few weeks, the AOI share price will likely be mainly driven by the Venus news flow.

The Opportunity – Share Price Down on Speculation by Retail Investors

During 2023, Total hyped Venus. Total used very strong statements on Venus’s size. See the FT article for an illustration.

The market expected that Total would use its well-advertised Capital Markets Day on 27 September to provide details on Venus’s size. Many retail investors speculated on this through shares of AOI.

The speculation did not work out. Total did not publish any material update on the Venus size on Capital Markets Day.

Total only stated that Venus will proceed to commercialization, and the deposit estimate size is at least 1-2 billion barrels. They also announced that Nara, an adjacent plot to Venus, showed a non-commercial deposit of oil.

Total communication drove AOI share price down by 30%.

This creates the opportunity – the stock was pushed down while strong catalysts on Venus are due by the end of November.

Total is drilling a second well in Venus. The flow data that should reconfirm the Venus size should be published by the end of November. That should re-rate the AOI share price in my view.

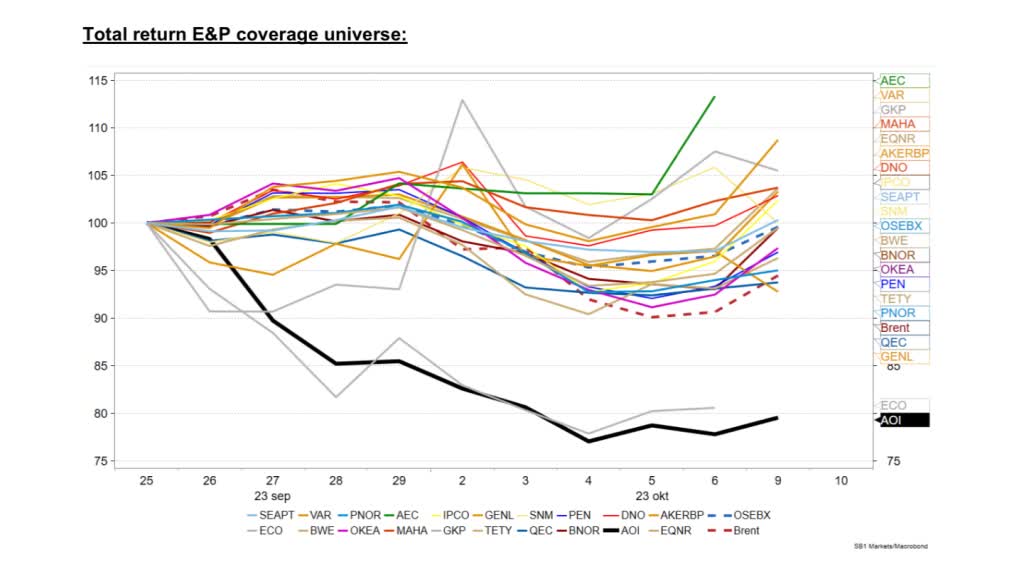

Total’s Capital Markets Day Drove AOI 30% down and made AOI the worst-performing Scandi Oil stock.

sparebank (Sparebank)

Source: Sparebank Research

Why did Total not Publish the Data?

I believe Total’s cheering up the deposit in the press was unusual. Conventional practice is to limit disclosure for deposits set for production in about five years.

There are speculations suggesting that Impact Oil may sell its 20% stake in Venus. AOI holds a 31% stake in Impact Oil.

Total might be an interested party to buy Impact’s stake in Venus.

If they would not buy, they would at least prefer to have a say in who the buyer is in my opinion. Total has, therefore, a low incentive to help prospective buyers be attracted by robust flow data.

Qatar could be an ideal buyer; they are a strategic long-term player. They may be less price-driven. Qatar is mainly working with Total – they are together in Namibia, South Africa, and Guyana.

Venus Massive Field’s Potential

Total declared Venus will be developed.

Total’s conservative estimate places Venus at 1-2 billion barrels. That is a very conservative assessment, according to AOI.

Wood Mackenzie’s report from 3rd October 2023 highlights Venus with a potential of 4.4 billion barrels boe (3 billion oil + 1.4 billion gas), assuming a conservative 30% oil recovery.

The flow data disclosed by the end of November should help to fine-tune the size of the deposits. It will be the major catalyst for the stock.

Further Upside in Adjacent Fields to Venus:

Nara: Found to contain oil, though not at commercial levels. Total contemplates further drilling in the Nara block. Nara still has a promising potential.

Mangetti: Situated above Venus, current drilling results are expected by February 2024.

Damara and South Damara show encouraging seismic results, with drilling planned for 2024.

africaenergy.com (africaenergy.com)

Valuation – Venus and other discoveries are given no value by the market

The recent sell-off brought the current AOI share price to 21 SEK (2.71 CAD). I looked at how Scandinavian broker houses value AOI´s two oil-producing assets:

SpareBank Research values AOI´s two oil-producing assets at 19 SEK

Pareto Securities values AOI´s two oil-producing assets at 17 SEK (assuming USD 70 per bbl, every USD 10 increase in assumed oil price would add 20% to the valuation)

Arctic Securities values the two oil-producing assets at SEK 22 SEK.

In summary, after the sell-off, the AOI is valued approximately at the valuation of its oil-producing assets. All discoveries and all prospective assets are, at the moment, not reflected in Africa Oil’s share price.

The Venus valuation is hard to assess. The valuation is driven by Venus Recoverable volumes and assumed oil price.

To give an indication, Arctic Securities produced a valuation matrix with the above two variables. For example, at Venus’ size of 3 bln barrels and with an assumed oil price of USD 80 per barrel, the AOI’s stake in Venus would be valued at USD 800 million. That is well above the current AOI’s enterprise value of USD 650 million.

Catalysts

Venus’s results will drive the AOI’s share price in the near term.

The second well results, expected by the end of November, might spark a material share price rebound.

The major catalyst would be the sale of an AOI stake in Venus to Qatar or a similar investor. The transaction value is hard to assess but could easily beat the whole AOI Enterprise value in my view.

Africa Oil has a 30% stake in Africa Energy, which is the owner of a 10% stake in Block 11B/12B, a major gas liquids deposit in South Africa. Rumors suggest the operator Total is close to sealing an off-take agreement with Eskom.

Conclusion

Africa oil is down 30% in the last few weeks. In the short term, the share price will most likely be driven by Venus’s news flow. The second well results from Venus should be available by the end of November and should re-rate the stock.

The potential sale of AOI’s stake in Venus would be game-changing for Africa Energy and its shareholders.

Total is spending 50% of its exploration budget this year on Venus. I think Total believes in Venus. Investors should at least study the opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

{kind=link}