We had a call with Africa Energy yesterday. Below are the notes from the call. I think the most important take out for us was that the Production Rights Licence should be issued by South African government by 1Q24. By that time the off-take agreement should be in place. Two major catalysts in the next 9 months.

Financing

Total cash stands at USD 2.7 million (actual at Q1 end)– that is sufficient till the end of the year and may last longer depending on our cost-cutting measures

Annual burn is now below USD 3 million

The company reduced its staff to 3 employees and closed the Cape Town office (4 employees total, including the new CEO), and reduced the size of its board from 6 to 5 members

Financing is not an issue – AEC will take more in loans from our shareholders if needed in 2024.

AEC does not plan to raise capital until the milestones have been reached

Block 11B/12B

The operator, Total, applied for production rights in September 2022. Approval is expected in 12-18 months after submission – early 24. The approval is automatic. There is no delay expected.

It is safe to assume that the offtake agreement will be reached before/when the production rights are granted.

After the offtake agreement – AEC will do the independent assessment

The goal of the AEC is still to sell the 11B/12B after the above is finalized

AEC is also willing to continue with the project if that creates more value – Banks are very favourable to the project, and they are interested in landing projects that reduce the carbon footprint of SA

There are three options for 11B/12B production

Deal with Eskom

Mossel Bay – power plant is burning diesel – owned by Eskomthey have enough diesel, but it is more expensive than gasEskom could save around 30% by burning gasEskom still have no CEO – which is slowing the talks

Deal with Petro SA

Petro SA is the owner of the Block 9 infrastructureAEC will need to use the infrastructure to supply gas to Mossel BayPetro SA owns gas to liquid plant in Mossel Bay, which is out of gas, as Block 9 is depleted – they do need gas

LNG liquefaction plant for export to Europe or Asia

Total/AEC needs a government guarantee for the supplies to either Eskom or Petro SA.

Two ministers are in charge – the new minister for electricity and the minister for energy. The issue is who can make decisions.

SA is now focused on short-term solutions for its electricity crises. Two years is long-term for them now.

Total busy with Venus in Namibia and LNG in Mozambique – 11B/12B is the third priority in Africa

Near-term Catalysts

Gas price agreement finalization – should come during 2023

The resource report by an independent auditor – after the off-take price is known

Sell or stay for development decision

Production Right grant Q1 2024

Our comment:

We are long AEC. The company is very cheap now. It takes much longer than we expected. But it always does. If we would not have our position limit fulfilled, we would be buying here.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Vicore is trading at 1/7 of its peer Pliant, that shows much worse results than Vicore. On Sunday Vicore published their latest IPF readouts in the most important IPF conference in Washington DC. The data reaffirmed “unprecedented regenerative profile of Vicore´s drug in IPF”

On Sunday Vicore Pharma has announced additional data from the AIR Phase II study, which is investigating its lead candidate C21 for the treatment of idiopathic pulmonary fibrosis (IPF). The readout, which was presented yesterday (21 May) at the American Thoracic Society (ATS) international congress, the most important IPF event of the year. On a larger sample of patients (included data on 51 patients treated for up to 36 weeks) Vicore showed progress that has never been seen by any other drug on the market nor in trials.

To illustrate the strength of the results you can read from three research reports:

Pareto securities 21/5/23:

To date, C21 is the only drug that demonstrated a positive trajectory of FVC increases over time….

Considering the potentially life-extending therapeutic profile of the drug coupled with the multibillion-dollar market (the two marketed drugs selling for over USD 4bn per year despite only slowing progression of the disease), we continue to see VICO as grossly undervalued both on a peer basis (e.g. PLRX) as well as on its DCF value

Carnegie Research 22/5/23:

“We therefore argue that Vicore’s research hypothesis holds up, and that the new findings, confirming that C21 could become the first drug to restore the lung function in IPF, validate C21’s truly transformative potential.”

DNB Research 21/5/23:

With more patients and a longer follow-up, the data is more solid than in the past, but basically shows the same thing: treatment with C21 improves lung function over time in patients with IPF. In our view this data and C21 could fundamentally change the way IPF is treated.

Today news on Vicore:

New C21 US patent granted, possibly doubling market exclusivity

Today, Vicore announced that it has been granted a new US patent of the lead candidate C21 for an improved formulation based on enteric coated compositions.

Carl-Johan Dalsgaard, CEO of Vicore comments “This is a very important milestone for Vicore. By prolonging protection in the US to at least 2041, it substantially increases the commercial potential of C21 in IPF beyond current assumptions based on orphan drug status and data protection.”

“We are very pleased that the USPTO has recognized the unique benefits of this technology” saysJohan Raud, CSO of Vicore. “Importantly, the patent provides protection for C21 in all diseases.”

In an interim analysis of the ongoing phase 2a trial, C21 has shown unmatched effects by increasing lung capacity in patients with IPF, a devastating disease which untreated results in a steady decline in lung capacity and a typical life expectancy of three to five years after diagnosis. C21 acts by preventing the scarring process characteristic of IPF, thereby restoring alveolar integrity and improving lung function.

“In IPF alone,the potential value of this critical patent is material considering that the US IPF market represents $2.8 bn in annual sales, despite the limitations of current therapies”, saysCarl-Johan Dalsgaard.

Vicore Pharma is very undervalued. We are very bullish on Vicore.

For the whole investment thesis please see previous blog post:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Summary of the Scandinavian opportunities we saw in the market last week.

Short Rec Silicon– Capital Raise this week?

All analysts indicate that Rec Silicon needs to raise capital.

Usually, companies do investor roadshows before they raise capital. Rec Silicon did their roadshow from 11/5 till 15/5. Last week was a short holiday week in Norway. Capital raise may come this week.

In good markets, I would expect a capital raise at a discount of at least 10% to current share price. In these markets, discount might be much bigger – could easily be 20%. We are short Rec Silicon – hope to buy it back after the capital raise at a much cheaper price.

The short-term trading idea is supported by the oversupply in the silicon market predicted for this year by both analysts and as well as the company (see their Q1 webcast)

Pyrum Q1 Update

In our view this is most promising company that is involved in chemical recycling of tires. They are most advanced, I am not aware of other tire recycling company that would be running a continues recycling operation for three years without interruption. For example Scandinavian Enviro systems (Ticker SES), has a batch process – you do one batch, cool the system, clean it and reheat. They cannot be efficient nor competitive vs Pyrum

Pyrum´s new line 2 and 3 should start operating in July 2023. The company plans to invite local politicians and TV crews on the occasion. Last time they did that the share price doubled.

The company has announced they will start construction of their third plant in Homburg this year. The company announced the funding for the plant is secured and they will provide details in the next weeks.

Pareto has a price target of 780 NOK, almost double from the current share price.

Calliditas reported last week sales below consensus. As a result share price was down by 30%. We have increased our position by 50% on the weakness.

Slow Q1 sales but positive signs lead to a stronger Q2 – According to the company, the weak Q1 sales were a result of low enrollments in January, partly due to many patients changing their insurance plans. However, March reported a record number of 408 newly enrolled patients (+30% from Q4), indicating the further growth of sales. On average it takes one month to convert enrollment into sales. Q2 sales should be very strong.

The company has no real competitor in the market. The sales are expected to accelerate every quarter.

The approval in China is expected in H2 2023 with a milestone payment. In China IgA Nephropathy is much more common disease than in western world where Calliditas is starting to sell now. China approval could be a material game changer.

Pareto has a fair value target of SEK 463 per share – 450% upside from current share price of SEK 100.

Redeye Research has Calliditas as one of its 14 Top Picks. Their Bull price target is SEK 485, and base case is SEK 310.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Seeking Alpha published the below article 5 days ago. Since than Pliant is down 27%.

According to Pareto analyst Dan Akschuti:

Vicore seems to be the game-changing drug for IPF. It is the first IPF drug that turns a deadly disease into a survivable one.

VIcore has much stronger results than Pliant does. Despite that Pliant traded at 12 times higher valuation that Vicore. We might be seeing reverasal. Pliant is down 27% in last week. Vicore up should be next. Due to the rotation and due to very strong catalyst in next three weeks for Vicore.

Our family office is long Vicore.

We publish the whole SeekingAlpha article below:

Pliant Therapeutics: Bad Risk Reward, Buy Vicore Pharma Instead

Apr. 26, 2023

Summary

Pliant Therapeutics is a USD 1.8 bn US based clinical-stage bio-pharmaceutical company developing new treatments for idiopathic pulmonary fibrosis (IPF).

Pliant reminds us of Belgian biotech Galapagos N.V., which first posted promising (at first glance) 12-week data but later had to terminate the program, losing over USD 3 bn in market capitalization.

There are serious questions every investor should ask Pliant.

Vicore Pharma has one IPF product and is at similar stage as Pliant. Vicore is trading at a 12 times lower valuation while having significantly stronger data than Pliant.

We are short Pliant and long Vicore.

everythingpossible

Pliant Therapeutics (NASDAQ:PLRX) is a US-based USD 1.8 billion market capitalization clinical-stage biopharmaceutical company developing new treatments for idiopathic pulmonary fibrosis (IPF) diseases.

IPF is a complex disease, and few available treatments for fibrosis exist today. Pliant indicates that its groundbreaking treatment may be game-changing. That is what´s behind its USD 1.8 billion market capitalization.

“Be strategic when disclosing data” quote could be taken in several ways. In my view, it is quite a strange quote from a pharma CEO. We believe it may be very symbolic for Pliant´s data readout.

Pareto Securities, a leading Scandinavian broker, Published on 17 March 2023 an analysis of Pliant’s latest readout. The quote below, in my view, may well represent the whole research piece:

The data looks positive at first glance as the placebo group looks to perform worse than treatment groups. However, having looked a bit closer at it, we conclude that Pliant’s 12-week data is inconclusive and with that we see a significant risk going forward….

What may be wrong with Pliant?

There may be three issues with Pliant´s data:

Inconsistent results across dosage

Irregularities in Pliant´s placebo population

Decline in the effectiveness of the 320 mg lead dose

Inconsistent results across dosage

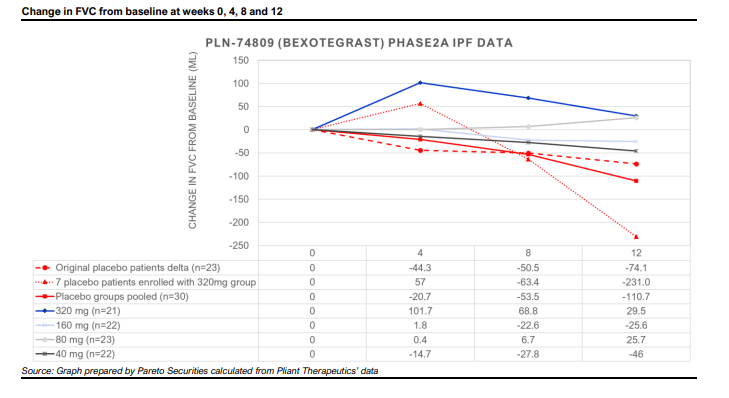

A key indicator if a drug is active or not is an assessment of its response to a dose increase. Generally, a higher dose should lead to a stronger effect until a plateau is reached (often capped due to toxicity). In Pliant´s case, there seems to be no dose response at the 12-week ending values:

Pliant compares the results of its medication with the results of its placebo clients. Pliant´s sample of placebo clients is not really placebo – 80% of the placebo clients were treated on Standard of Care (treatment that is accepted by medical experts as a proper treatment for a certain type of disease and that is widely used by healthcare professionals).

There are three completed studies on drugs on the market. These studies used real placebo (wholly untreated clients) comparisons. As 80% of Pliant´s placebo clients were treated on Standard of Care, Pliant´s placebo sample clients should show a smaller deterioration than placebo clients from the three samples.

My understanding of Pliant´s placebo clients shows the opposite. Pliant´s placebo clients seemed to decline at a rate around four times as fast as that of 1600 wholly untreated patients (from three completed studies of drugs on the market). If that understanding is right, then it is quite a worrying sign.

Data of the 320 mg lead dose

The 12-week study shows a strong positive effect in weeks 0-4, which is followed by a decline in weeks 4-12. The decline is the same as with the placebo clients indicating that the drug works only in weeks 0-4 and then is the same as the placebo.

I enclose a graph from the Pareto research that illustrates the above.

Source: Graph prepared by Pareto securities calculated from Pliant Therapeutics´ data

Unconvincing response from the company

I sent the issues raised in the Pareto research and summarized above to the company. The key part of their response was:

(this is) … mistake made by many other investors and analysts in trying to think about this as a linear calculation when backing out the placebos. As you may recall, this was a Mixed Models for Repeated Measures (MMRM) analysis that we implemented. In addition, they did not remove the outlier that appeared in the 40mg cohort (as part of the July 2022 dataset) that was identified as part of the placebo pool in conjunction with the 320mg data announcement and subsequently removed….

I wrote back asking for a detailed response to each of the points I summarize above. I got no reply to that.

Even if you accept that “the placebo decline is similar to what Boehringer Ingelheim saw in their trial”, due to Pliant´s use of Mixed Models for Repeated Measures and due to removing of outliers, you still have the issues of inconsistent results across the dosages and the positive effect of the drug only in the first four weeks with subsequent declines in line with placebo. The company did not provide any response to these points.

The above issues were covered in the Pareto research. I would have expected the company to be ready to address each of the points. I was surprised they did not. I tried twice.

I want to stress that the data may be too inconclusive to conclude that the drug is not actually doing something good. 12 weeks might simply be too short. I just note that the above are issues that concern me. And they should concern other investors too.

The Pliant share price has been rising sharply despite rumours of another capital raise. In my view, there is a significant downside risk in the stock price.

At the same time, these situations are hard to short. The pliant share price has positive momentum. We are short Pliant through long maturity deep out-of-the-money put options. Our position is small.

Introduction to Vicore Pharma

Vicore Pharma (STO:VICO) is a Sweden-based and Stockholm stock exchange-listed company with a market capitalization of 1.6 billion SEK ($160 million)

Pliant and Vicore are both focused on one IPF drug, and both are in a broadly similar stage of testing. In my view, Vicore Pharma has much stronger results. Despite that, Pliant is trading at a 12 times higher valuation than Pliant.

Vicore Pharma released the latest test results in November 2022:

At 36 weeks of treatment with C21, shows an FVC increase (+633).

The company provided the below illustration of the results:

Illustaraion (DNB Research)

I understand no other drug has shown a profile like this in IPF.

Do compare the Vicore and Pliant graphs. The difference is significant. While in Pliant´s case, you see a positive result for the first four weeks followed by a decline. In Vicore’s case, you see a stabilization already in week 6. After week 18, you see a material improvement in lung function.

Vicore seems to be the game-changing drug for IPF. It is the first IPF drug that turns a deadly disease into a survivable one.

As mentioned above, Pliant´s trading at 12 times higher valuation vs a drug with much stronger results does not make sense.

Vicore shares trade in Stockholm. Investors can buy through brokers or online trading platforms. For example, Interactive brokers allows trading in Vicore.

Vicore valuation

There are two analyst covering Vicore:

Pareto securities has a price target of 97 SEK per share, and

DNB has a price target of 98 SEK per share.

Both price targets represent a 5x multiple vs the current share price of 20 SEK.

In my view, the upside may be very significant. There are two drugs on the market which sold more than USD 3.5 billion in 2021. Both drugs have incomparable results in comparison with Vicore. The USD 3.5 billion price tag represents a 35x multiple from the current share price.

If the readouts continue to produce such strong results, Vicore will be taken over by a major. The only question is how high of a price compared to the current price. Our target for Vicore is to make at least a 100% return.

It makes no sense that Vicore would trade at 1/12 of Pliant. The main reason is Vicore is listed in Sweden and off the radar screens of most investors. This may change soon – see below.

What is next – catalysts

Both companies will present the next readout during 2Q23.

Pliant’s next 24-week readout is expected within Q2 2023.

Vicore issued a press release that they will announce the next phase readout at the American Thoracic Society International Congress on May 21st in Washington, DC. This is a very bullish indicator for the stock. This is the biggest and most important event for the IPF. The fact that Vicore chose to announce the results there indicates that they are very bullish on the readout. You would not want to publish results in the most important event unless you have high confidence you can impress the industry. This is a very bullish indicator for Vicore. Not only does it give us confidence in the next readout, but it will also put Vicore on the screens of US investors. It could be a game-changing event for Vicore.

Conclusion

We believe there is a material downside risk for Pliant. The next readout may clarify the above issues. Or it may not. Given this uncertainty, its USD 1.8 billion valuation seems just too high to justify.

Vicore seems to be the game-changing drug for IPF. It is the first IPF drug that turns a deadly disease into a survivable one. The fact it is off the radar screens of US investors creates a great opportunity. The May 21 presentation at the most important IPF event could be a game-changing moment for Vicore.

We are short Pliant through options and long Vicore.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

IN February, 2023 EU imposed sanction on Russian oil products (diesel, etc). That meant that EU will have import diesel from 3-7 times longer distances than when supplied by Russia. It means the product tanker rates will go up and therefore Product tanker equities should benefit.

This is happening with some time lag – the EU build up supplies from Russia before February. Now the inventories are steadily falling – and product tankers equities are starting to gain traction. We are long HAfnia.

The risk of the trade – if oil goes down, it would drag tankers with it, despite the profits they are making. The recent OPEC cut indicates, that OPEC cares about the oil price, which reduces risk of the oil price fall.

Summary from Pareto Research published today:

Product Tankers: Another leg up is imminent

While product tanker rates in 2023 are only marginally ahead of our estimates – we remain encouraged by the longer distances for Russian cargoes. With so far still a modest order-response we continue to find the shares extremely attractive – with fleet growth going to slow down further into 2024.

We thus raise our forecast for 2024 and are now 25 – 35% above consensus for the next two years – and expect positive revisions soon. BUY reiterated across the board – with target prices raised once again.

Strong start to the year Though volatility remains, product tanker rates have had a strong start to 2023, following the euphoric fourth quarter of 2022. Year-to-date, LR2s and MRs have averaged USD 53,000 and USD 38,000 (both eco ships) respectively, slightly ahead of our estimates.

Russian barrels now travelling longer distances Since the sanctions against Russian product exports came into force in early February, we have seen a sharp rise in total oil products ‘in transit’, meaning that distances are increasing. Northwest Europe has yet to fully replace the ~0.75mbd of Russian products it imported in 2022 and is now seeing inventories slowly but steadily fall.

So far only a small supply-response While the ordering pace has picked up for LR2s and MRs, orderbooks remain at decade-low levels. Shipyard prices are elevated, and delivery dates pushed out in time – and we will next year see a 10:1 relationship between the number of vessels above 15 and the number of vessels on order.

Raising estimates and expect consensus to do the same Encouraged by the positive start to the year, increased Russian distances – and limited supply response, we raise our 2024 TCE rate estimates by 10 – 20%. This results in EPS-changes of ~33% – and puts us ~25-35% ahead of consensus for both Scorpio and Hafnia. We find HAFNI-estimates particularly low and expect significant revisions in conjunction with the Q1 report – as Q2 guidance is going to be materially above current expectations.

Still see ~50% upside in Hafnia and Scorpio We continue to use a 1Y-forward NAV approach, adjusting fleet values for ageing and including forecasted cashflow. Both HAFNI and TORM are trading at 20%+ yields for 2023 and 2024. We currently have HAFNI/STNG at ~0.85x NAV and see those NAVs growing by 25 – 30% through Q2’24. Sub 4x EV/EBITDA with rapidly falling LTVs (already below 30%) we struggle to see better value elsewhere, and thus reiterate BUY across the board. Hafnia, TP from NOK 80 to NOK 87.

I recommend to review on post on Norsk Titanium from yesterday.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

We try to publish interesting ideas worth to look at and analyze further.

Norsk Titanium (Oslo listed: NTI) is a US based and Norway listed company which has developed a proprietary disruptive technology which can produce titanium-parts for about 55-70% lower cost than incumbents.

The first plant is built in the US and is now certified by Airbus and others. The company is already producing for Airbus, ASML (the largest producer of chip making machines) and others.

Airbus is now certifying the plant for production of safety critical aircraft parts, where margins are very strong. The company in its presentation (see below) indicated the first Airbus critical parts order is expected in 2Q23. The order would serve as a proof for investors. When received, the share price should react very strongly.

The company raised around 10 mln USD recently and should be well funded until the Airbus certification.

Note from Carnegie analysts

Norsk Titanium

Invested: $400m

Mcap: $90m

Debt: zero

Cash: $5m

Burn: $1,8m/month

Cash need to fully funded: $50m

Norsk Titanium is an innovative Norwegian company which has developed a proprietary disruptive technology which can produce titanium-parts for about 55-70% lower cost than incumbents.

Norsk Titanium was started in 2007, one of the founders was Alf Bjørseth (REC, Scatec Solar).

From its start and up until today around USD340m has been invested in the company. Norsk Titanium has received USD125mill in grants from the NY state, which has financed both all their machines and the production facility, which is the largest 3D printing facility in the world.

Norsk Titanium is not ‘another metal 3D printing company’. NT’s technology called Rapid Plasma Deposition(RPD), uses a plasma torch to melt a titanium wire and thus builds the products ‘drop-by-drop’. This is different to traditional 3D metal printing, which basically is ordinary printing done over and over and over again. Norsk Titanium’s products have 100% ‘forging-quality’ (extremely important, since they will produce critical structural parts), while 3D metal printing have not. Thus Norsk Titanium will not be in competition with the 3D metal printing companies.

Titanium is a metal that is extremely suitable for ‘high-value applications’ since it is strong and relative light. It is a life-or-death’ metal within the aerospace industry and has bean around in that industry at lease since 1950.Norsk Titanium has until now used their resources in R&D and run numerous testing and qualification programs and is the only 3D (or more precisely Additive Manufacturing) company that has been qualified by FAA (Federal Aviation Association) for production of structural titanium parts for the commercial aircrafts. Structural parts are typically parts that carries weight – that part that ties the engines to the wing, parts that tie the different airwing sections to each other and also tie the wings to the body of the aircraft. Unsurprisingly there are long and extensive quality and qualification prosesses ahead of any serial orders.

The total addressable market (TAM) for NT’s titanium parts is around USD150bn with the aerospace around 13bn – that is based on the final product. Since Norsk Titanium produce ‘near-shape parts’, the relevant numbers for Norsk Titanium is half of the TAM.

Since an ever increasing share of the aircraft is composite materials, the share of titanium will almost automatically also increase since titanium does nor corrodes with composites (which other materials may do). The current aircrafts fleet contains around 7% titanium on average, while Dreamliner (which use a lot of composites) for instance contains 15% titanium

Norsk Titanium’s competitors are the traditional forging companies (the incumbents) – ATI, Howmet (both listed), Albert & Duval and Otto Fuchs to name a few.

In general titanium metal is expensive. When producing a final product the incumbents use around 12x as much titanium metal than the end product. Similar numbers for Norsk Titanium is around 3-4x. This is the lower(dark) section in the chart below. In order to produce a finished product, the incumbents need to heat the metal, forge, press, use a die to form it, press it again, forge, press, use another die, forge, press, etc etc. This process is typically repeated 7-10 times and equals the machining cost in the chart. As you see this cost is typically far higher than the pure raw material cost. Norsk Titanium costs to create the product is more or less the same as its raw material cost. This is the light color (the RPD cost) in the middle of the Norsk Titanium bar. After production, Norsk Titanium sells its ‘near-shape product’ to its customer which further shaves off excess metal and process it further. That machining cost is shown on top of the Norsk Titanium bar. I stress that this cost is not a cost for Norsk Titanium, but I stack all costs in the RPD process to compare overall costs between a typical incumbent and costs based on Norsk Titanium technology.

Norsk Titanium’s business idea is to sell their products to its customers equal to incumbents RAW MATERIAL COSTS. Since the titanium cost per aircraft is high – and increasing – Boeing and Airbus are screaming for lower titanium costs. With Norsk Titanium’s disruptive technology, costs can be reduces by 55-70%. By switching to Norsk Titanium, both its customers and the end customer will save costs and thus improve profitability. The end game is probably that the major share of the structural parts in the titanium market somewhere in the future is made from similar (right now Norsk Titanium is the only player) technology.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

ON Sunday, Spare bank published the following note on Africa Energy:

Africa Energy – Total’s 11B/12B negotiations with slow progress, market discount a delay

Total, the operator of block 11B/12B in South Africa where Africa Energy holds a 10% stake, has over the past quarters negotiated with electricity producers Eskom (fully owned by the South African Government) for an offtake agreement. However, negotiations have been slow and Total has indicated other solutions may be evaluated. Africa Intelligence recently wrote there are “Two other options on the table” and that “If negotiations do not work out with either of them, TotalEnergies still plans to participate in a FLNG facility in South African waters and focus on exporting gas abroad”. As far as we interpret the situation, an LNG export solution is more likely now than before (but probably not base case). One year later first gas from 11B/12B cuts our SOTP valuation by SEK ~0.40/share.

Summary of SpareBank research dated 30/3/23

Africa Energy (Buy, tp SEK 3.0) – Market discounts delay for 11B/12B and only USD 1.2/boe fair value

Q4 financials roughly as expected: Africa Energy reported Q4 22 recurring net income of USD -1.1m, slightly better than our forecast of USD -1.5m. Net cash of USD 1.8m was below our forecast of USD 3.2m, mainly driven by increased payables. Overall, Q4 financials were roughly as expected in our view.

Some funding needed soon: While the company’s cash burn at low activity level is minimal, we see some funding requirement over the next few quarters (if not assets are divested). We note that the company has established a USD 5m credit facility with its three largest shareholders: Africa Oil, Deepkloof Limited and the Lundin Group. The maturity date of this facility is January 31, 2024 and accrue interest at a 10% annual interest rate if repaid by October 31, 2023 or 15% annual interest rate if repaid after October 31, 2023.

Total’s 11B/12B negotiations with slow progress, market discount a delay: Total, the operator of block 11B/12B in South Africa where Africa Energy holds a 10% stake, has over the past quarters negotiated with electricity producers Eskom (fully owned by the South African Government) for an offtake agreement. However, negotiations have been slow and Total has indicated other solutions may be evaluated. Africa Intelligence recently wrote there are “Two other options on the table” and that “If negotiations do not work out with either of them, TotalEnergies still plans to participate in a FLNG facility in South African waters and focus on exporting gas abroad”. As far as we interpret the situation, an LNG export solution is more likely now than before (but probably not base case). One year later first gas from 11B/12B cuts our SOTP valuation by SEK ~0.40/share. Our full SOTP valuation stands at SEK 6.3/share while our core NAV is SEK 3.3/share. Since the announcement of the dry Gazania well, which is unrelatrf to the 11B/12B development, the share price is down SEK 0.5, which implies that market over the past few months implicitly has assumed 1.2 years delay for 11B/12B compared to the implied assumption as of late 2022. At the current share price (SEK 1.2/share) the marked values 11B/12B discovered wounded at USD 1.5/boe vs. our assessment of USD 4.3/boe. That assessment assumes zero net cash and no value assigned to other assets. We rate African Energy Buy with a SEK 3/share target price. Our target price corresponds to P/NAV of ~0.6x

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

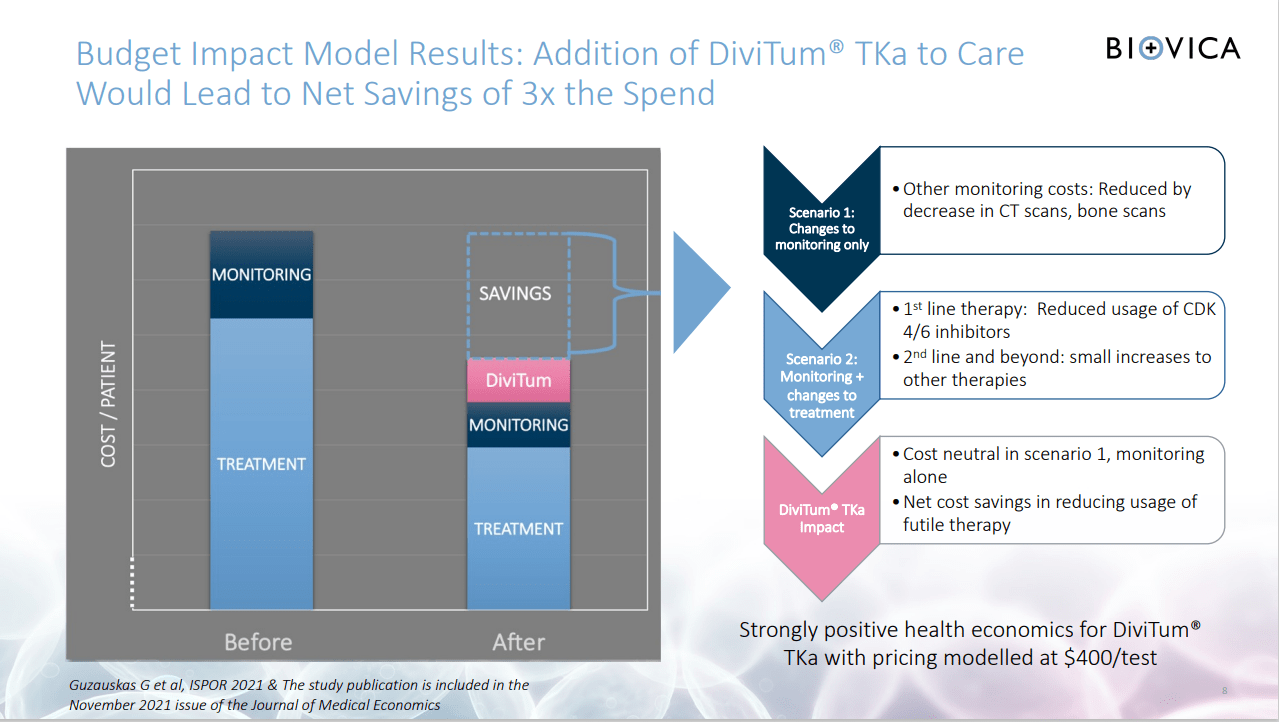

In cancer treatment – the speed of cancer monitoring drives survival. Biovica breast cancer test can quickly detect if the selected medication is working or not.

Biovica biomarker breast cancer test can detect cancer progression at least 60 days earlier than imaging. And 3-10 times cheaper.

Bloomberg just reported “Biomarkers are Dramatically Changing Cancer treatment”. Biovica was the first-ever FDA-approved Biomarker test for cancer. It has the potential to be one of the market leaders.

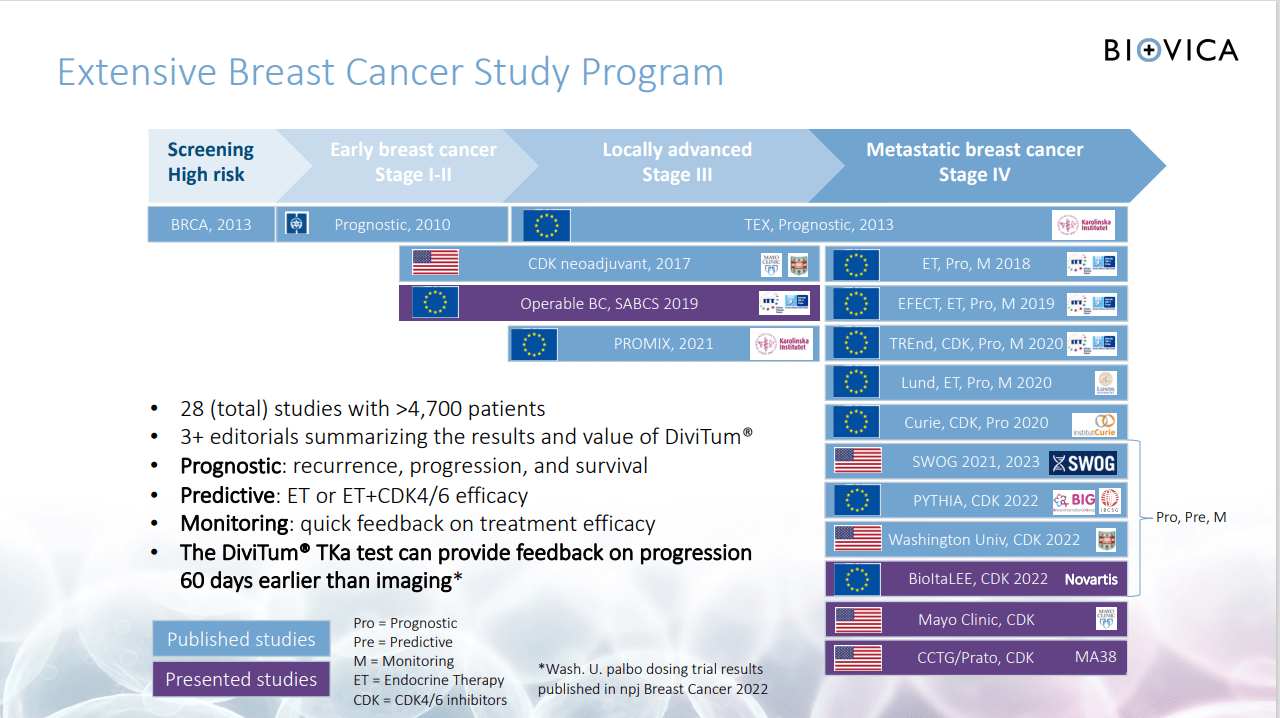

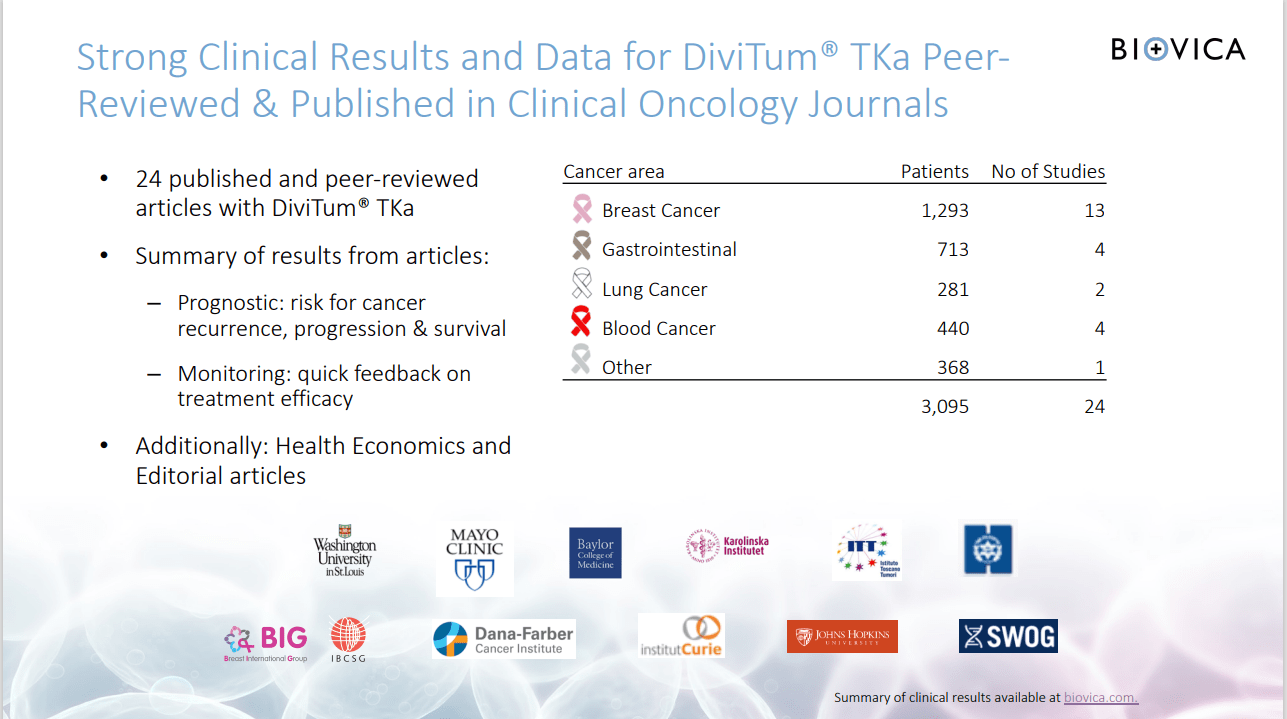

Very strong clinical data – 28 studies including from the most prominent US hospitals (Mayo Clinic, John Hopkins, the Dana-Farber Cancer Institute).

Market potential > $2 billion for monitoring of metastatic cancer.

bymuratdeniz/E+ via Getty Images

Introduction to Biovica International

Biovica International (STO:BIOVIC.B) is a biotech company with a laboratory, production facility, head office in Uppsala, Sweden and a laboratory in San Diego, US.

Biovica has the first FDA approved cancer biomarker test that can detect Breast Cancer progression at least 60 days earlier and 3-10 times cheaper than currently used imaging procedures.

Biomarkers are changing the way cancer is treated. Biovica´s biomarker test has the potential to become the leading force in disrupting and changing the way the cancer is tested and treated today.

The test is a result of 35 years of research at Uppsala University, the most prominent university in Sweden.

Biovica has a primary listing in Stockholm with SEk400 million (USD40 million) market capitalization. The company has 2022 year end projected net cash position of SEK 133 million (USD 13 million).

Management owns 15% of the company. The CEO invested SEK 10 million in the recent SEK148 million capital raise (USD 1 million) in cash, which I understand is a very material amount given his net worth. You do not often see the CEO of a company this size investing such a material cash amount. It is a strong rubber stamp of confidence in the project. The incentives of management are therefore aligned with the other shareholders.

Bloomberg: Biomarkers are Dramatically Changing Cancer Treatment

The article talks in length about how biomarker testing is changing the way cancer is treated and predicts a very bright future for Biomarker:

The use of biomarkers in cancer treatment has changed the course of treatment dramatically. For decades, many cancers were treated in the same way: with surgery, radiation therapy, or chemotherapy. The identification of biomarkers in cancer cells has resulted in the development of novel precision medicine treatments, such as targeted therapy and immunotherapy, which are designed to target specific traits in cancer cells while causing minimal harm to healthy cells.

The FDA Approval

At the end of July 2022, the Company received 510(K) clearance from the FDA in the US for DiviTum TKa as a tool for monitoring disease progression in post-menopausal women with hormone receptor positive metastatic breast cancer. FDA recommended monthly testing of cancer progression.

Biovica

The topline conclusion from DiviTum’s clinical data within MBC is that it can predict whether a patient is not progressing within the coming 30 days (treatment is working) with 96.7% accuracy and the coming 60 days with 93.5% accuracy. This indicates that frequent testing allows for a sort of “live monitoring” of what the cancer is doing. That this is not common is supported by the fact that it isthe first such blood-based biomarker approved by the FDA.

The Opportunity – Covid Delayed the FDA Approval Driving the Share Price Lower

Biovica’s market capitalization is down 80% from its peak of SEK2 billion in August 2021 to the current SEK400 million now.

Market capitalization Graph

Market Capitalization Graph (Tradingview.com)

Pareto Securities issued detailed research on Biovica dated 10 February 2023. Their summary of the share price decrease:

… the company has been simply unlucky…. By no fault of its own, the flood of COVID-19 diagnostics has stalled Biovica’s submission for over 1.5 years, causing a continuous decline in the share price. With the FDA approval finally obtained in July 2022, the market conditions dictated a strong discount for autumn 2022’s rights issue while causing a 37.5% dilution – beating the share price down to the current low levels…

Biovica Has A Market Disruptive Product

Biovica’s biomarker test has the potential to disrupt and change the way breast cancer is tested today. Breast cancer is the most common cancer form – there is a big market for the product, treatments are very expensive, fast detention can increase survival and the test is much cheaper than currently used methods.

Breast Cancer – the Most Common Cancer Form

Breast cancer is the most common form of cancer among women around the world.

An estimated 450,000 patients in the EU and the US are living with metastatic breast cancer, and breast cancer is responsible for more than 40,000 deaths each year solely in the US.

These deaths are due to the disease spreading through the body and affecting critical organs. The cancer is generally incurable if it has metastasised, but recent new treatments have increased the quality of life and lengthened the time a patient can live with metastatic breast cancer.

The number of available treatments has also increased. Metastatic breast cancer is a chronic disease that requires lifelong treatment, approximately 29 percent of patients live longer than five years.

Breast Cancer Treatment is Very Expensive

Approximately 80 percent of all breast cancer patients have hormone receptor-positive cancer. The leading suppliers of CDK4/6 inhibitors are Pfizer with Ibrance, Novartis with Kisqali and Eli Lilly with Verzenio.

In 2020, sales for these three CDK4/6 inhibitors were estimated by Research Nester to amount to approximately USD 7 billion

Frequent Cancer Progression Testing is Vital

There is a significant need for being able to evaluate the effect of treatment more easily and quickly. Additionally, many cancer treatments involve serious side effects which should only be accepted if monitoring verifies that the treatment is effective.

Current Diagnostic Procedures are Expensive and Results Take a Long Time

A number of tests and methods are run repeatedly and regularly to assess how the disease is progressing.

In most instances, a single test will not provide a definitive answer, which is why many different tests are run repeatedly.

Current diagnostic procedures are expensive, complex and require time for monitoring and imaging that exposes the patient to radiation, injections with tracing etc., which is sub-optimal for the health care system and stressful for patients. External advisors and oncologists suggest that a blood-based test such as DiviTum TKa could be used on a monthly basis early on during treatment, and every three months thereafter.

Biovica’s DiviTum TKa can detect cancer progression 60 days earlier than imaging.

The DiviTum Cancer Test

Cancer diagnostics is a strongly evolving field. DiviTum is an innovative test developed with the aim to evaluate cancer progress. The test measures the activity of the enzyme Thymidine Kinase-1 (“TK”) in blood serum or cell cultures. In normal cells, TK activity is hardly detectable, but in cancer-affected cells, its levels increase. Since the degree of TK activity is highly associated with the rate of cell proliferation, it is a particularly suitable biomarker for researching tumor aggressiveness.

DiviTum offers several advantages over alternative testing:

Rapid Evaluation – DiviTum proved that it can detect if a patient is responding to a treatment or not already after 14 days. The current techniques require 3-4 months.

Cost savings on treatments – DiviTum proved that it can quickly recognize if the current cancer treatment is working. The cancer treatments are very expensive. The DiviTum would reduce the use of treatments that are not benefiting the patient.

Costs savings on testing – MRI testing price ranges between USD 300-3500, PET Scan costs USD 1250 – 9200. The analysts expect the DiviTum would cost USD 300 – 750. That is significantly below competing tests.

Easily obtainable samples for testing – samples can be obtained from patients in any laboratory.

Biovica

Strong Scientific Backing

The Company has published 13 scientific articles from clinical breast cancer studies that encompass over 4,700 breast cancer patients, and a total of 28 clinical studies.

Biovica International

These studies have documented the ability of DiviTum TKa to measure cell proliferation as well as its utility as a prognostic tool for patient survival and as a monitor of treatment efficacy in patients with breast cancer.

No Real Competition

Pareto Analyst Dan Akshuti wrote in his initiation research on Biovica:

“With the exceptions of AroCell and DiaSorin, we have not found any companies that have clinically evaluated their products. All of the companies observed sell their products for research use only. Costs for the kits vary enormously (e.g. USD 2,030 for Eagle Biosciences’ kit and USD 703 for Abcam’s kit), and due to non-clinically validated regulatory approval in any kind of indication, we do not consider the kits as competitors to DiviTum.”

US Product Launch in 1Q23, European Launch in 2Q23

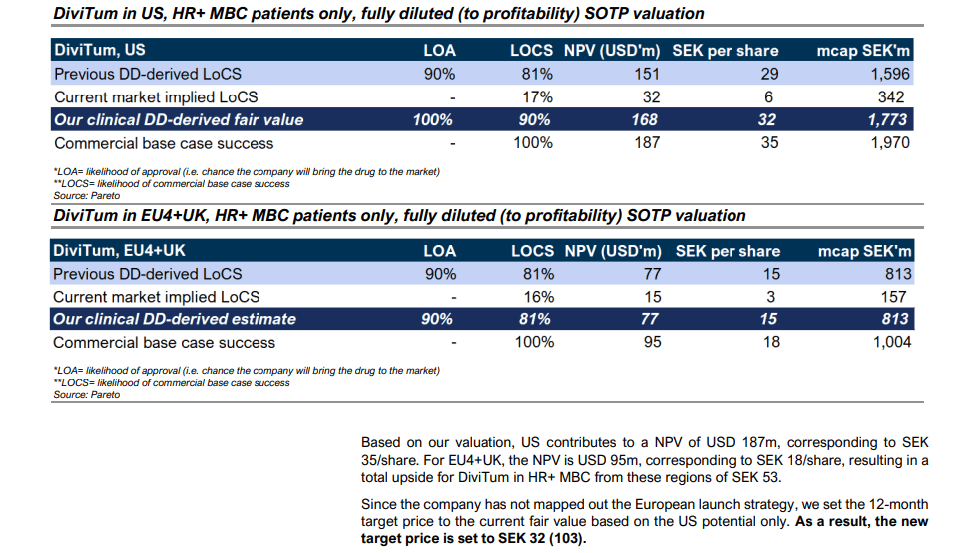

The Company is launching DiviTum TKa in the US market during the first quarter of 2023.

In Europe, the product holds IVD-D approval and will be launched in selected markets during the second quarter of 2023 through strong partnerships with major industrial players.

The middle management sales team consist of six US regional directors with a combined 128 years of medical sales experience.

Strong Revenue Potential

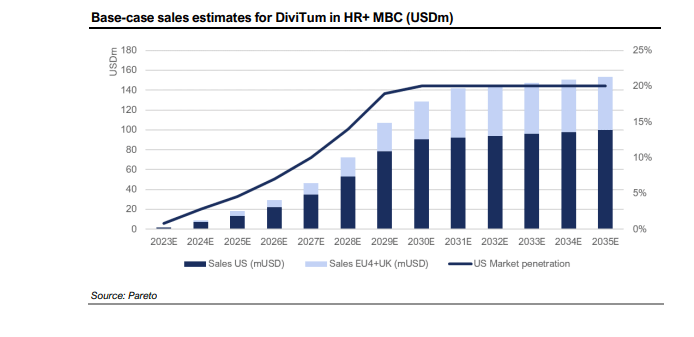

The prices per DiviTum test are estimated by the Pareto analyst at USD 450 in the US and USD 250 in EU4+UK. Assuming seven tests a year per patient, they assume an annual US price of USD 3,150 and USD 1,750 in Europe. Peak market penetration is assumed to be 20% in the US and 19% in EU4+UK.

Pareto states:

“The peak penetration is likely underestimated considering the simplicity of the test. We will adjust this as with other values upwards as soon as we can see that the launch curve is steeper than ours… We were very conservative this time and there is a good chance that the company will beat our estimates.”

Pareto Securities has a price target of SEK 32 (fair value now, only US, excluding EU and UK) and SEK 53 (fair value US, EU and UK), and

Redeye has a base case price target of SEK 95. The price target was issued before the latest capital raise, that diluted the shareholders by 37.5%. Although Redeye must have assumed the capital raise, for conservative purposes I adjust their price target for the dilution, which results in adjusted price target of SEK 69.

Even the lowest base case of SEK 32 represents a potential return of ~250% from the current share price.

Pareto valuation summary:

Pareto Securities

In my view Pareto is very conservative. Before the FDA delay, Biovica was their favorite biopharma pick. As Covid delayed the approval, the share price was sliding and Pareto investors lost money. That is the reason Pareto is now quite conservative. They also openly say this – see the quote above.

Pareto has two base case valuations – SEK 35 (US only), and SEK 53 (US+EU+UK).

Pareto in their base case takes into account only the US market, because “the company has not mapped out the European launch strategy” (see above). I understand from the call with management that took place after the research was published that the company plans to enter the European market through partnership with major European players. Further I understand that Biovica is engaged in discussion with several partners and that first such agreement may be announced already in 1Q23. When this happens, I believe the base price target of SEK 53 should become more relevant.

Another indication of the value potential is to look at the market valuation in 2021 before the FDA approval, when investors believed the approval was in sight. At that time Biovica was trading at a USD200 million market capitalization, five times higher than the current market capitalization of USD40 million.

The share price development will depend on how quickly the company is able to announce strong partnerships, and generate sales. There are two positives that speak in Biovica’s favor:

High concentration of breast cancer care – 10% of cancer centers represent 50% of all breast cancer treatment costs,

Biovica has strong ties to the most prominent US hospitals, as many have already done client studies with DiviTum.

The company discloses many near term catalysts in their prospectus, that should help to gradually increase investor confidence in the story.

My base case is, that Biovica should reach the Pareto “lower” price target of SEK 35 this year and should well exceed its pre-FDA peak valuation next year. That would mean above 400% return within two years.

Risks

The main risks include adverse macro conditions that could result in an overall market sell-off, delays in new partnerships, delays in the product acceptance by the cancer centers, slower sales growth, bad market communication (overpromise and underdeliver), higher cash burn during the launch, higher dilution during the capital raise and general management mistakes.

Near Term Catalysts

There are many catalysts listed in the 2022 prospectus. I have adjusted the dates based on my discussions with the management:

• Launch of DiviTum TKa in the US – announcement of the first sales – 1Q23

• Announcement of the first partnerships for European market – 1Q23

• Announcement of the first commercial agreements with major US hospitals – 1Q23

• Application for the PLA code with Medicare – 1Q23

• Launch in the first European markets through partners – first sales 2Q23

• First sales through major US hospitals – 2Q23

• Obtaining the PLA code with Medicare – 2Q23

• At least one local agreement for Medicare – 2Q23

Not Priced In

Biovica is working on biomarkers for other cancer forms. The analysts do not talk about those in their recent research – their valuations are based only on the breast cancer biomarker test. As the breast cancer revenues start to increase, the analysts will start taking into their valuations the global potential related to the testing of other cancer forms.

At some point Biovica will likely become a takeover target for a global industry player.

Biovica International

How can US Based Investors Buy

I have bought part of my position on Interactive Brokers. The ticker is BIOVIC.B in SFB market. I believe you can buy through other online platforms too.

Materials for Further Analysis

There are very useful materials on Biovica’s IR site. Do look at the prospectus, presentations and the long recording from the investor day, that introduces the investment case in detail. I would also register for Biovica alerts on their web site and follow Biovica on Facebook, where they announce more details on their progress.

Conclusion

Cancer diagnostics is a strongly evolving field. Biomarkers are changing the way cancer is treated. Biovica has the first FDA approved biomarker cancer test and therefore is in line to become one of the market leaders in biomarker cancer testing.

Biovica cancer test can save lives by delivering results around 60 days earlier and 3-10 times cheaper than the current methods. The timely diagnoses if the selected cancer medication is working or not can materially decrease medications costs.

Biovica has a potential to disrupt the way cancer progress is tested. This would benefit the patients, the insurers and Biovica shareholders.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. This article expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

FT Reported “Risk growing of Russia weaponizing its metal exports” – some ideas how to trade this

Mintra – extraordinary cash distribution of 32% of its market cap signals takeover may by coming. Takeover premiums in Scandinavia ranged 50%-120%

Linkfire up 250% in last 10 days, but still 80% down from its IPO price

Biovica – last year biggest looser, this year biggest winner

Russia War Trades – Palladium Trade

FT reported today:

Citigroup has warned clients about the risks of Russia weaponizing its exports of materials such as aluminium, palladium and nuclear fuels, potentially leading to price rises for these critical commodities….

Russia produces about a quarter of the world’s palladium, which is used in catalytic converters in vehicles, and exports most of what it produces.

We like most the palladium trade, as Russia has the biggest share of the metals. We bought Sibanye StillWater Ltd SBSW. The company has mining and processing operations. It is primary producer of platinium, palladium, rhodium and gold. When the war started the stock traded around USD20, as market was worried Russia would cut supplies of metals. The worries since disappeared and the stock trades at USD8, a two year low. Downside might be limited, unless there is a global sell off. Upside could be 150% if the stock would return to levels when the war started. Idea for further research by investors.

Mintra – The extraordinary dividend may be funding for the takeover

Mintra declared 1.75 NOK capital disctibution, which represents 32% of its market capitalization.

Mintra structured the dividend as a return of capital. Return of capital is tax-free, the dividend is not.

Mintra does not have enough cash; they need to borrow for this. I was trying to figure out why they would do it. The share price would react more favorably to a declaration of regular dividends at an annually sustainable amount. The share price did not respond to the extraordinary dividend announcement.

The capital distribution have the following implications:

Mintra’s share price decreased by that amount to 3.6 NOK

Investors will get an extraordinary dividend equal to 50% of the adjusted share price

If one wants to take over MIntra – it is an ideal situation – it reduces the Mintra share price significantly + Mintra itself provides tax-free cash (see below) for the takeover

Both analysts that cover Mintra believe that Mintra will be taken over by its two major shareholders, who control over 40% of Mintra. The extraordinary dividend is a smart corporate finance exercise that indicates that the takeover may be coming soon

Pareto analyst estimates, that takeover premiums in the last 12 months were around 50%-120%. This is the possible upside, if the takeover really materialises.

Linkfire up 250% in last 10 days, but still 80% down from its IPO price

since we wrote here about LInkfire, the stock has more than doubled. LInkfire reported best quarter ever for a second time in a row. Please see my previous post here on Linkfire. We are very bullish.

Biovica – last year biggest looser, this year biggest winner?

SeekingAlpha published a detailed article on Biovica on Monday. It is very appealing story.

Bloomberg published article that Biomarkers are changing the way cancer is treated (link below)

Biovica has the first ever FDA approved Biomarker test – for breast cancer. Biovica is one of global leaders in the booming field.

Quite detailed analysis of Biovica investment case published on Seeking Alpha, the largest investment idea site in the world.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Linkfire delivered the best quarter in its history, beating previous best quarter 3Q22.

Revenues grew by 72%. The growth was driven also by the new partnerships with Apple Music and Amazon Music

Gross margin of 79% – the highest ever

The CEO of Band Lab became 4th largest shareholder in Linkfire. Band Lab is the largest a online Cloud Digital Audio Workstation tool for creating music with over 60 million users, including professionals like Dr. Dre or Jay-Z.

Profitability is the main goal for 2023. With the current cost base, the revenues need to grow only by 22% to reach profitability. Last quarter growth exceeded 70%.

After partnering with Amazon Music and Apple Music, new majors partnerships should be announced in 2023.

Linkfire dominates smart links for music industry. We expect the company will enter into podcasts in Q1/Q2 to dominate the podcasts as well.

We have bought material stake in Linkfire in the last few months and we should be among the largest investors now.

We think the biggest opportunity for this year would be to look for solid companies, whose share price was beaten up severely last year. Linkfire is the best example of such investment case. Solid company, dominating its industry, no competition, 70% growth…

Linkfire is 90% down from its post IPO peak

Linkfire market capitalization is down from 1.4 bln SEK to 130 million SEK. The drop was mainly caused by market dislike for growth companies + Linkfire refinancing in worst possible time last year. Last year biggest mkt cap looser this year winner may fit well for LInkfire.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.