We enclose our top ideas for Q3. I wrote her before about many of those and include links to the investment rationale.

Biovica – FDA approved first biomarker test in cancer area

On Monday Biovica reported FDA approval for its unique breast cancer test. The stock went up only by 30%. The current market cap is only around 80 million USD. Very low for the first biomarker test in cancer area. There are plenty catalysts shortly. Strong takeover candidate. See the links for details.

Mintra – high beta play on shipping and energy exploration growth.

Mintra reported best Q in Q1. Pareto believes Q2 should be even better. Q2 is due on 11/8. Mintra is profitable, growing strongly, healthy cash flow generation, no debt and it is still one of the cheapest vs Scandinavian peers.Doubling candidate for this year.

Russia war against Ukraine results in gas shortage. EU wants to buy gas from elsewhere. LNG tankers should be the beneficiary. Cool Company was recently listed in Norway, US listing is due in 2H22. Should appreciate strongly this year.

A global leader in servicing streaming companies. +70% market share, +70% gross margin, 50-70% revenue growth. Top 10 IPO from Denmark. Unjustifiably punished by the growth stock sell off.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

We have been very bullish on Biovica. I wrote here several times about the opportunity, I published articles on SumZero and SeekingAlpha. We viewed the likelihood of the FDA approval for its Breast Cancer Test as over 90%. Market gave it much lower probability, the not patient retail sold the stock. Over the weekend Biovica announced the FDA appoved its product. Today the stock should re-rate materially. The major catalysts have materialized.

I believe there is a material re-rating in the coming weeks as well. The company will be announcing plenty of newsflow:

– Biovica will immediately start discussing with insurance companies on reimbursement. – there should be increased price targets by brokers in the next days – there should be first sales in the US through its partner hospitals – there should be announcements about next cancer type FDA application timeline – they have several studies on other cancer forms. – there should be announcement on EU sales strategy – Biovica is now the leading company in this area. They could become takeover target later in the year

Pareto Securities Comment:

DiviTum gets FDA approved as first ever biomarker in its field

Over the weekend, Biovica finally received US approval from the FDA for its diagnostic test. The approval was delayed over a year due to FDA’s prioritization of COVID-19 diagnostics and DiviTum specific questions. DiviTum is the first biomarker that has been cleared by the FDA for treatment monitoring (seeing disease progression or treatment response early) in hormone receptor positive, metastatic postmenopausal female breast cancer patients. The company has already set up a US organization and is now able to launch the product before end of this year. This is Biovica’s biggest achievement yet and we believe the stock should trade up more than 50% over the coming days or weeks. We have a Buy rating on BIOVIC with a target price of SEK 103/share.

Redeye research on Biovica published this morning:

Biovoca FDA Approval: A late qualifier for a pole position

2022-08-01

Johan Unnerus

Finally, Biovica has secured US approval (510k) for DiviTum in the core market indication. The approval is to use DiviTum to aid in monitoring disease progression in previously diagnosed hormone receptor-positive, metastatic postmenopausal female breast cancer mBC. The company is now a Dx (broad sense) with an approved clinical marker on the US market.

The approval is excellent news. Even if widely expected, the approval finally came a bit earlier than expected. DiviTum is now the first FDA 510 (k) approved blood-based TKa marker, which is part of why the FDA process has been taking that long, in addition to the direct and indirect COVID effects.

Apart from this exclusive position (hence our reference to a pole position), the approval is based on the SWOG (SO226) study. The clinical outcome where DiviTum shows the ability to confirm non-progression of mBC with a very high negative predictive value, NPV, of 96.7% for non-progression within 30 days and 93.5% for non-progression within 60 days. The ability to confirm non-progression when using CDK 4/6i (at a price above USD 10k per month) in this patient cohort based on a blood sample (timed with existing planned patient visits) is clinically, ethically and economically very useful.

DiviTum’s NPV is significantly above the ctDNA (also blood-based) test. When using DiviTum mBC, patients can also reduce the use of imaging during the CDK4/6i therapy as long as DiviTum confirms non-progression, especially as earlier studies have confirmed DiviTum’s ability to deliver a result almost two months earlier than imaging.

Later in August, we expect Biovica to update and confirm the go-to-market plan announced during the CMD earlier this year. Should we expect sales already during 2022, and when can we expect to break even? We expect a launch with some sales already in 2022.

We also expect Biovica to initiate the process of expanding the label, where the first step could be to advance the BC space into advanced (regional) BC. This label expansion is a natural step as DiviTum has already secured clinical support in this space. It is also rational for DiviTum to follow the CDK4/6i therapy progression, expanding into this space where both Pfizer and Novartis are market leaders with a proven interest in DiviTum.

A second wave could include using DiviTum in other cancer indications and potentially confirming non-progression among already successfully treated patients.

Our value proposition is a base case value of SEK 95 (Bull SEK 325, Bear SEK 20). This approval increases the probability of approval from >95% to 100%, but market expectations have probably been significantly below 95% due to the delayed approval. Biovica is initially committed to initiating the US launch as an independent company without a strategic partner. We can expect Bivica to:

Step up the initiative to secure a CLIA certification for Biovica’s Sand Diego lab (covering most of the US market).

The first sales wave is probably to have the initial objective of expanding the network of interested cancer hospitals and centers, mainly in the US coastal region. The sales process could take some six to nine months to establish recurring volume sales. At this stage, investors should look out for an indication of the run rate of CDK 4/6 patients treated in this expanded network, in our view. At the first wave’s later stage, we expect Bivica to secure early recurring sales.

In the second sales wave, we can expect Biovica to expand the in-house sales team and the commercial reimbursement cover and US guideline support. The prospects of including DiviTum in the US guidelines will be an opportunity later in 2023/24. If turned into reality, we can expect a step change in the usage and the commercial cover.

Biovica has already secured pharma interest and collaborations well ahead of plans, including seven agreements with large and mid-sized pharma at this stage. With the FDA approval, we can expect this interest to intensify to a higher level.

These commercial processes will require growth capital. Having secured the FDA approval, we expect Biovica to secure growth capital, allowing the company to reach cash break even with a good margin whilst also allowing Biovica to progress with market activities in both US and Europe and expand the FDA label probably already during 2023.

At this stage, we do not change our Base case value proposition (SEK 95) as the approval is balanced by some uncertainty regarding the details of the approaching fundraising for obvious reasons. We look forward to the update of the go-to-market plan later in August and the subsequent launch.

We can expect a highly significant positive market reaction on the back of the FDA approval, and even a 50-100% increase would leave plenty of upside to our SEK 95 base case. The current market value of USD <90m for a company with FDA approval is hugely undemanding. Our Bull case (SEK 325) reflects the value proposition with support from an expanded label and support from strategic industrial partners. First thing first.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

We have been very bullish on Cool since the war started, I wrote here several times about the company. Thesis is simple. Europe is braking relience on Russian gas and will need to get gas from more remote places. By LNG tankers. Cool company should be one of the beneficients. Spot rates are booming, Cool stock has not move, yet. It is a newly listed stock. Dual listing in the US announced for H2.

ABG Sundal Collier published very bullish report. Front page summary below:

Recent weakness in spot rates carry little impactABGSC slightly below cons for Q2’22e, above for ’23-24eTP up to NOK 179 (154) on a stronger USD

Recent weakness in spot rates carry little impact The Freeport incident on 8 June, and the following loss of LNG cargoes, has lowered spot rates for 160k TFDE ships such as those owned by Cool Company, but we also note that the 174k MEGI spot rates have increased for two consecutive weeks now. However, declines in spot rates in recent weeks should have a minimal impact for Cool Company given its extensive contract coverage for this year. As we adjust the 1-year TC contract fixed at USD 120,000/day earlier this year to start in May (previously assumed to start in June), we increase our Q2’22 EBITDA by USD 1m, to USD 33m. We have also added a dividend payout already from the coming quarter of USD 0.1/sh based on a cautious 25% pay-out ratio.

ABGSC slightly below cons. for Q2’22e, above for ’23-24e Although we add USD 1m to our Q2’22e EBITDA, we are still 4% below FactSet consensus, while our market rate assumptions for H2 are above consensus and for the full year our USD 151m EBITDA is 12% above consensus. For ‘23e and ‘24e our EBITDA is USD 256m and USD 274m, respectively, reflecting our positive stance on the continued strength in the LNG shipping market, with average spot rates above USD100,000/day in both years, and we are 81% and 137% above consensus, respectively.

TP up to NOK 179 on a stronger USD The continued appreciation of the USD/NOK adds NOK 28/sh to our 1y fwd. NAV of NOK 199/sh, to which we apply a 10% discount to arrive at our target price of NOK 179/sh, up from NOK 154/sh. We estimate a current P/NAV of 0.77x and regard Cool Company the most attractive exposure to what we continue to believe will be a very interesting LNG shipping market in the years to come. We reiterate BUY.

Do read our previous blog post on Mintra, one of the beneficiaries of the shipping boom. Very interesting company

Disclosure: The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

Mintra – going up even in current turmoil, reporting best quarters in Mintra´s history, strong cash generation, high cash balance, no debt, AND still the cheapest among Nordic peers. My base case is double share price this year.

Summary

Product and LNG tankers have the best year in decades. Energy exploration is booming. Mintra is a high beta play on these sectors.

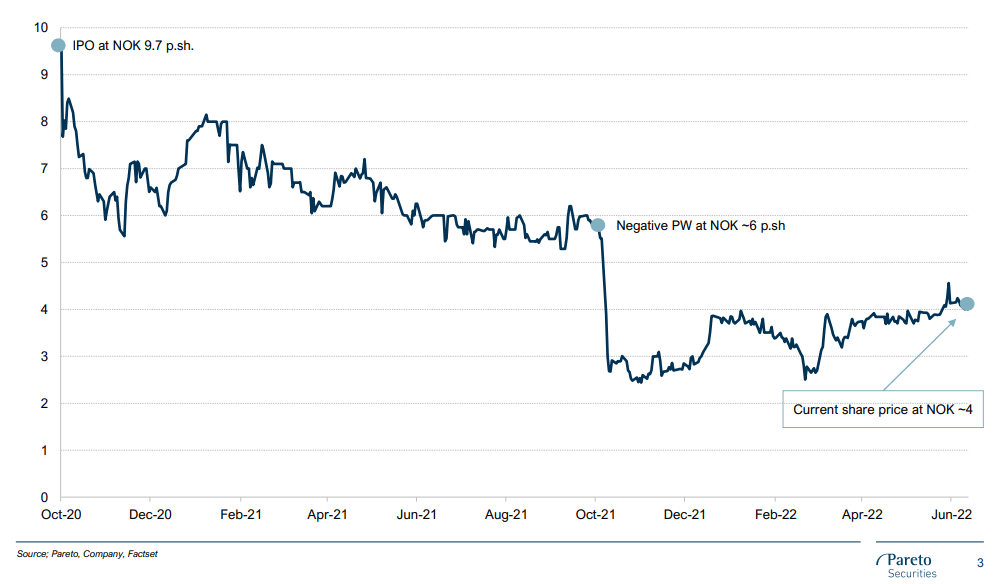

Mintra was hammered during COVID. It is in recovery mode – up 70% from its lows this year, but still 60% down from its IPO in October 2020.

Mintra is still one of the cheapest vs Scandinavian peers.

Product and LNG tankers may not double this year. Mintra should.

Introduction to Mintra

Mintra Holding (MNTR.OL) is a Norway based parent company of several operating entities from Norway, the United Kingdom and Singapore. The company provides on-demand digital learning training and certification courses for safety critical industries worldwide. Mintra is listed in Norway on Euronext Growth. The stock can be traded on Interactive Brokers as well as other trading platforms.

The Mintra team consists of over 140 designers, developers, industry consultants, and supporting functions working to the highest standards.

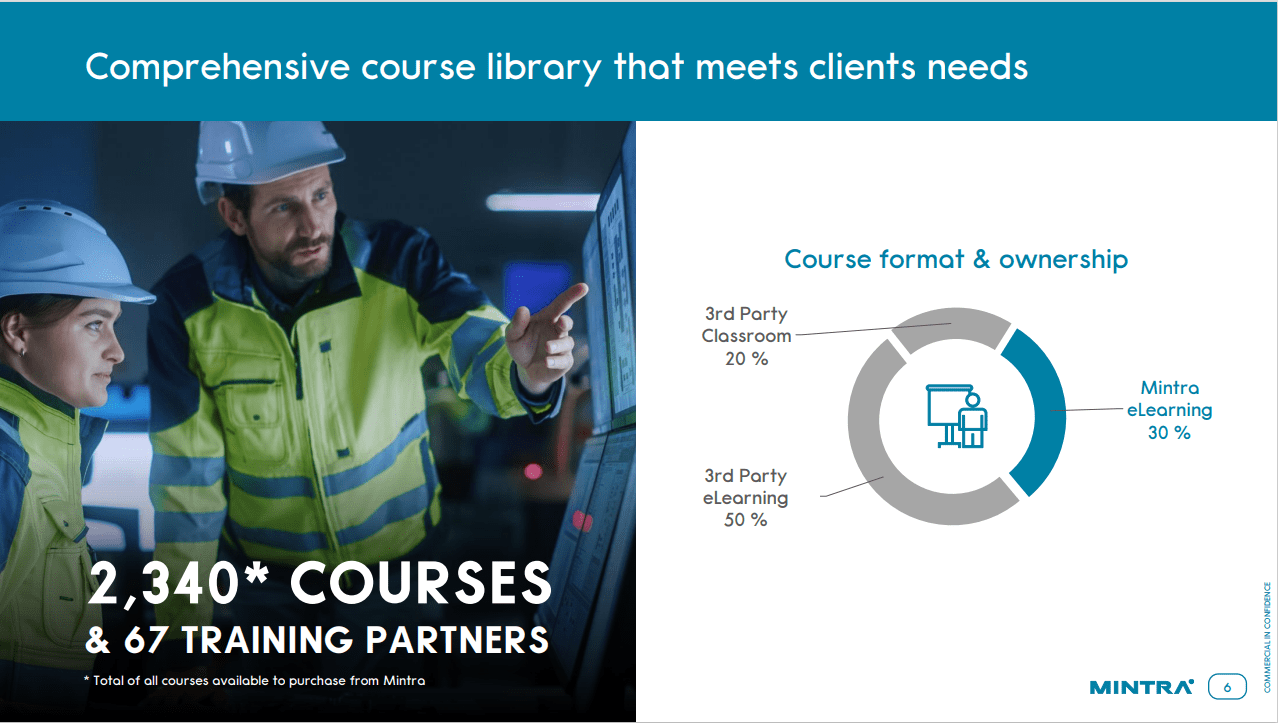

Mintra currently provides 2340 courses mainly for safety critical industries worldwide. 30% of courses are from Mintra library, the remainder is from its 67 eLearning partners.

Introduction to Mintra (Mintra)

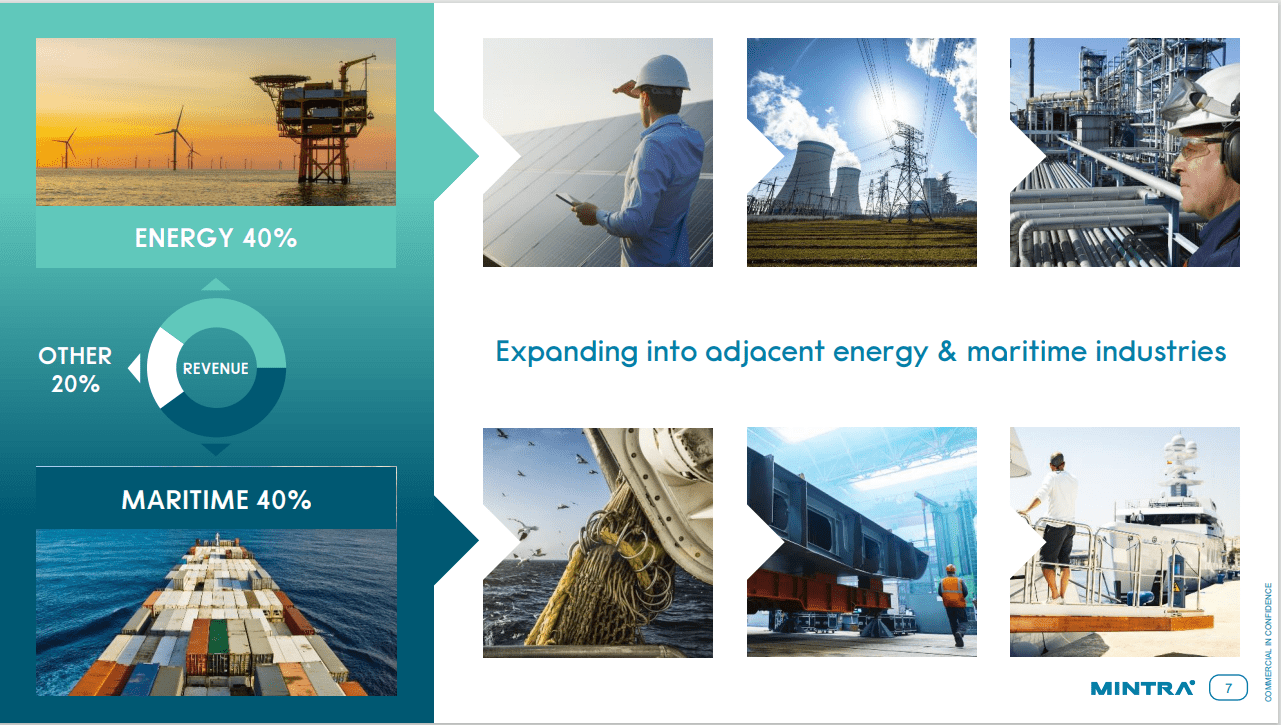

Training courses to Maritime and Energy crews represent 80% of Mintra business. Mintra is therefore highly correlated with Gas and Oil markets as well as with the Maritime industry.

Source: Mintra (Mintra)

Mintra was a COVID victim

Mintra business is heavily dependent on frequency of rotation of maritime and shipping crews. Low degree of crew rotation during COVID meant low need for crew certifications and therefore lower need for crew courses.

… continuing inability of ship operators to conduct crew changes has been the single greatest operation challenge confronting the global shipping industry since the Second World War…

ICS Shipping on the crew change crises during Covid

The significant decrease in crew rotations led to revenue and profitability declines, resulting in share underperformance since the IPO.

Source: Pareto Securities (pareto)

Mintra – great way to play the Shipping and Energy Boom

2022 is the year of Shipping and Energy. Product tankers and LNG tankers are flying up due to the Russian war on Ukraine. Container ships are rising higher on supply chain congestion. Oil and Gas markets have been booming. Rig operators are announcing the best rates in a decade. But mainly, all the Mintra clients are making a lot of money. Crews are rotating, so there is an increased need for Mintra training courses and online certifications. Mintra is the beneficiary of the shipping and energy turnaround.

Mintra’s 1Q22 was its best quarter ever, 2Q22 should be even better

The turnaround in shipping and energy is already showing in Mintra’s numbers. 1Q22 was Mintra’s best quarter ever – Mintra generated a 10% FCF yield in the quarter. That is 40% annualized FCF! They can generate CF equal to their market capitalization in 2.5 years. 2Q22 will most likely be even better.

Broker consensus still assumes only 10% growth for 2022

Last year Mintra guided 10% revenue growth for 2022. That was well before the energy and shipping growth started. The guidance was not revised yet. It could happen during the Q2 report. We could easily see doubling of the growth guidance.

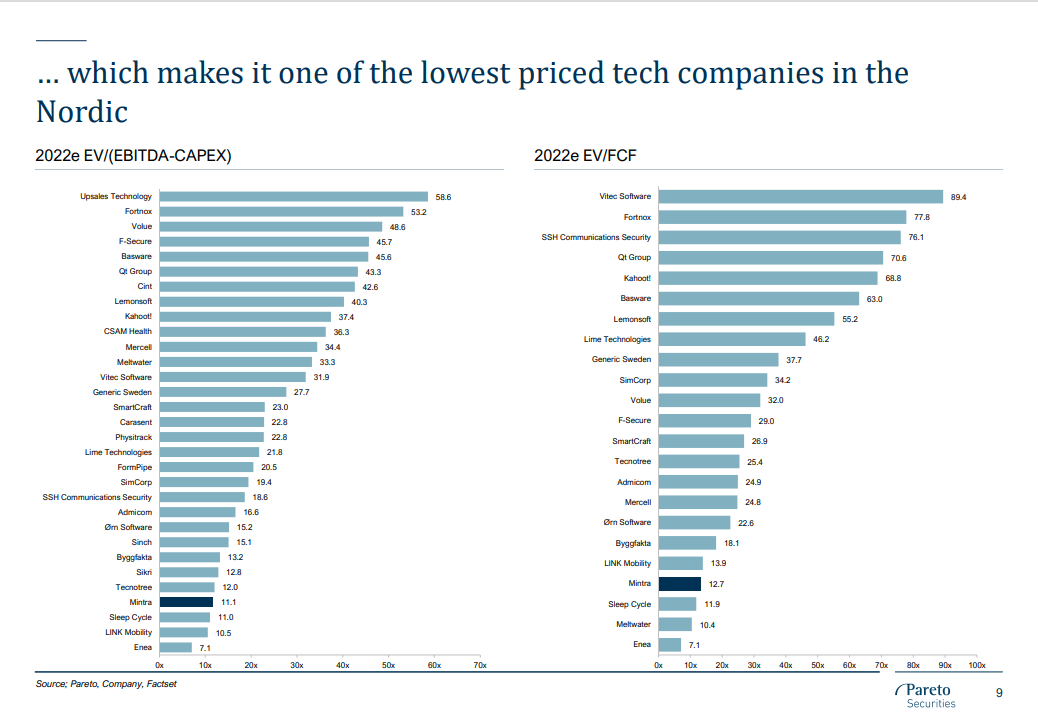

Mintra is still one of the cheapest Nordic tech companies despite being up 70% since March lows

As the share price graph above shows, Mintra is up 70% in three months. But it is still 60% below its 2020 IPO price of 9.7 NOK per share. Despite the strong share price performance this quarter, Mintra is still one of the cheapest tech stocks in the Nordics according to Pareto Securities.

Source: Pareto Securities (Pareto)

Mintra is net cash positive, has a strong balance sheet and healthy margins

As of the end of Q1, Mintra has a net cash position of 110 million NOK (cash balance has exceeded its small leverage). Based on the 2022 guidance, Mintra should be generating 28% EBITDA margins and 13% EBIT margins.

Mintra should at least double this year

Our base case is for Mintra to double this year. That would bring Mintra from the current 4 NOK to about 8 NOK, still well below its IPO price of 9.7 NOK. In this scenario, Mintra would remain one of the cheapest tech stocks in the Nordics.

Catalysts

The main catalyst is the Q2 report scheduled for 11 August 2022. The Q2 report should be the best quarter the company ever reported. In addition, the Q2 report may include new full-year guidance.

Conclusion

2022 should be the year of Energy and Shipping. Mintra should be the beneficiary of the boom. Mintra has a strong balance sheet, no debt, and strong cash generation. In the current environment, Mintra should generate cash equal to its capitalization in under three years. Mintra is still one of its peers’ cheapest stocks while reporting the best quarterly results ever. It’s a good opportunity to buy a good company cheaply.

Go to SeekingAlpha to see the full article

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

We have been very bullish on Pyrum Innovations, the most advanced company involved in chemical recycling of tires. Today Pyrum made two announcements:

Announcing a recycling cooperation with Schwalbe

Pyrum has announced a cooperation with the Ralf Bohle GmbH, who considers itself to be the European market leader for bicycle tires with its iconic brand “Schwalbe”.

Under this agreement, Schwalbe has established a recycling network for used bicycle tires with all participating Schwalbe dealers. These used bicycle tires will then be delivered and fed into the pyrolysis process at Pyrums plant in Dillingen, we understand.

Pyrum adds Schwalbe as another well-reputed name to an already impressive list of cooperating partners (BASF, Conti, Michelin)

First joint venture established – third plant construction announced During the IPO, Pyrum indicated it is negotiating several JVs for construction of additional tire recycling plants.

Pyrum has announced to establish the first joint venture to build and operate a pyrolysis plant with a (standard) capacity of 20,000 tons of used tyres.

The location of the plant, which will be operated under the name “REVALIT GmbH”, will be in Straubing near the Danube in Bavaria. Besides Pyrum, the shareholders of REVALIT GmbH will be the Munich-based companies MCapital GmbH, TEXTOR GmbH and Auer Holding GmbH, each with 25%

Pyrum is our top position, together with Quantafuel in the chemical recycling space. There is a lot going on for both companies. Pyrum should have a lot of newsflow in H2 in connection with commissioning of their second plant in Dillingen.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

AEC is our top conviction plays in Energy. Pareto Securities is fully on board. Below is a summary of their latest research. The stock should double in next months.

Pareto research Summary:

Stars aligning & Significant news flow ahead

Africa Energy is down yoy (vs peers up >50%) despite commodity prices advancing, which we believe is caused by lack of news flow. This will change imminently driven by drilling of the Gazania prospect (SEK 2.5-3.0/share potential if successful) and upcoming catalysts on the development of the vast discovered resources at Block 11B/12B. In addition, we think the market has overlooked the increased strategic value of Africa Energy’s portfolio as energy security and gas exposure (increasingly seen as an enabler for energy transition) are becoming key themes in the industry. We think the stock can double over the next months and reiterate BUY/TP SEK 4.50.Drilling at Block 2B expected to commence in early September

We expect the rig move for the Gazania-1 well (27-5% WI) to be announced shortly with drilling start in early September and results 25-30 days thereafter. The well is fully carried by the partners (Eco Atlantic (operator), Panoro and Crown Energy) and has a unrisked potential of >300 mill boe gross of oil. We estimate a value potential of SEK 2.5-3.0/share net to Africa Energy based on a long-term oil price of USD 70/bbl. The well will be drilled up-dip from the A-J1 discovery, which reduces risk compared to most exploration wells in frontier areas. Another positive is that also a fairly small discovery can be commercial (threshold around 50 mill bbl) due to a benign operating environment and favorable fiscal terms.

Production Right application by Sept’22 & Gas sales agreement approaching Operator Total is progressing the development of the large gas discoveries (>1bn boe) on Black 11B/12B (10% WI). The Phase 1 development will benefit from existing infrastructure and supply existing customers in the Mossel Bay area. This is expected to enable first gas already in 2025 with a production of 50-55,000 boe/day (35-40% liquids) gross. We estimate a project IRR of 25-30% based on a capex assumption of USD 2-3bn and a gas price of USD 6/mmbtu, which implies significant upside if commodity prices remain at current levels (contract will likely have an oil price link). The next step is submission of the Production Right application that we expect will occur by the latest in early Sept’22 and be a positive trigger for Africa Energy. Ahead of this, the partners also aim to secure a gas sales agreement that if realized will materially derisk the project. While difficult to forecast the timing of this important milestone, increased focus on energy security (domestic production vs imports), environment benefits (replace coal) and current highcommodity prices (make the contracted price look low) all provide incentives to move the project forward for the South African government, in our opinion.

Attractive risk/reward – BUY/TP SEK 4.50 reiterated We estimate Africa Energy’s NAV at SEK 5.5/share based on a long-term Brent price of USD 70/bbl and a gas price of USD 6/mcf for the Block 11B/12B development. With the cash balance and existing discoveries valued at SEK 2.7/share (vs current share price SEK 2.05), we find the risk/reward to be attractive ahead of the upcoming catalysts that over the next months have potential to increase the value of its key asset and add another discovery to Africa Energy’s portfolio. While Total is exactly the type of company preferred to operate the Block 11B/12B development, the near-term drawback is limited news flow as majors typically only report progress upon major milestones. This have impacted Africa Energy’s share price over the last year (down 8% measured in USD) and create an attractive opportunity to buy in ahead of the news flow ahead. We reiterate our TP of SEK 4.50 and see upside potential to above SEK 7.0/share if the Gazania-1 exploration well is a success (SEK 0.5/share downside to our NAV if unsuccessful). Africa Energy is financed for the upcoming catalysts with limited near-term spending but will upon progress at the Block 11B/12B development require external capital in 2023/24, in our estimates. The key risks to our positive view are unsuccessful exploration activities and delays in the development of Block 11B/12B.

SMC Research, a specialist for the analysis of German small- and mid-caps, has rated the Pyrum Innovations AG share for the first time. In the conclusion of the research report published today, the analyst sees “a fair value of EUR 88.00 per share and thus significant upside potential” despite a safety discount on the Company’s long-term plans regarding capacity expansion.

Since 30 September 2021, Pyrum Innovations AG has been listed on the Euronext Growth Market, the growth segment for small and medium-sized enterprises of the Oslo Stock Exchange. Since 30 March 2022, there has also been a secondary listing in the Scale Segment, the SME growth market of Deutsche Börse AG. In addition to SMC’s new research, the research report of Edison Investment Research Limited is also available on the company’s website.

As a pioneer, Pyrum Innovations AG was the first company in the end-of-life-tyre recycling sector to receive REACH registration from the European Chemicals Agency (ECHA) for the pyrolysis oil it produces. This means that the oil is recognised as an official raw material that can be used in production processes. In addition, Pyrum has received ISCC PLUS certification for the pyrolysis oil and the recovered carbon black. Both products are thus considered sustainable and renewable raw materials. These achievements have also been recognised by international experts in the tyre industry. For example, Pyrum won the Best Tyre Recycling Innovation category at the inaugural Recircle Awards and has been nominated for the “Grand Prix Mittelstand” (“Großer Preis des Mittelstandes”) from the German state of Saarland.

Biovica had their road show presentations for Pareto clients this week. The company reconfirmed that it is in an active talks with FDA which they believe should conclude with the FDA approval by Q3. Our base case (based on discussion with analysts) is June/July. Biovica is meanwhile preparing for the US sales lunch. The impressive US sales team was presented at their Investor Day presentation.

Best Biovica CEO quotes from the presentation yesterday:

“FDA is developing really well… We are confident to get our FDA clearance in Q3….. The last time we communicated with the FDA was last Friday…”

Updated timeline for sales start FDA decision expected in Q3, potential sales start in Q4 DiviTum shown complimentary to ctDNA Q4’21/22 EBIT of SEK -19m, cash position of SEK 90m

Updated sales start The main news from the report was the timeline and path forward for approval and sales start of DiviTum. The revised 510(k) filing was submitted on 28 April and Biovica has received an indication that the FDA has started to review it. The normal review time is 90 days: Biovica expects a decision during calendar Q3, which will either be a clearance or a request for more information. Simultaneously it is establishing the CLIA lab where the facility is in place (evident in the higher right-of-use liability) and is now working to get it certified, a process that should be smoother than the 510(k). The company guided for sales start in calendar Q4, with key commercial personnel already in place.

DiviTum shown complimentary to ctDNA at ASCO The BioItaLEE study was presented at ASCO, the world’s largest cancer conference. The study included 287 breast cancer patients receiving ribociclib and letrozole as first-line treatment and ctDNA and TK activity (with DiviTum) was measured for 241 patients. The results showed that baseline measurement and patterns throughout treatment were prognostics for treatment for both biomarkers. Measuring TKa and ctDNA were complimentary. Given the hype surrounding the latter, we believe it opens new possibilities on how to position DiviTum.

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

2022 is the year of shipping. Product tankers and LNG tankers are flying up on RuSSian war on Ukraine. Container ships are flying on supply chain congestion. We wrote several times here this year about Product tankers and LNG (we are long COOL, HAF, STNG, GLNG, FRO, MNTR). These trades have been very profitable. We like the Mintra idea, that was brought by Pareto Securities. It is a high beta trade on growth in Shipping and Energy. While most Shipping and Energy stock may not double from current levels this year, Mintra is a good doubling candidate for this year.

Mintra (www.mintra.com) provides online training courses mainly for shipping and energy.

Mintra was listed last year in Norway at 9.70 NOK at the end of 2020. Ticker MNTR

Mintra was hammered in the pandemic – the crew teams (on shipping boats and energy platforms) did not rotate due to Covid.

Lower crew rotations resulted in lower use of e-learning courses.

The situation turned around now – shipping and energy companies are in the best shape for years, generating best profits in decades. They spent more money on hiring and crew rotations – Mintra should be the beneficiary of the shipping and energy turnaround.

in 2021 Mintra acquired and successfully integrated SafeBridge.

SafeBridge was losing cash, it is now profitable under Mintra wings.

Mintra already has a 50% market share in the segment.

Safebridge acquisition decreased competition and increased Mintra pricing power

Mintra will grow by the increasing use of its courses by its existing customers, new contracts and acquisitions

Mintra guided last year 10% revenue growth for 2022. Pareto analyst believes it is too conservative. It does not reflect the current boom in Mintra´s target sectors. The consensus is low.

1Q22 was Mintra´s best quarter ever – Mintra generated a 10% FCF yield in the quarter.That is 40% annualized FCF! They can generate CF equal to their market capitalization in 2.5 years.

Next quarter is most likely much better than Q1.

Pareto analyst has Mintra as a top pick in his area.

SpareBank weekly research shows Mintra as one of the cheapest stocks in the sector.

Mintra share price is up 70% from its March lows of 2.5 NOK to current 4.3 NOK. Still well below the 9.70 NOK listing price tag.

Mintra is our doubling candidate from these price levels. It is a very good proxy to play shipping and energy boom. While most shipping and energy will not double from these levels, Mintra easily could.

Pareto on Product tankers this morning

HAFNI NO – HAFNI – Product tanker rates are moving higher again, particularly MRs and LR1s (key for Hafnia). Scorpio outperformed vastly yesterday, confirming that near all of Q2 are booked at rates that imply EPS of USD 3.5. BUY HAFNI; Q2 and Q3 estiamtes are still lagging sharply, and rate momentum seems to be returning. NAV towards NOK 50 by Q4.

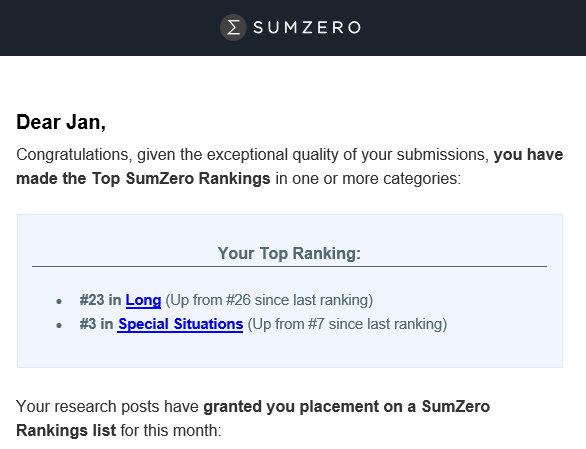

Ranking of our writings

I publish our family office ideas on SeekingAlpha (largest retail investment ideas platform) and SumZero (largest hedge fund and professional investor investment idea platform). We have noticed two achievements this week.

SumZero rated the performance of our ideas among TOP 25 and I was number 3 in the Special Situations sector.

I saw that SeekingAlpha is using our ideas (for example on Linkfire) as paid add for getting investors on the platform.

Var Energy opportunity

Last night Var Energy did USD600m secondary placement of shares. Two shareholders were selling. The share price is down today by around 10% at time of writing as some investors sold the share. I believe the share price should recover. We bought in the SPO and bought in the market after open. Var is one of the best energy companies listed in NOrway. Good enetry point for both short term and longer term trading.

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.

LInkfire delivered 51% revenue growth in Q1. Linkfire is below radar screens of most investors. In our view great opportunity. Linkfire provides smart links that lead consumers from social media to streaming platforms. Amazon Music, Apple Music and other pay Linkfire to bring consumers to their platforms. Linkfire is our top pick in the area.

Competition in the streaming industry is increasing. Linkfire is the prime tool for the streaming companies to increase their market share. Deal with Amazon Music was announced two weeks ago. we expect further deals with the majors this year.

Pareto Securities summary

Strong start to the year for Linkfire

Linkfire delivered a strong Q1’22 report, beating our topline estimates by ~13% and achieving a y/y revenue growth of ~46%, on a constant currency basis, and 51% on a recognized revenue basis, helped by the strong USD. Particularly impressive was the RPM, which grew 38% y/y and came in at DKK 9.52, Linkfire’s highest quarterly number ever, as well as the consumer connections, which grew 36% y/y to 481m (354m). We have a Buy recommendation on Linkfire with a TP of SEK 10, and expect to make some minor upward revisions to our estimates and expect a positive share price reaction today following the report.

Highlights for the quarter: – Linkfire increased its revenue by 46% y/y, on a constant currency basis and 51% on a recognized revenue basis, helped by the strong USD. smartURL, which was acquired in the beginning of Q1’22, had no significant impact to the topline in the quarter, and Linkfire is currently working on integrating the company and its traffic flows, and will come out with an update on how that is proceeding next quarter

– Revenue, on a constant currency basis, came in at DKK 11,1m (7.6m), which was ~13% higher than PAS at DKK 9.8m

– Subscription revenue grew from DKK 5.2m to DKK 6.6m (26% y/y), while commission revenue remained the main growth driver, growing from DKK 2.4m to DKK 4.6m (88% y/y), with both beating our estimates

– One of the key highlights from the quarter was the RPM, which grew by 38% y/y and came in at DKK 9.52 (DKK 6.87), which was the highest quarterly RPM in Linkfire’s history

– It was also promising to see consumer connections kicking off to a strong start in 2022, growing by 36% y/y to 481m (354m)

– EBITDA came in slightly lower than we had expected, driven by greater staff costs and slightly higher other external expenses

– The company remains confident in its mid-term target of 50-70% organic revenue growth and a gross margin of 80% as well as its FY2022 financial guidance DKK 50-60m in revenue with an EBITDA of between DKK -22 and -32m

– Following the report, we expect a positive share price reaction, as Linkfire showed that it is on good track to reach its financial guidance for FY2022

Biovica presentation at ABS conference

Biovica is starting to move prior to FDA approval. Up 10% today. Could easily double before the FDA approval in late JUne. That would be normal pattern for similar Scandi pharma stocks. See my posts here on Xbrane where we doubled our money.

We are very bullish on Biovica. Based on Broker analyst conversations, we believe the FDA approval for their innovative cancer test should happen by end of June. The reason for this timing estimate is that Biovica submitted last piec of information that th FDA wanted in May.

Do watch the video from ABG Sundal Collier conference on 24/5/2022:

Hydrogen

The Russian agression will accelerate energy transition. We have two exposures in hydrogen – Fusion Fuel and HydrogenPro. interesting article Fusion Fuel was published today on SeekingAlpha:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.