Finansavisen yesterday reported about a letter sent to the Mintra CEO Kevin Short by a shareholder asking for a buyback.

Both the letter and the link to the article is below:

Dear Kevin,

We have been your loyal shareholder since the Mintra IPO and have bought additional shares in the market.

We are writing to encourage Mintra to buyback its shares to correct the market mispricing and improve the liquidity.

The Covid era hit Mintra hard, sending its share price almost 80% lower. Under your leadership, Mintra’s share price performed well this year but is still around 50% below its IPO price of 9.7 NOK in October 2020. The share price would need to double to reach its IPO pricing.

Mintra is one of the cheapest stocks in the Scandinavian tech universe while generating strong cash flows and having one of the highest EBITDA margins in its sector. Both Pareto and Sparebank analysts believe that your share price is undervalued. So do we.

The time to do a buyback is now

You repeatedly stated on your investor calls that you are looking for further takeover targets. Takeovers may require equity issuance. Financing a takeover with your stock at current price levels makes any takeover less attractive. Mintra is also rumoured to be a takeover candidate for its two largest shareholders. That should not happen based on the current share price levels.

Put the high cash balance to work

Mintra has a large underutilized cash balance. We estimate that your year-end cash balance should exceed 140 million NOK, representing around 15% of your market capitalization. Buying your shares cheaply is a very attractive investment opportunity for Mintra.

There are multiple reasons for the buyback:

Increase investor confidence

Covid has hammered investor confidence in Mintra and caused an 80% drop in its share price. A buyback is a confidence rubber stamp from the management that the share price is undervalued. Such a signal is long overdue.

Close the valuation gap – remove the Covid era discount

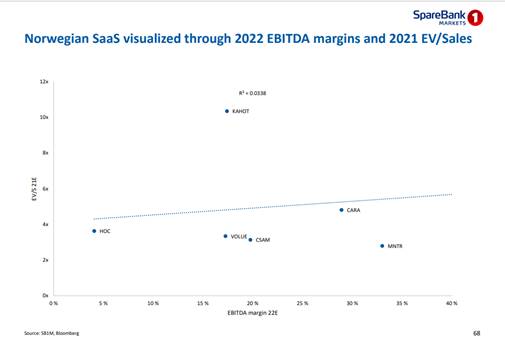

Mintra is trading at 2.6 times sales, one of the cheapest vs its Norwegian peers. At the same time, Mintra has one of the highest EBITDA margins in the sector. To illustrate Mintra low pricing, we include below the Sparebank slide from their TMT & Small Cap: SaaS Weekly Playbook dated 28.11.2022.

Improve liquidity

Mintra is not a very liquid stock. There is empirical evidence that liquidity improves with raising the share price. A successful buyback should increase both Mintra’s share price and its liquidity.

Enable capital raising for acquisition growth

The industry is consolidating. Mintra has been a successful acquirer and is looking for further acquisitions. Mintra’s low share price is limiting the company’s ability to raise capital efficiently for future acquisitions. At the current share price, Mintra’s ability to acquire other companies using its shares as a currency is hampered.

Enable takeover at a fair price

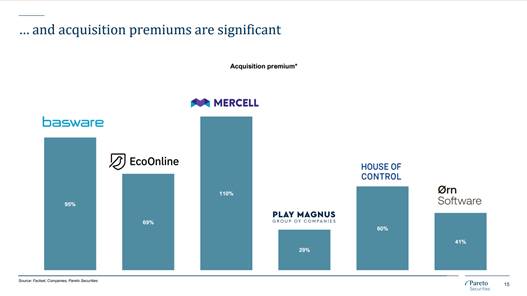

The two largest shareholders’ industrial holdings Todjur and Ferd, control 42% of Mintra’s capital. Both primarily work with private companies. They already wanted to buy Mintra before its IPO. Todjur and Ferd have been increasing their positions and are rumoured to be considering taking Mintra private. Pareto and Sparebank analysts have written about it several times. The buyout premiums this year in Norway have been between 29% and 110% (see below). The latest takeover transaction on Readly was announced with a 59% premium this week. For illustration, if such a premium was applied to Mintra’s current stock price, the resulting buyout price would be 20% below its IPO price from two years ago. That would still undervalue Mintra. A buyback should help the share price to correct and move it to more appropriate levels that could serve as a basis for a takeover.

Dear Kevin, under your leadership Mintra’s business is performing well. Its share price did not recover from the Covid shock. It is negatively affecting the company’s prospects. A stronger and more valuable Mintra is in our common interest.

Kind regards,

Jan Martinek

Link to Finansavisen article:

https://www.finansavisen.no/nyheter/teknologi/2022/12/07/7967115/mintra-eier-krever-tilbakekjop

Disclosure:

The goal of the blog is to provide investment ideas for further research. I/we have a beneficial position in the shares discussed above either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. The article does not represent investment advice. Please do your own research before making any investment action.